Picture this You have just closed a massive deal with a buyer in Europe. The goods are shipped, the invoice is sent, and you’re waiting for payment. When the Euros finally hit your Indian bank account, you notice a significant chunk is missing.

It hasn’t been stolen it has been quietly consumed by aggressive forex conversion rates and hidden transaction fees. What stings most is that with the wrong bank account setup, these losses aren’t a one off they become the routine cost of doing business.

This is the silent profit killer for thousands of export businesses in India, from thriving textile units in Tirupur to budding agri exporters near the Machilipatnam port.

If you’re running an export business, your banking partner is much more than a safe for your earnings. It’s effectively a core supplier in your global supply chain.

The difference between a current account and a carefully structured export account with EEFC (Exchange Earners Foreign Currency) facilities can be upwards of 4% per invoice a figure that exceeds most exporters entire annual profit.

So, what truly is the best bank account for export business, and how do you go beyond surface level promises to find the right fit? It’s more about who understands the RBI’s FEMA guidelines, offers transparent and responsive forex facilities, efficient documentation, and digital trade finance solutions. These are not luxury add-ons.

They are survival tools in today’s cut throat global trade.

In this comprehensive guide, we’ll go deep into the international trade banking. You’ll discover why EEFC accounts are critical, how the biggest banks stack up for exporters in real life, what features you should never compromise on, and how you can systematize your account structure to keep more of what you earn.

Practical tips, regulatory insights, expert examples, and stepwise guidance all tailored to the needs of Indian exporters.

Table of Contents

The Core Requirement: Why Standard Current Accounts Fail Exporters

Let’s start with a hard truth the default Indian current account, even a business focused one, is not designed for exporters.

A Real Life Loss Scenario

Meet Ram, owner of a small scale handicrafts export company in India. He secures an $18,000 order from a buyer in the United States. The payment hits his standard current account, and the bank auto converts it to INR at the daily card rate shaving off 1.5% compared to what he could have got with a negotiated forex deal.

His supplier in China quotes in USD, so to pay him, he converts INR back to USD, losing another 2% in the reverse transaction. On a thin margin business, he’s out nearly ₹53,000 absolutely avoidable with the right account structure.

The Mechanics of Auto Conversion

In a standard setup, foreign remittance is immediately converted at the day’s rate which is rarely the most favorable. Most exporters are forced into this. But for an operation doing regular trade, or hoping to grow, this means getting bled by the spread, repeatedly.

The Double Conversion Fee

Even more damaging if exporters then need to pay suppliers, shipping lines, or overseas consultants, they must purchase forex again at higher “card rates,” incurring further conversion losses and bank markups. Over a year, these fees add up to tens of lakhs for mid tier exporters.

The Solution: The EEFC Account

India’s best export businesses protect their foreign gains with EEFC accounts. But what exactly is an EEFC, and why does it matter so much?

The EEFC Account Explained

The Exchange Earners’ Foreign Currency (EEFC) account is an RBI approved facility that allows exporters to hold 100% of their foreign currency earnings in the currency received dollars, pounds, euros without forced conversion to INR.

This transforms the exporter’s position. With an EEFC, you:

- Shield Your Margins: By not being tied to the bank’s spot rate, you can hold funds in USD, EUR, GBP, or other major currencies. Convert them as needed, when rates are favorable or only when you need INR liquidity.

- Conduct Payments With No Double Losses: Directly pay for overseas freight, insurance, or supplier payments from your EEFC in the same currency, bypassing INR conversion entirely.

- Hedge Against Rupee Volatility: If you suspect the INR will weaken, you can even ‘park’ your dollars for weeks, timing conversions strategically before major remittances.

- Win on Speed and Transparency: Many modern banks allow real time transfers between EEFC and INR accounts, giving you full control over your money.

The Regulator’s Role

RBI has fine tuned the rules to ensure only genuine exporters benefit only AD Category-I banks can operate EEFC accounts, there’s compulsory quarterly compliance, and accounts are non interest bearing (the savings are in the spreads, not small interest).

EEFC balances that are unutilized by the end of the next calendar month must be converted to INR a built-in prompt for exporters to use currencies wisely.

Typical Beneficiaries

- Agri exporters: With fluctuating produce values, the ability to delay conversion by a month can save lakhs in off seasons.

- IT exporters and service providers: Getting paid in USD by global clients, they can pay SaaS subscriptions or software vendors from the same pot, sidestepping INR altogether.

- Manufacturers importing raw materials: By cycling forex earnings to pay overseas supplier invoices, they slash unit economics and keep pricing globally competitive.

Top Banks Comparison: Who Rules the Export World?

Choosing a bank as an exporter is more complex than most realize. Forget the superficial “which bank is largest.” Instead, judge them on their ability to support export trade reliably, transparently, and cost-effectively.

Here’s a realistic view of India’s power players, based on actual exporter feedback and up to date service audits from 2025–2026.

1. HDFC Bank: The Efficiency Engine

HDFC is the leader for ambitious, growing export operations. Let’s break down why:

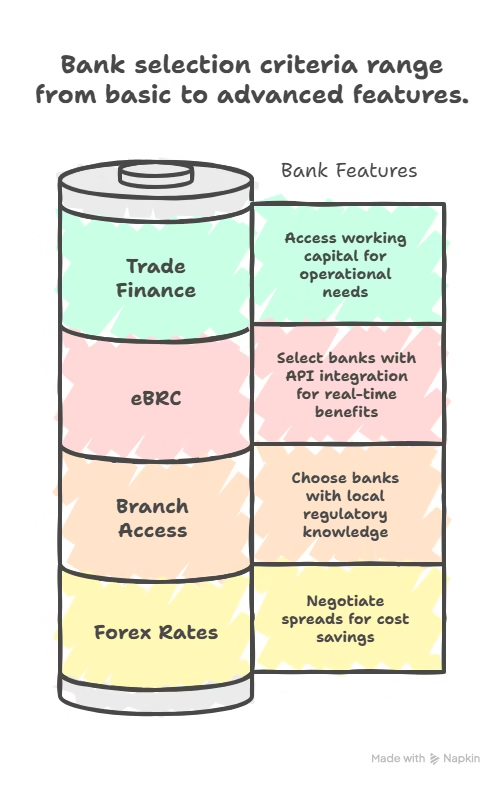

- EXIM Portal: Almost all documentation, from shipping bills to eBRCs, can be uploaded, tracked, and managed online. An exporter in Mumbai described the portal as “a digital second office,” with proactive reminders for compliance dates and instant forex deals.

- Forex Desk: HDFC’s forex team actively works with exporters, customizing rates for bulk deals. Talk to the treasury directly, and you’ll often get rates within 0.15% of the interbank spread, a key advantage for those moving large sums.

- Turnaround Speed: Payments clear remarkably fast (sometimes same day for preferred clients). In an industry where holding costs and working capital pressure are crushing, this is a crucial edge.

- Disadvantages: HDFC is premium, monthly service charges, minimum balance, and export transaction fees can seem daunting for micro enterprises (< ₹25 lakhs annual exports). However, most accounts come with bundled services like export credit lines, making it worthwhile at scale.

User Case: Textile Exporter in Surat

Rajesh, running an apparel export house, found HDFC reduced his average payment receipt time from 4 days (at his earlier state bank) to under 2 days. The ability to hedge using forward contracts further stabilized his annual margins, allowing pre planned pricing for long term buyers.

2. ICICI Bank: The Digital Innovator

ICICI combines high touch advisory with top tier digital innovation, making it a formidable choice for new age exporters.

- Trade Online Platform: Upload documents, access LC advisory, settle transactions, and get real time forex rates all without branch visits. With more than two dozen supported currencies, multi-geography deals become simpler.

- Relationship Managers: Unlike rivals that leave SMEs(small and medium enterprises) arguing through call centers, ICICI assigns direct, named managers fluent in trade finance.

- Weaknesses: Some SMEs have reported up to 3.5% markups on smaller ticket transfers. The keypoint: always negotiate forex rates or lock in forward contracts for predictable costs.

User Case: Mumbai Engineering Firm

Srinivas, exporting industrial machinery, found the “Trade Online” dashboard essential. He credits ICICI not just for timely remittance, but for guiding him through complex LC paperwork and for arranging a secure payment arrangement for high value deals, removing his dependency on costly third party legal advice.

3. State Bank of India (SBI): The National Giant

SBI doesn’t offer the most polished tech or the flashiest customer amenities,, but in reach and reliability, it’s untouchable.

- Pan India Branch Network: If you’re in a smaller city or rural trade belt places SBI is often the only bank with experienced forex staff and knowledge of local export incentives.

- Low Fees and MSME Focus: Cost sensitive businesses, especially those exporting to government buyers, benefit from SBI’s minimal monthly maintenance, low eBRC charges, and competitive export credit schemes linked to ECGC(Export Credit Guarantee Corporation) coverage.

- Drawback: Paperwork can be a little slow, particularly at non metro branches. Exporters with time sensitive supply chains may face occasional delays but for single location, agri or bulk goods exporters, the tradeoff is worth it.

User Case: Agri Exporter

Lakshman, exporting fresh produce, found that SBI’s tie-in with APEDA (Agricultural and Processed Food Products Export Development Authority) and DGFT systems allowed for rapid generation of shipping bills and automatic RoDTEP incentive claims a primary growth driver.

4. Axis Bank: The Tech Challenger

If tracking and speed are your obsession, Axis is rapidly gaining ground.

- SWIFT GPI Integration: Get granular, real time tracking of international payments. This reduces disputes if your European buyer says money has been sent, you’ll know, and can provide undeniable proof of status.

- Receivable Finance: Axis is flexible offering quick fix solutions when invoices are delayed and working capital is reduced.

- Digital Friendly: From onboarding to document submission, everything can be handled online a big plus for exporters in competitive, tight schedule segments.

- Minimum Drawback: Its rural network is still building. Exporters far from urban centers may not get full service parity with metro clients.

User Case: Bengaluru IT Services Startup

Suresh, running a SaaS export operation, prefers Axis for quick inward remittances and instant generation of eBRC certificates, which are critical for claiming MEIS (Merchandise Exports from India Scheme) and other DGFT incentives.

5. IndusInd Bank: The Startup Friend

High touch and eager, IndusInd targets SMEs and new exporters.

- Personalized Onboarding: Expect guidance at every step an advantage for first time exporters or those shifting banks.

- Low Fees and Quick Settlements: For volume exporters, or those moving multiple small shipments monthly, the transaction based fee structure means lower overall costs.

- Heavy eBRC Integration: Automated linkage with ICEGATE and DGFT systems reducing human error, speeding up government incentive claims, and lessening dead time.

- Small Network: The primary caution is their branch reach. If you’re dealing with frequent letter-of-credit validations or high value face to face negotiations, larger banks may still have the upper hand.

User Case: Startup in Chennai

Akash, exporting spices to Europe, chose IndusInd for the best in class support for DGFT documentation and rapid eBRC automation. For Akash, the bank’s willingness to process non traditional export incentives (like organic certifications) was a game changer.

6. Table: Snapshot Comparison of Top Export Banks

| Bank | Key Strengths | EEFC Features | Ideal For | Drawbacks |

| HDFC Bank | Speed, sophisticated forex desk, EXIM portal | Multi-currency, rate negotiation | Mid-large exporters, low delays | Higher fees for smaller trades |

| ICICI Bank | Trade Online, relationship managers, advisory | 24+ currencies, digital LCs | Personalized support, digitalists | Margin mark-up if not negotiated |

| SBI | National reach, lowest fee, APEDA tie-up | EEFC/RFC, MSME focus | Rural/agri, gov contract seekers | Slower processing, digital less advanced |

| Axis Bank | SWIFT GPI, real-time tracking, receivable fi. | Quick online doc and account | High-volume, urban exporters | Limited branch presence outside metros |

| IndusInd Bank | SME focus, low charges, eBRC automation | Low processing, custom onboarding | Startups, fast gov claimants | Smaller network, less global brand value |

Deep Dive: Critical Selection Factors for Exporters

Success isn’t just about choosing the right bank. It’s about leveraging its strengths with clarity. Let’s zoom in on the four critical factors you must examine and tips to exploit them fully.

1. Forex Rates and Margins

Why It Matters

The forex spread could be a silent leak or a secret profit lever. Suppose you’re exporting $250,000 in textiles a year. At a 1% better spread versus a rival bank, you’re saving ₹2,00,000+ per annum money you can reinvest in better sourcing or logistics.

Practical Tips

- Use Treasury for Big Deals: Always phone (don’t email) the bank’s treasury before closing any transaction above $10,000. Negotiate. Record confirmations.

- Forward Contracts: For predictable export cycles, hedge with forward contracts locking in rates for 3-12 months for budgeting stability.

- Monitor Daily: Keep a spreadsheet of daily rates from 3–4 banks, and select the best some exporters do this regularly before converting.

- Batch Small Transfers: If practical, batch smaller remittances to get better rates, especially at HDFC and ICICI.

2. Location and Branch Access

Real World Impact

Several industries, especially agricultural and perishable goods exporters, need banks that understand local regulatory specifics(e.g., APEDA, MPEDA, DGFT). You want a manager who knows the ins and outs of regional paperwork. For instance, in Andhra’s port cities, SBI branches have customs officers on-site, expediting document verification.

Practical Tips

- Map Branch Proximity: List all your regular document touchpoints (customs house, DGFT office, port) and compare with bank branches in that zone.

- Leverage Local Ties: Regularly engage your branch for local trade talks and seminars. Banks with active ties to trade associations are more up to date on new incentives.

3. Digital Infrastructure & eBRC

Why This Matters

The eBRC certificate is your key to government benefits. Exporters who wait weeks for BRCs miss early bird incentives and often get stuck in customs bottlenecks.

Practical Tips

- Choose Banks With API Integration: Axis and HDFC have API hooks with DGFT and ICEGATE for real time BRC transfer.

- Automate Reconciliation: Set up automatic notifications for each incoming forex transfer so BRC processing starts immediately.

- Ask for Trial Runs: Before opening an account, request a demo of the eBRC issuance and export tracking portal.

4. Trade Finance Availability

The Exporter’s Lifeline

Most exporters eventually need working capital to buy raw materials, manage logistics, and survive long payment cycles.

Export Focused Solutions

- Packing Credit (Pre-shipment Finance): Discounted rates (as low as 6–8% p.a. in foreign currency) if you’re in a sector eligible for government interest subsidy.

- Post-shipment Credit: Once BRC is received, top banks like HDFC and SBI can quickly convert document evidence into rupee liquidity, helping cover cash flow gaps caused by slow paying overseas customers.

- Foreign Currency Loans: PCFC (Packing Credit in Foreign Currency) lets exporters borrow at international rates often 2–3% lower than INR based loans.

Tips

- Negotiate Bundled Deals: Some banks offer lower forex spreads if you also take trade finance lines.

- Check Disbursal Speed: Confirm average document to credit times in writing. Delays can cost dearly during peak seasons.

The Account Opening Process: A Step by Step Guide

Opening an export account shouldn’t be overwhelming if approached methodically.

Step 1: The Documentation Stack

Be prepared complete documents mean faster approval:

- IEC Certificate: Apply with DGFT if you don’t have this banks won’t consider export accounts otherwise.

- Proof of Address/Business: GST registration, shop act license, or utility bill in the firm’s name.

- Board Resolution: Company’s formal sanction for account opening with named signatories.

- Identity and Entity Proofs: PAN/Aadhaar for all directors/partners MOA/AOA or Partnership Deed.

- Additional for Partnerships/LLPs: Registration proof and individual KYC for all partners.

Step 2: Choosing the Right Branch

Visit the AD Category-I branch not a sub or satellite office for swift forex permissions and direct access to trade managers.

- Pro tip: Request a meeting with the branch’s trade officer before submitting docs clarify process, timeframes, and application tracking.

Step 3: Activation and Digital Linking

- Timeline: Expect 2–7 working days for account activation.

- Mobile and Internet Banking: Ask for EEFC-INR account linking, app based remittance approvals, and SMS alerts for every inward forex credit.

- Test Run: Do a small test inward remittance to validate the process and check confirmation timeframes.

- eBRC Setup: Ensure your new account is registered with ICEGATE/DGFT eBRC portals for government rebate eligibility.

Account Maintenance Tips

- Quarterly Compliance: Banks will ask for trade volume verification and source of funds regularly respond promptly to avoid compliance flags.

- Annual Review: Reassess your main bank annually for shifting needs, especially if exporting to new geographies.

Mastering the EEFC Mechanism

Having an EEFC account is only step one mastering its use is what separates world class exporters.

The 100% Credit Rule Explained

Previously, there was a cap (50%) on forex earnings that could be credited to an EEFC account. Now, you can retain everything an exceptional benefit for those with regular overseas receipts.

Best Practices:

- Direct Buyer Instruction: Tell all international clients to transfer funds directly to the EEFC account. Make this clear in your commercial invoices and contracts.

- Truck Your Cash: For those who import as well as export, use your EEFC to pay foreign suppliers in their own currency, consolidating global receivables and payables efficiently.

The Conversion Trap Make It Work For You

Understand your cash flow and conversion requirements:

- Calendar Reminders: Set alerts for conversion deadlines to avoid last minute forced INR switches at unfavorable rates.

- Partial Conversions: Only convert as much as needed for Indian expenses, keeping the rest for strategic forex exposure and future payments.

EEFC & Risk Management

- Forward Contracts: Work with your bank’s treasury desk to protect future receipts from major rate swings. If you’re pricing an export contract in dollars but the rupee is leaning weaker, hedge.

- Currency Diversification: If you export to Europe and the USA, maintaining euros and dollars side by side protects you if one weakens unexpectedly.

Government Incentives and Your Bank

A robust banking relationship helps unlock and maximize government trade incentives.

RoDTEP and DBK

- RoDTEP Scheme: Your bank must support direct, automated credit of RoDTEP and Duty Drawback rebates. Delays cause working capital shortages.

- DBK (Duty Drawback): Verify your bank’s ability to facilitate customs clearances and utilize ICEGATE tie-ins for prompt claims.

Interest Equalization and Export Credit Insurance

- Interest Equalization: For sectors like engineering, handicrafts, and textiles, interest rates can be reduced thanks to government subsidy. Banks like SBI, Canara, and Bank of Baroda are enthusiastic in onboarding MSMEs and passing through benefits quickly.

- Insurance Integration: ECGC schemes are best supported by public banks ask for package deals on credit, forex, and insurance products at account opening.

Security and Compliance

Security and regulation are not just boxes to check they are the bedrock of sustainable, stress free export operations.

EDPMS: Stay on RBI’s Good Side

The Export Data Processing and Monitoring System tracks all your export proceeds. If funds don’t arrive from buyers within RBI timelines (generally nine months), your account is flagged (caution listed), blocking future shipments and incentives.

Practical Tips

- Prompt Entry: Submit proofs of export and inward receipt to your bank as soon as they occur.

- Use Bank Alerts: Enable automated monitoring and deadline alerts with your relationship manager.

- Seek Extensions Early: If payment delays are anticipated (e.g., buyer disputes), notify your bank immediately and have them work with RBI for extension approval.

Advisory Services: Leverage Bank Know How

The right banker doubles as a trade consultant:

- LC (Letter of Credit) Examination: Use in-house bank expertise to verify LCs and minimize risk of non-payment or delayed receipt.

- Country Risk Advisories: For new geographies, banks like ICICI and SBI offer periodic advisories on political, sovereign, or banking sector risks crucial for newcomers to emerging markets.

Case Study: Leveraging the Right Account for Growth

Scenario: Agri Exporter Scaling Up

Vijay, exporting processed mangoes from Andhra Pradesh, began with a basic current account at a local bank. As volumes rose, so did his conversion losses and frustration around delayed eBRCs, affecting his RoDTEP claims.

Switching to SBI, he set up both EEFC and a new INR current account. By instructing all buyers to pay into EEFC, he:

- Saved ₹3,00,000+ annually on forex spreads.

- Used eBRC API integration to claim incentives within 1 week (down from 1 month previously).

- Embedded working capital financing at subsidized rates, thanks to SBI’s MSME desk.

Within a year, his export volumes doubled as he could price more competitively and had smoother cash flows.

Conclusion: The Verdict

So, what truly is the best bank account for export business in India? There’s no universally perfect answer but there is a process to get it right for your own business.

- Choose HDFC Bank or ICICI Bank if you’re a high volume, mature exporter needing ultra reliable digital infrastructure and advisory led support.

- Start with IndusInd Bank or Axis Bank if you’re a startup, SME, or digital challenger that prizes fast settlement and low processing costs.

- Opt for SBI if local presence, broadest incentives, and cost management are primary, especially for agri or tier-2 exporters.

Your Next Steps:

- Audit Costs: Review the last several months of inward and outward forex transfers. Compare actual received rates to market averages itemize all fees.

- Open an EEFC Account: Don’t delay! Every day on a standard current account is money lost.

- Negotiate Ruthlessly: Use your audit to bargain with banks. Loyalty should not be blind get them to compete for your business.

- Automate Compliance: Go digital. Use banks with eBRC/ICEGATE integration, and subscribe to compliance and forex alerts.

- Stay Informed: RBI rules evolve. Keep an eye on annual master circulars and the latest DGFT incentives relevant to your sector.

Exporting is about bridging distances. Don’t let your bank be a roadblock make it your growth partner.

Frequently Asked Questions (FAQ)

Q: Can I withdraw cash directly from an EEFC account?

A: No, cash withdrawals are not permitted from EEFC accounts. Funds must be transferred to your INR current account or used for permitted foreign payments.

Q: Is there a minimum balance requirement for EEFC accounts?

A: There’s usually no strict minimum for the EEFC account—your primary INR account will have the balance requirement. It’s advisable to check the policy for your chosen bank.

Q: Does the EEFC account earn interest?

A: EEFC accounts are non-interest-bearing as per RBI. The savings lie in minimized conversion losses and greater flexibility.

Q: What happens if I don’t convert or use the EEFC funds?

A: Per RBI rules, funds must be converted to INR by the last business day of the month following credit if unused.

Q: Who is eligible to open an EEFC account?

A: Any individual, partnership, LLP, or company in India receiving payments in convertible foreign currency for goods, services, or software exports.

Q: Can I hold balances indefinitely in foreign currency?

A: No. Per FEMA rules, foreign exchange must be used or converted typically within one calendar month of receipt, although rules may change—check with your bank for updates.

Disclaimer: Banking regulations, eligibility, and government schemes are subject to change. For the latest FEMA guidelines, always consult with your bank’s trade or forex desk and specialists.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

My brother suggested I might like this blog. He was entirely right. This post truly made my day. You can not imagine simply how much time I had spent for this information! Thanks!

Thanks a lot! Glad the post helped you. Really appreciate you taking the time to comment. More detailed guides are coming soon.