You’ve just landed your first international buyer. The deal looks good, the price is right, and then they send three words that stop you cold.

“We’ll pay LC.”

Suddenly you’re staring at a bank document packed with clauses, conditions, and terminology that reads like it was written for lawyers, not exporters. Shipment dates. Compliant documents. Advising banks. Issuing banks. Discrepancies.

Most first time exporters do one of two things here they either panic and walk away from the deal, or they say yes without really understanding what they’ve agreed to.

Both are costly mistakes.

Here’s the truth a Letter of Credit in export is not complicated. It’s not a trap. It’s not even that unusual. It is simply a structured payment system, that has been protecting exporters and importers in global trade for decades.

This guide breaks it all down. Plain language. Real examples. No textbook fluff.

By the end, LC in export business will feel less like a foreign language and more like a tool you actually want to use.

Table of Contents

What Is a Letter of Credit?

The One Line Answer

A Letter of Credit (LC) is a written guarantee from the buyer’s bank, promising to pay the exporter as long as the exporter ships the goods and submits the right documents.

That’s it. Strip away the banking language, and that’s the entire idea.

Why Does It Even Exist?

Think about the core problem in international trade neither side fully trusts the other yet.

The exporter thinks: “What if I ship the goods and never get paid?”

The importer thinks: “What if I pay upfront and nothing arrives?”

This is what trade professionals call the trust gap and it’s been a real obstacle in global commerce for centuries. A bank letter of credit solves this by placing a neutral, credible third party the bank right in the middle of the transaction.

The bank doesn’t take sides. It doesn’t care about the goods. It cares about one thing only do the documents match the agreed terms? If yes, payment goes through. Simple, structured, enforceable.

LC Meaning in Export vs. General Banking

In general banking, an Letter of Credit is a credit instrument a line of financial promise. But letter of credit meaning in export is far more specific.

In the export world, an LC is a payment mechanism tied directly to shipment proof. The exporter gets paid not because the buyer is feeling generous, but because a bank has already committed to releasing funds the moment compliant documents land on their desk.

It shifts payment risk from “will my buyer pay?” to “can I submit the right paperwork?”. For most exporters, that’s a far easier problem to solve.

Who’s Actually Involved? (The 4 Key Players)

Before you can understand how an LC moves, you need to know who’s in the room. Every Letter of Credit in export involves four key players each with a distinct role, distinct responsibility, and a very specific moment when they matter most.

The Applicant (Importer / Buyer)

This is the overseas buyer the one who wants your goods. The applicant kicks the entire LC process off by walking into their bank and requesting the Letter of Credit be issued. They define the terms, what documents they want, what shipment dates they’ll accept, and how much they’re committing to pay. The LC is essentially their instruction manual to the bank.

The Beneficiary (Exporter / Seller)

That’s you. The LC beneficiary is the party who receives payment once compliant documents are submitted. You don’t deal with the buyer’s money directly you deal with their bank’s promise. Your job is to ship correctly and document everything precisely.

The Issuing Bank

The buyer’s bank is the one that creates and issues the LC. The issuing bank carries the payment obligation. Once your documents are verified and found compliant, this bank releases the funds. Their credibility is essentially what makes the Letter of Credit worth anything.

The Advising / Confirming Bank

This is your bank sitting on your side of the transaction. The advising bank receives the Letter of Credit from the issuing bank and passes it to you, verifying its authenticity along the way. When a bank goes one step further and adds its own payment guarantee on top of the issuing bank’s promise, it becomes a confirming bank particularly valuable when dealing with buyers in high risk countries.

The key distinction between issuing bank vs advising bank? One makes the promise. The other delivers it and sometimes backs it up with their own.

How Does a Letter of Credit Work? (Step by Step)

Understanding the letter of credit process step by step is what separates exporters who use LC confidently from those who avoid it out of fear. Here’s the full journey told from where you actually stand, the exporter’s side of the deal.

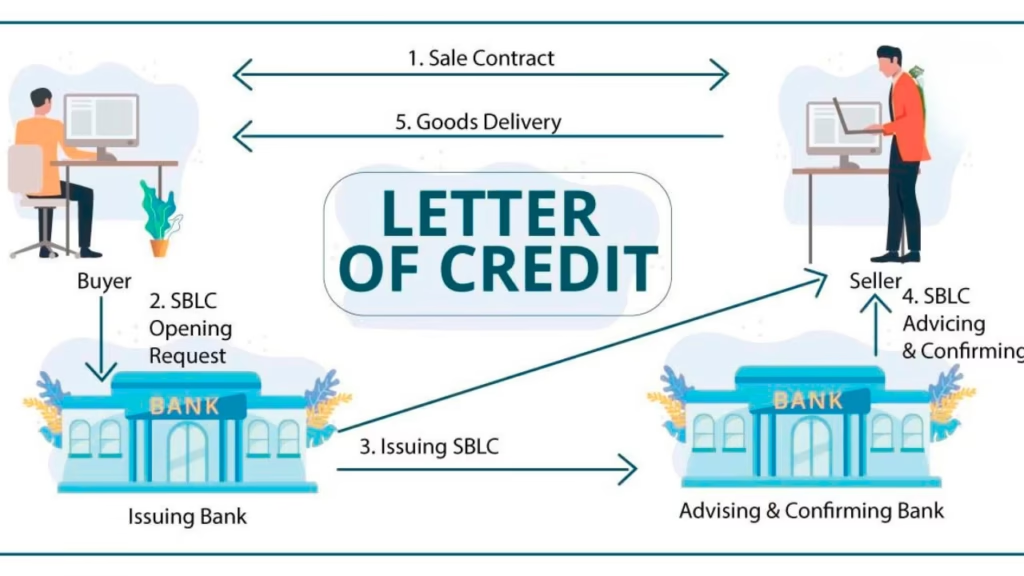

Step 1: The Sales Contract Where It All Begins

Before any bank gets involved, it starts with a conversation between you and your buyer. You agree on the product, price, delivery terms, and critically the payment method Letter of Credit.

This needs to be explicitly stated in your proforma invoice or sales contract. Don’t leave it unclear. Specify the LC type (sight or usance), the currency, and the expiry timeline. Ambiguity at this stage creates expensive problems later.

Step 2: Buyer Applies to Their Bank

With the contract signed, your importer walks into their bank the issuing bank and formally applies for the Letter of Credit . The bank evaluates the buyer’s creditworthiness and trade terms before approving and issuing the document.

This is entirely the buyer’s process. Your job here? Wait but not passively. Use this time to prepare your documentation checklist.

Step 3: LC Is Transmitted to Your Bank

Once issued, the LC travels typically via SWIFT, the global banking messaging network from the issuing bank to your advising bank. Your bank authenticates it and notifies you that an Letter of Credit has arrived in your name.

This is your green light to start preparing but not yet to ship.

Step 4: You Review the LC This Step Is Non-Negotiable

This is where most exporter mistakes happen, and where the most damage is done.

Read every line. Check:

- LC amount — does it match the invoice?

- Shipment deadline — is it realistic given your production timeline?

- Port of loading and discharge — are they correct?

- Documents required — can you actually obtain all of them?

- Payment terms — sight or usance?

- Special conditions — anything unusual or difficult to comply with?

If anything is wrong, unclear, or impossible to meet request an LC amendment immediately. Do not assume you’ll sort it out after shipping. Banks work on written terms only. What isn’t fixed in the document doesn’t exist.

Step 5: Ship the Goods, Generate Your Documents

Once you’re satisfied the Letter of Credit terms are workable, ship the goods exactly as specified. This triggers the creation of your core

Export documents:

- Commercial Invoice

- Bill of Lading or Airway Bill

- Packing List

- Certificate of Origin

- Insurance Certificate (if required under Letter of Credit terms)

Every detail product description, quantity, port names, dates must mirror the LC precisely. A mismatched spelling, a wrong unit of measurement, a date one day off any of these creates a discrepancy and can delay your payment.

Step 6: Submit Documents to Your Bank

You now hand your complete document set to your advising bank within the Letter of Credit‘s presentation period typically 21 days from the shipment date, unless stated otherwise.

Your bank checks the documents line by line against the LC terms. If everything aligns, the documents are forwarded to the issuing bank. If there are discrepancies, you’ll be notified and given the option to correct what’s correctable before time runs out.

This is the most technically demanding stage of the entire LC process in export. Treat it accordingly.

Step 7: Payment Is Released

Compliant documents reach the issuing bank. They verify. They approve.

Then:

- Sight LC → Payment is released immediately to your bank

- Usance LC → Payment is scheduled for the agreed date (30, 60, or 90 days post shipment)

Your bank credits in your account. The buyer receives the documents and uses them to claim the goods at the port. The Letter of Credit cycle is complete.

The golden rule of LC in export is Banks pay for documents, not goods. Get the paperwork right, and the money follows.

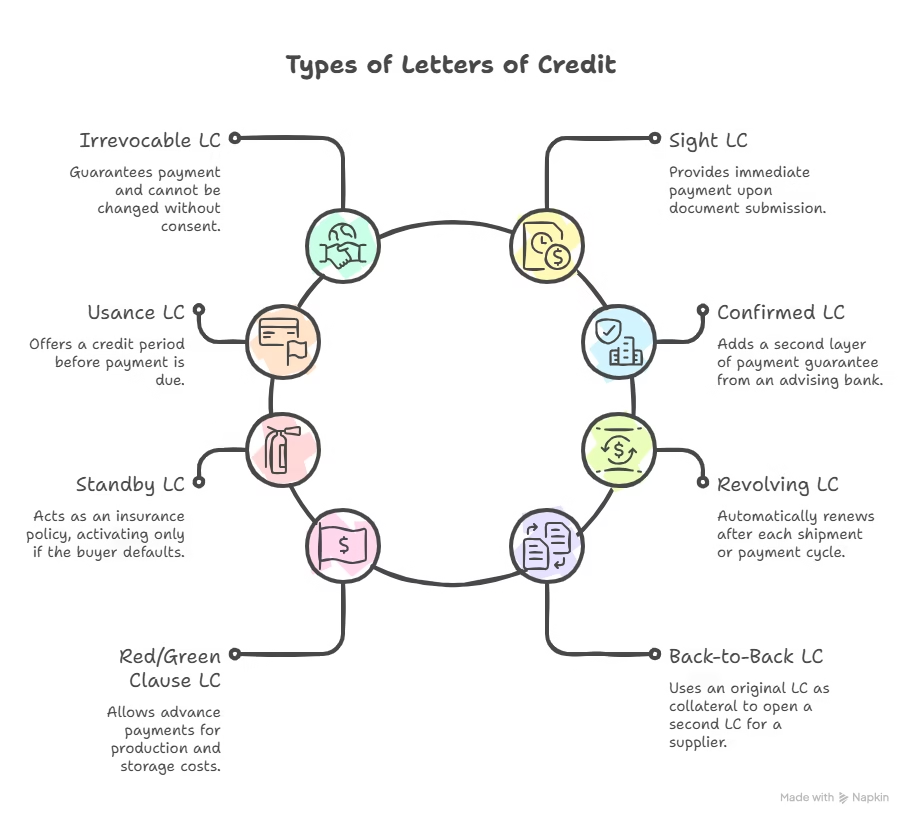

Types of Letter of Credit (Which One’s Right for You?)

Not all LCs are built the same. The types of letter of credit available in international trade are designed for different risk levels, buyer relationships, and cash flow needs. Rather than listing them like a banking manual, here’s what each one actually looks like in a real export situation.

Irrevocable LC — The Standard Choice

“We’ve agreed on terms. Nobody changes them without everyone’s consent.”

This is the baseline for most export transactions. An irrevocable letter of credit cannot be cancelled, modified, or withdrawn by the buyer or their bank without your explicit agreement. It’s the foundation of trust in Letter of Credit based trade.

If someone offers you a revocable LC one that can be changed at the buyer’s discretion walk away. Irrevocable is the only version worth accepting.

Sight LC — For Exporters Who Need Fast Cash

“Ship the goods, submit the documents, get paid.”

A sight letter of credit means payment is released the moment your compliant documents land at the issuing bank. No waiting periods, no credit extensions. If cash flow is a priority and for most small and mid size exporters it is.

Sight LC is the cleanest option. Fast, straightforward, and low risk on the payment timeline.

Usance / Deferred LC — For Competitive Markets

“The buyer needs time to sell before they can pay.”

Also called a usance LC, this type builds a credit period into the payment typically 30, 60, or 90 days after shipment. It’s common in markets where buyers expect trade credit as standard practice. Useful for winning deals in competitive industries.

But only accept it if your cash flow can absorb the wait or if your bank offers Letter of Credit discounting to bridge the gap. This is the core of the sight LC vs usance LC debate speed versus competitiveness.

Confirmed LC — When the Destination Makes You Nervous

“I trust the buyer. I’m not sure I trust their country’s banking system.”

A confirmed LC adds a second layer of payment guarantee, your own advising bank commits to paying you even if the issuing bank defaults or the buyer’s country faces a financial crisis. It costs more, but when you’re exporting to politically unstable or economically volatile regions, that extra guarantee is worth every basis point.

Standby LC — The Corporate Safety Net

“We don’t expect to use this. But it’s good to have.”

A standby LC functions less like a payment tool and more like an insurance policy. It only activates if the buyer fails to meet their payment obligation through normal channels. Common in large corporate contracts and long term supply agreements.

Think of it as the Letter of Credit equivalent of a fire extinguisher you hope you never need it, but you’re glad it’s there.

Revolving LC — For Repeat Business

“We ship every month. Let’s not open a new LC every time.”

A revolving LC automatically renews after each shipment or payment cycle, up to a pre-agreed total value. It’s efficient, administratively lighter, and ideal for established buyers you ship to regularly. Less paperwork per shipment, more time running your business.

Red Clause & Green Clause LC — Advance Payments for Trusted Partners

“I need funds to produce the goods before I can ship them.”

These specialist LCs allow the exporter to draw an advance payment before shipment funded by the buyer’s bank. The red clause covers basic production advances the green clause also covers storage costs. High trust, high risk. These are for established relationships only not first time buyers.

Back-to-Back LC — The Intermediary’s Tool

“I have a buyer’s Letter of Credit in hand. Now I need to pay my own supplier.”

Used by trading companies and intermediaries who sit between a buyer and a manufacturer. The original LC from the end buyer is used as collateral to open a second LC in favor of the actual supplier. Technically complex and not recommended for beginners but essential for traders who regularly broker between buyers and producers.

Documents Required Under a Letter of Credit

Here’s something every exporter needs to understand before their first LC shipment the bank never sees your goods. They see only your paperwork. Which means your documents aren’t just administrative they are your payment.

Every item on the LC document checklist must match the LC terms with surgical precision. Here’s what’s typically required and why each one matters.

“Banks check documents not goods. One spelling error, one wrong date, one mismatched description and your payment stalls. Precision isn’t optional. It’s everything.”

Commercial Invoice

The master document of your shipment. It must mirror the Letter of Credit exactly buyer and seller names, product description, quantity, unit price, total value, and currency. Even a minor variation between what’s written here and what the Letter of Credit specifies constitutes a discrepancy.

Bill of Lading / Airway Bill

Your proof that goods have been shipped. The bill of lading in LC is the most critical document in the set it’s what the buyer uses to claim goods at the destination port. For sea freight, it’s a Bill of Lading. For air freight, it’s an Airway Bill. Both must reflect the ports, dates, and cargo details stated in the Letter of Credit.

Packing List

A detailed breakdown of how the goods are packed number of cartons, weight, dimensions, and contents per package. Banks cross reference this against the invoice. Inconsistencies between the two are a common source of discrepancies.

Certificate of Origin

Proof of where your goods were manufactured. Required by most importing countries for customs clearance and to determine applicable duty rates. Issued by your local Chamber of Commerce or relevant trade authority. The country of origin stated here must be consistent across all other documents.

Insurance Certificate

Required when the Letter of Credit is issued on CIF (Cost, Insurance & Freight) terms. Must cover at least 110% of the invoice value a standard banking requirement. The policy date cannot be later than the shipment date.

Inspection Certificate (Where Applicable)

Some buyers particularly for industrial goods, chemicals, or food products require a third-party inspection report confirming the goods meet agreed specifications. If the LC demands one, there are no shortcuts. An accredited inspection agency must verify and certify before shipment.

Pro tip on the LC document checklist: Before you ship, lay your draft documents side by side with the LC. Read them against each other, word for word. What doesn’t match needs fixing before the goods leave your warehouse not after.

A Real World LC Example

Sometimes the clearest way to understand a financial instrument is to watch it work in real life. So here’s a real world LC example in export the kind of transaction that plays out thousands of times a day across global trade.

Meet Mahadev.

Mahadev runs a spice export business out of Kochi, Kerala. He’s been exporting domestically for years, but this is his first serious international inquiry a bulk order of black pepper and cardamom from a food distribution company based in the Netherlands.

The Dutch buyer is interested. The price works. But they’ve never done business before, and the order value is ₹45 lakhs. Neither side wants to carry the full risk. They agree on payment by Letter of Credit.

Here’s how it unfolds:

The Dutch buyer approaches their bank in Amsterdam and requests an LC in Mahadev’s favor. The Amsterdam bank issues the LC and transmits it to Mahadev’s bank in Kochi. Mahadev reviews every clause shipment date, port of loading, required documents and finds one issue the LC demands shipment within 15 days, but his production needs 22. He immediately requests an amendment, which the buyer approves.

Revised LC in hand, Mahadev ships the goods. He generates his document set commercial invoice, bill of lading, certificate of origin, phytosanitary certificate, packing list and submits everything to his bank within the presentation period.

His bank checks the documents. Everything matches. The documents travel to Amsterdam. The issuing bank verifies and releases payment. Mahadev gets paid. The Dutch buyer gets their spices. Both walked into an unfamiliar trade relationship and came out whole.

That’s how LC works in real trade not as a bureaucratic obstacle, but as the bridge that made the deal possible in the first place.

Benefits & Risks — The Honest Assessment

No financial instrument is perfect. Anyone who sells you on LC as a risk free payment solution is either uninformed or trying to sell you something. The truth, like most things in export business, sits squarely in the middle.

Here’s the honest breakdown of letter of credit advantages and disadvantages told straight.

The Real Benefits

1. Payment security that doesn’t depend on the buyer’s goodwill This is the headline advantage. When you ship under an LC, your payment commitment doesn’t come from your buyer it comes from their bank. Banks don’t default on payment obligations the way buyers sometimes do.

For exporters dealing with new clients or large order values, that shift in counterparty is enormously reassuring.

2. Opens doors to buyers you’d otherwise never touch Without LC, trading with an unknown buyer in an unfamiliar market is a gamble. With LC, the bank’s guarantee neutralizes the trust gap. Exporters who master LC documentation consistently report accessing markets and order sizes they simply couldn’t have pursued on open credit terms.

3. Protects both sides which actually helps you close deals Sophisticated importers appreciate LC too, it guarantees them that payment is only released against proof of compliant shipment. When both parties feel protected, negotiations move faster and deals close cleaner. LC isn’t just your safety net. It’s the shared foundation that makes the transaction viable.

4. Can be discounted for immediate cash flow Many banks offer LC discounting advancing you funds against a confirmed usance LC before the payment date arrives. For cash flow sensitive businesses, this turns a 90 day usance LC into near immediate liquidity.

The Real Risks

1. Document discrepancies can freeze your payment This is the most common and most painful LC risk for exporters. Banks operate on strict documentary compliance. A product description that reads “Black Pepper 500g” on your invoice but “Black Pepper – 500 grams” on the LC?

That’s a discrepancy. Seemingly trivial differences trigger delays, rejection notices, and in worst cases, non-payment. Precision isn’t a suggestion it’s the entire game.

2. LC bank charges add up faster than expected LC bank charges hit at multiple points the buyer pays to open the LC, you pay advising fees on your end, amendments cost extra, and discrepancy handling fees apply if documents need correction. For smaller order values, these costs can meaningfully erode your margin. Always factor LC costs into your pricing before you quote.

3. Amendments take time you may not have Found a problem with the LC after reviewing it? You’ll need to request an amendment which requires the buyer’s agreement, their bank’s processing, and transmission back to your advising bank. In tight shipment timelines, this back-and-forth can eat days you don’t have.

The lesson: review your LC the moment it arrives, not the night before shipping.

4. Strict compliance leaves no room for “close enough” Banks don’t exercise judgment. They apply rules. An LC that demands a specific inspection certificate from a specific agency isn’t satisfied by a similar certificate from a different agency, no matter how equivalent they may be in practice. What the LC says is what the LC means nothing more, nothing less.

The bottom line: LC is one of the most balanced payment instruments in international trade but balanced doesn’t mean effortless. Used with preparation and precision, it protects you powerfully. Used carelessly, it becomes an expensive lesson in documentary compliance.

LC vs. Bank Guarantee vs. Line of Credit

Three terms. Endless confusion. If you’ve ever Googled “letter of credit vs bank guarantee” at midnight before a client call, you’re not alone. These instruments sound similar, operate in overlapping worlds, and yet serve fundamentally different purposes. Here’s the clearest breakdown you’ll find.

The Comparison Table

| Letter of Credit | Bank Guarantee | Line of Credit | |

| What it is | Payment promise from bank | Compensation promise from bank | Pre-approved borrowing limit |

| When bank pays | On compliant documents | When buyer defaults | When you draw funds |

| Primary purpose | Facilitate trade payment | Insure against non-performance | Provide working capital |

| Who benefits most | Exporter | Either party | Borrower |

| Common in | Export transactions | Construction, contracts | Business operations |

| Risk trigger | Document compliance | Contractual default | None — it’s a facility |

LC vs Bank Guarantee — The Core Difference

Both involve a bank making a financial commitment. But the difference between LC and bank guarantee comes down to one word: timing.

An LC pays you proactively the moment you submit compliant documents, funds move. It’s built for transactions where payment is the expected outcome.

A bank guarantee pays reactively it only activates when something goes wrong. A buyer misses a payment, a contractor abandons a project, a supplier fails to deliver. The guarantee compensates the injured party after the failure occurs.

Think of it this way: an LC is the plan. A bank guarantee is the backup when the plan falls apart.

LC vs Line of Credit — Not Even Close

The LC vs line of credit confusion is understandable both involve banks and both involve credit but they operate in completely different lanes.

A line of credit is a loan facility. Your bank pre-approves a borrowing limit, and you draw from it when you need working capital. You pay interest on what you use. It has nothing to do with your buyer, your shipment, or your documents.

A Letter of Credit is a trade payment instrument. It’s not money you borrow it’s a payment guarantee tied to a specific transaction with a specific buyer.

One funds your business. The other pays for your shipment.

When to Use Which

- Exporting goods to a new international buyer? → LC

- Entering a large construction or service contract? → Bank Guarantee

- Need working capital to manage cash flow? → Line of Credit

- Buyer in a high risk country, large order value? → Confirmed LC + consider Bank Guarantee for added protection

Common Mistakes Exporters Make with LC

LC doesn’t punish ignorance gently. The system is rules based, bank enforced, and completely indifferent to good intentions. These are the mistakes that cost exporters real money and the ones that are almost entirely avoidable.

Mistake 1: Skimming the LC Instead of Reading It

The LC arrives. It’s four pages of dense banking language. You scan it, it looks fine, you move on. This is how LC discrepancies are born.

Every clause matters. Shipment date. Port names. Document specifications. Special conditions buried on page three. Read it line by line or pay someone qualified to do it with you. An hour of careful review now saves weeks of payment delays later.

Mistake 2: Missing the Shipment Deadline

LC shipment dates are not suggestions. Miss the date specified in the LC even by a single day and your entire document set becomes non-compliant. Payment stops. You’re back to requesting amendments, waiting on buyer approval, and hoping the issuing bank’s clock hasn’t already run out.

Build your production and logistics timeline backwards from the LC shipment date. If it’s not achievable, request an amendment before you start production not the day before the vessel sails.

Mistake 3: Document Format Mismatches

Your LC says “Full Set of Clean On-Board Bills of Lading.” You submit a received for shipment Bill of Lading instead.

Rejected.

Your LC specifies the invoice must show “HS Code 0904.11.” Yours doesn’t include it.

Rejected.

LC document errors like these are extraordinarily common and extraordinarily preventable. Create a document checklist directly from the LC text. Draft your documents before shipment. Cross reference everything against the LC word for word before submitting a single page.

Mistake 4: Ignoring Clauses That Seem Minor

“Goods must be packed in new, double corrugated export cartons.”

You use single corrugated. You figure it won’t matter.

It matters.

Banks enforce every condition stated in the LC including ones that feel like logistical footnotes. If a clause exists in the LC, it exists for a reason. If you can’t comply with it, raise it before shipping. Silence is not agreement in LC banking it’s a discrepancy waiting to happen.

Mistake 5: Delegating Everything to Your Freight Forwarder

Your freight forwarder is invaluable for logistics. They are not your LC compliance officer. The responsibility for correct, compliant documentation rests entirely with you the exporter.

Freight forwarders can prepare the Bill of Lading, but they don’t review your full document set against LC terms. They don’t flag that your invoice description doesn’t match the LC. They don’t notice that your certificate of origin was issued a day after your shipment date.

You do. Or you pay the price when the bank does.

The throughline across all five mistakes? LC rewards exporters who are thorough and punishes those who are rushed. Slow down on the paperwork. The payment will come faster for it.

When Should You Use a Letter of Credit?

LC isn’t the right tool for every export transaction. Knowing when to use a Letter of Credit and when not to is just as valuable as understanding how it works.

Use this as your quick decision framework.

Use LC When…

You’re dealing with a new buyer No payment history. No established trust. No problem that’s exactly what LC is designed for. Let the bank hold the risk while the relationship develops.

The order value is significant The higher the invoice value, the higher your exposure if payment fails. LC makes sense when the financial stakes justify the documentation discipline it demands.

The destination carries country risk Political instability, currency controls, unreliable banking systems if the buyer’s country raises flags, a confirmed LC shifts that risk onto banks, not onto you.

You’re entering a new market Unfamiliar trade regulations, unknown buyer behaviour, untested logistics routes. LC gives you a structured safety net while you find your footing.

Consider Alternatives When…

Your buyer is a trusted, long term partner Years of clean payment history earn a degree of trust that Letter of Credit formality can’t improve upon. For established relationships, open account export payment terms or documents against payment may serve you both better faster, cheaper, and less administratively intensive.

The order value is modest If LC bank charges represent a significant percentage of your invoice value, the cost benefit calculation shifts. Evaluate whether the protection is proportionate to the fees.

The rule of thumb: The newer the buyer, the larger the order, the riskier the market the stronger the case for LC. As trust builds over time, your payment terms can evolve with it.

FINAL THOUGHTS

Here’s what nobody tells first time exporters about the Letter of Credit the complexity you feel at the beginning isn’t the complexity of the instrument. It’s the complexity of the unfamiliar.

Once you’ve worked through your first LC reviewed the clauses, prepared the documents, watched the payment land something shifts. It stops being a wall of banking jargon and starts being exactly what it always was a structured, reliable system that lets two strangers on opposite sides of the world do business with confidence.

Letter of Credit doesn’t guarantee easy. It guarantees fair. Ship correctly, document precisely, and a bank backed payment follows. That’s a better deal than most payment instruments offer.

The exporters who thrive in international trade aren’t the ones who avoided LC out of fear. They’re the ones who took the time to understand it and then used that understanding to open doors that advance payment and open credit simply couldn’t.

You now have that understanding. The next LC that lands in your inbox isn’t a problem to solve. It’s a deal waiting to close.

Go ship something.

Frequently Asked Questions

1. What is the full form of LC in export?

LC stands for Letter of Credit. In export contexts, it refers specifically to a documentary letter of credit — a formal, bank-issued payment instrument that guarantees the exporter will receive payment once they present the correct shipment documents. You’ll also see it written as LoC in some banking documents, but LC is the universally accepted shorthand across international trade.

2. Can a Letter of Credit be amended?

Yes and more often than you’d think. The LC amendment process begins when either the exporter or importer identifies a clause that needs changing: an unrealistic shipment date, an incorrect port name, a missing document requirement. The importer formally requests the amendment from their issuing bank, which then transmits the updated terms to the advising bank.

3. What happens if documents have discrepancies?

A discrepancy occurs when your submitted documents don’t match the LC terms exactly wrong dates, mismatched descriptions, missing signatures, incorrect port names.

When discrepancies are found, the bank issues a discrepancy notice. You then have a few options correct the documents if time permits, request the buyer to waive the discrepancy, or accept that payment will be delayed until the issue is resolved. Some banks charge a discrepancy fee per document set typically between $50 and $100 on top of the delay.

4. Is LC safer than advance payment?

For the exporter, advance payment is technically safer you receive funds before a single carton leaves your warehouse. But it places the entire risk burden on the importer, which makes it a difficult term to negotiate, particularly with new or cautious buyers.

LC sits one step below advance payment on the safety scale but it’s far more commercially viable. Your payment is backed by a bank, not by buyer goodwill, which makes it the most credible guarantee available short of cash upfront. For most real world export scenarios, especially with new international buyers, LC offers the best balance between security and deal-ability.

5. What does at sight mean in a Letter of Credit?

At sight means payment is due immediately upon presentation of compliant documents the bank releases funds the moment they verify your paperwork is in order. There’s no credit period, no waiting window, no deferred timeline.

A sight LC is the fastest payment structure available within the LC framework. For exporters prioritising speed and cash flow certainty over extended buyer credit, at sight terms are the gold standard. When comparing export payment terms, “at sight” is as close to instant as international banking gets.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

3 thoughts on “What Is a Letter of Credit in Export? (And How Does It Actually Work)”