Getting paid sounds simple until you step into international trade. Selling across borders adds distance, different legal systems, currency conversion, and banking procedures. Because of that, payment becomes the most sensitive part of any export deal.

A shipment can move perfectly, documents can be correct, and the buyer may even receive the goods on time. But if the payment method is poorly chosen, the exporter may still face delays, disputes, or even complete non-payment. That is why experienced exporters focus on export payment terms before they focus on shipping.

This is where export payment terms come in.

Export payment terms define how, when, and under what conditions an exporter receives payment from a foreign buyer. These terms determine the level of financial risk for both sides and help structure the transaction in a predictable way.

In international trade, the choice of payment method affects three critical things.

Cash flow. Exporters often spend money on production, packaging, and logistics before they receive payment. The wrong payment terms can create serious cash flow pressure.

Trust between buyer and seller. A buyer may hesitate to pay in advance, while an exporter may hesitate to ship goods without payment security. Payment terms balance this trust gap.

Risk exposure. Some methods protect exporters strongly, while others shift more risk toward the seller. Choosing the right structure reduces the chances of delayed payments or financial loss.

Understanding the methods of payment in international trade helps exporters protect their revenue while still keeping deals attractive for overseas buyers.

In the coming sections, we’ll break down how payment terms work, why they exist in global trade, and how exporters decide which payment structure fits a specific deal.

Table of Contents

What Are Export Payment Terms?

At its core, export payment terms refer to the agreed conditions that determine how an international buyer will pay an exporter and when that payment will take place.

In simple terms, they answer three basic questions:

- When will the exporter receive the money?

- How will the payment be made?

- What conditions must be fulfilled before payment is released?

This forms the export payment terms definition. Every export transaction includes these conditions because buyers and sellers operate in different countries, under different financial systems.

Why Export Payment Terms Exist in Global Trade

Domestic transactions usually rely on direct trust or familiar legal systems. International trade works differently.

A buyer in another country may never meet the exporter personally. Shipping can take weeks, and resolving disputes across borders is complicated. Export Payment terms exist to reduce that uncertainty.

For example, a secure payment method may require the buyer’s bank to guarantee payment, while another method might allow the buyer to pay after receiving the goods. Each structure balances risk differently.

This is why choosing the right international trade payment terms becomes one of the first decisions in any export negotiation.

Role of Banks in Export Payments

Banks play a central role in many international trade payment methods. They act as financial intermediaries that help move money safely between countries.

In many cases, banks also verify documents such as shipping papers, invoices, and bills of lading before releasing funds. This process protects both parties by ensuring that the shipment actually took place before payment is completed.

Because exporters and buyers operate in different banking systems, banks provide the financial bridge that keeps transactions reliable.

Where Export Payment Terms Are Written

Export Payment terms are not informal agreements. They are clearly stated in official export documents so both parties understand the conditions.

You will typically find payment terms in export contracts and trade documentation, such as:

- Proforma Invoice – shared before the order is confirmed

- Sales Contract – defines commercial terms of the deal

- Letter of Credit documentation – when banks guarantee payment

Clearly stating payment conditions inside these documents ensures there is no confusion about when the exporter will be paid and what requirements must be fulfilled first.

Once these terms are agreed upon, both the exporter and buyer can proceed with the transaction knowing exactly how the payment will be handled.

Why Export Payment Terms Matter in International Trade

Export Payment terms are not just a small line in a contract. In international trade, they determine who carries the financial risk and when the money actually moves.

If exporters ignore this part of the deal, they can easily end up shipping goods without having real payment security. That’s why experienced traders negotiate payment terms before production even starts.

Risk of Non-Payment

The biggest concern in exports is simple getting paid after the goods leave your country.

Unlike domestic trade, recovering unpaid money across borders is extremely difficult. Legal systems differ, disputes take months, and enforcement can be complicated.

Because of this, exporters must evaluate the export payment risk before agreeing to any method. Some payment structures protect the seller strongly, while others place most of the risk on the exporter.

Choosing the wrong structure increases the international trade payment risk, especially when dealing with a new buyer or unfamiliar market.

Impact on Exporter Cash Flow

Exports require upfront spending. Manufacturers produce goods, packaging is prepared, logistics are arranged, and shipping costs are paid before the buyer receives the shipment.

If payment is delayed for too long, the exporter’s working capital can get stuck. This is why many businesses prefer secure payment methods for exporters that release funds quickly or guarantee payment through banks.

For example, a shipment worth $50,000 paid after 60 days may leave the exporter waiting months to recover production costs. That delay directly affects the ability to accept new orders.

Buyer–Seller Trust Level

Payment terms often reflect the level of trust between the two parties.

A first time buyer may hesitate to pay fully in advance. At the same time, exporters may be uncomfortable shipping goods without any payment guarantee.

Over time, as the relationship strengthens, both sides may move toward more flexible arrangements. The important point is payment terms evolve with trust. New trade relationships usually start with safer methods and gradually shift toward more flexible structures.

Compliance With Banking Regulations

Export payments are also tied to financial regulations.

Many countries require exporters to receive foreign currency payments through official banking channels. In India, for example, exporters must comply with RBI guidelines, and proof of payment is often required for GST refunds or export documentation.

Because of this, payment methods are closely linked to banking procedures and documentation. Proper payment terms help ensure that export transactions remain compliant and transparent.

Understanding these factors helps exporters choose payment methods that protect revenue, maintain smooth cash flow, and reduce financial risk.

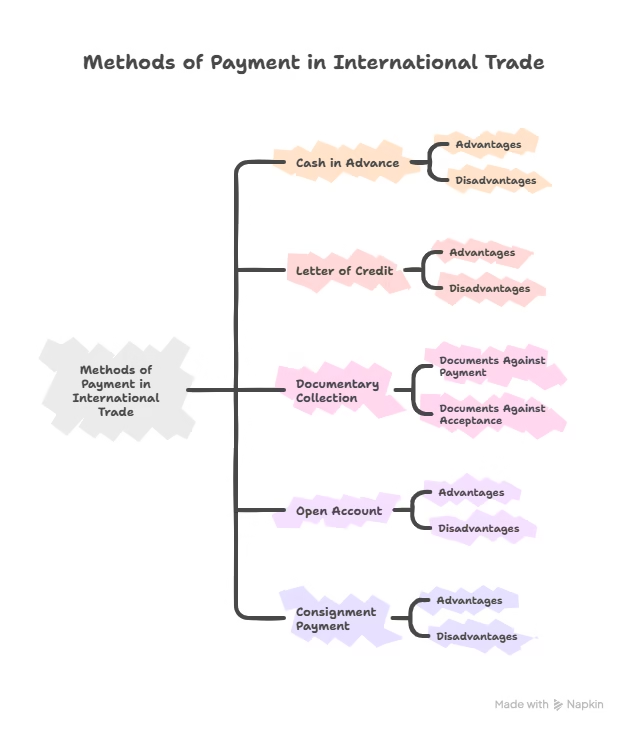

Methods of Payment in International Trade

There is no single payment method that fits every export transaction. Different deals involve different levels of trust, shipment value, and market risk.

Because of this, methods of payment in international trade range from very secure options to highly flexible arrangements. The level of security usually determines who carries the greater financial risk.

At one end, exporters receive payment before shipping goods. At the other end, exporters ship first and wait for payment later. Understanding these options helps businesses choose the right international trade payment methods based on the situation.

Below are the most commonly used export payment terms in global trade.

Cash in Advance (Advance Payment)

One of the safest payment options for exporters is advance payment in export.

Under this method, the buyer sends the payment either fully or partially before the goods are shipped. The transfer is usually made through bank wire, SWIFT transfer, or credit card.

This structure protects the exporter because production and shipping happen only after funds are received.

Exporters typically use cash in advance export payment terms in situations where the risk of non-payment is high or when the buyer urgently needs the product.

When exporters usually request advance payment

- First time buyers with no trading history

- Small or customized orders

- Products with high demand

Advantages

- Minimal payment risk for the exporter

- Immediate cash flow

- No dependency on bank approval or document verification

Disadvantages

- Buyers may hesitate to pay upfront

- Less competitive in highly competitive markets

Because of these limitations, advance payment is often combined with partial payment structures, such as 30% advance and the remaining balance before shipment.

Letter of Credit (LC)

A Letter of Credit (LC) is one of the most structured and widely used payment terms in export business, especially for large international transactions.

Under this system, the buyer’s bank issues a formal commitment guaranteeing payment to the exporter. The payment is released once the exporter submits the required documents that prove the shipment has taken place.

This makes letter of credit in international trade a reliable method because the bank takes responsibility for payment instead of relying solely on the buyer.

How LC payment works

- Buyer requests their bank to issue an LC

- The bank guarantees payment under specified conditions

- Exporter ships the goods and submits documents

- Bank verifies documents and releases payment

One common variation exporters encounter is LC at sight meaning. In this arrangement, the bank releases payment immediately after verifying the shipping documents, usually within a few working days.

Advantages

- Payment guarantee from the bank

- Reduces risk of buyer default

- Suitable for large or high value shipments

Disadvantages

- Higher bank fees

- Requires strict documentation accuracy

- Processing can take longer than direct bank transfers

Because of its security, LC payment terms in export are often used when trading with new buyers or dealing with large contract values.

Documentary Collection – Documents Against Payment (D/P)

Another widely used option is Documents Against Payment, often referred to as D/P payment terms in export.

In this method, the exporter ships the goods and sends the shipping documents through banking channels to the buyer’s bank. The buyer must make the payment before receiving these documents.

Without these documents, the buyer cannot clear the goods from customs. This structure is known as documents against payment, and it provides moderate protection for the exporter.

How D/P works

- Exporter ships goods

- Documents are sent to buyer’s bank

- Buyer pays the bank

- Bank releases documents

- Buyer clears the cargo

Because payment happens before the buyer receives the documents, this method offers more security than credit-based payment terms. However, it still carries some risk if the buyer refuses to make the payment after the shipment arrives.

Documentary Collection – Documents Against Acceptance (D/A)

Documents Against Acceptance (D/A) works similarly to documentary collection, but the payment happens later.

Instead of paying immediately, the buyer signs a legal document called a bill of exchange, agreeing to pay on a specific future date. This arrangement is known as documents against acceptance.

For example, a buyer may accept payment terms like D/A 60 days, meaning the exporter will receive payment 60 days after the documents are accepted. While this method helps buyers manage cash flow, it significantly increases the export payment risk for the seller.

Why D/A increases exporter risk

- Buyer receives goods before payment is made

- Payment depends on the buyer’s future commitment

- Recovering unpaid funds across borders is difficult

Because of this risk, DA payment terms in export are usually offered only to buyers with an established trading relationship.

Open Account

An open account payment in export is one of the most flexible arrangements in international trade.

Under this method, the exporter ships goods and delivers the necessary documents directly to the buyer. The buyer then pays the invoice after a fixed credit period.

Typical payment timelines include:

- Net 30 days

- Net 60 days

- Net 90 days

This structure is commonly known as international trade open account.

From the buyer’s perspective, it is very convenient because they receive the goods before making payment. However, for exporters, it carries a higher financial risk. Because of that, open account terms are usually offered only to long term clients or highly reliable buyers.

Consignment Payment

Among all international trade payment methods, consignment is considered the highest risk for exporters.

In a consignment export payment arrangement, the exporter ships goods to the buyer but retains ownership until the products are sold in the destination market. The buyer acts as a distributor and pays the exporter only after selling the goods.

These arrangements fall under consignment trade terms.

While this method can help exporters enter new markets, it exposes them to several risks:

- Payment depends on the buyer’s sales performance

- Unsold goods may remain in foreign warehouses

- Cash flow becomes unpredictable

For these reasons, consignment is usually used only when exporters have a very strong relationship with the overseas distributor.

Risk Comparison of Export Payment Terms

Not all export payment terms carry the same level of risk. Some methods protect the exporter strongly, while others shift most of the financial risk toward the seller.

Understanding this export payment risk comparison is important because the wrong payment structure can expose exporters to delayed payments or unpaid shipments.

Exporter Risk vs Buyer Risk

Every payment method in international trade distributes risk differently between the buyer and the exporter.

When the buyer pays before shipment, the exporter carries almost no financial risk. But when goods are shipped first and payment comes later, the exporter assumes much more uncertainty.

This creates a clear risk spectrum.

| Payment Method | Exporter Risk | Buyer Risk |

| Cash in Advance | Lowest | Highest |

| Letter of Credit | Low | Low |

| Documents Against Payment (D/P) | Moderate | Moderate |

| Documents Against Acceptance (D/A) | High | Low |

| Open Account | Highest | Lowest |

From the exporter’s perspective, cash in advance is the safest option because the payment arrives before production or shipment begins. At the other extreme, open account terms expose exporters to the highest risk because goods are delivered before payment.

Because of this balance, exporters constantly evaluate which method is the safest export payment method for a particular transaction.

How Trust Level Affects Payment Choice

In real export transactions, payment terms usually evolve as trust develops between the buyer and seller. A new trade relationship often begins with secure structures where the exporter receives payment before or during shipment. As both parties build confidence, more flexible terms may be introduced.

For example, a first shipment may use advance payment or a Letter of Credit. If the buyer consistently pays on time, future transactions might shift toward D/P or even open account arrangements.

This gradual adjustment allows exporters to reduce risk while still keeping the business relationship competitive.

Why Banks Are Involved in Risk Control

Banks play an important role in reducing payment risk in international trade. Since exporters and buyers operate in different countries, banks act as trusted intermediaries that handle document verification, fund transfers, and payment guarantees.

For example, in a Letter of Credit transaction, the buyer’s bank guarantees payment once the exporter submits the correct shipping documents. In documentary collections, banks release documents only after payment or acceptance.

By involving financial institutions, exporters gain additional protection against fraud or payment disputes. This is why many of the most secure international trade payment methods rely on banking systems to control risk.

Understanding how risk is distributed across different payment terms helps exporters choose methods that protect their business while maintaining workable agreements with overseas buyers.

How to Choose the Right Export Payment Term

Selecting the right export payment terms is rarely a one size decision. The best option depends on the buyer relationship, order value, and level of financial risk involved. Experienced exporters evaluate these factors before deciding which payment structure works best for a deal.

Payment Terms for New Buyers

When dealing with a new buyer, the priority should always be risk protection. Since there is little trading history, exporters should rely on the safest payment method for export transactions.

Common options include:

- Advance payment

- Letter of Credit at sight

- Partial advance with balance before shipment

These structures ensure the exporter receives funds before the shipment leaves the country or has bank backed payment security.

Payment Terms for Repeat Buyers

Once a trading relationship is established, exporters may choose more flexible arrangements. Repeat buyers who have consistently honored previous payments may be offered options such as:

- Documents Against Payment (D/P)

- Partial advance with balance against shipping documents

- Short credit periods

These terms help maintain competitiveness while still keeping payment risk under control.

Payment Terms for Large Orders

Large export shipments involve greater financial exposure, which makes payment security even more important.

For high value transactions, exporters typically rely on bank supported payment structures, such as:

- Letter of Credit

- Confirmed LC

- Structured milestone payments

These arrangements reduce the chances of non-payment while ensuring that exporters recover their production and logistics costs. Ultimately, the best payment terms for exporters depend on balancing two factors protecting financial security while keeping the deal attractive for the buyer.

Choosing the right payment structure helps exporters manage risk, maintain stable cash flow, and build long term international trade relationships.

Best Practices for Export Payment Agreements

Payment terms should never be unclear in international trade. If the conditions are not written clearly, misunderstandings happen fast and resolving disputes across borders becomes difficult.

A proper export payment agreement removes ambiguity by specifying every financial condition in writing. These details are usually included in the proforma invoice, sales contract, or other official documents that form the international trade payment contract between the exporter and buyer.

Here are the key elements that should always appear in a well structured export payment agreement.

Currency Specification

The contract must clearly state the currency in which payment will be made.

Since international trade involves multiple currencies, failing to define this can create confusion when exchange rates fluctuate. Exporters typically specify widely used currencies such as USD, EUR, or GBP to avoid volatility in local currencies.

For example, an invoice might state that the buyer must pay USD 25,000 via international bank transfer. This removes uncertainty and ensures both parties understand the exact financial value of the transaction.

Payment Timeline

Export contracts should also define the exact payment timeline.

Terms like Net 30, Net 60, or Net 90 indicate the number of days the buyer has to make payment after receiving the invoice or shipment documents. Without a defined timeline, buyers may delay payments indefinitely.

Clear payment timelines help exporters maintain predictable cash flow and reduce disputes about due dates.

Payment Method

Another critical part of the export payment agreement is specifying how the payment will be transferred.

Common methods include:

- SWIFT bank transfer

- Telegraphic Transfer (TT)

- Letter of Credit (LC)

- Documentary Collection

Defining the payment channel ensures the funds move through recognized banking systems, which is important for both financial security and regulatory compliance.

Bank Charges Responsibility

International transfers often involve multiple banks, and each may charge processing fees.

Export contracts should clearly state who will bear these charges. In many cases, buyers agree to cover the transaction fees charged by their bank, while exporters handle charges from their receiving bank.

Without this clarification, exporters may receive less money than expected due to deductions along the banking chain.

Late Payment Penalties

Including penalties for delayed payments creates a strong incentive for buyers to respect the agreed timeline.

A contract may specify interest charges for overdue invoices, such as 1–2% monthly interest on late payments. While penalties are not always enforced, their presence in the contract discourages unnecessary delays.

When these elements are written clearly, exporters reduce the risk of disputes and ensure the financial structure of the deal is understood by both parties.

Compliance for Indian Exporters

Export payments are not just commercial agreements they are also regulated financial transactions. For Indian exporters, receiving foreign payments must follow specific regulatory procedures.

Understanding export payment compliance in India helps exporters avoid legal issues and ensures they receive the financial benefits associated with export transactions.

RBI Export Payment Rules

The Reserve Bank of India (RBI) regulates how export payments are received and reported.

Under export payment RBI rules, exporters must receive payment for shipped goods within a specified period, usually through authorized banking channels. Payments are typically routed through banks using international systems such as SWIFT.

These regulations ensure that export proceeds enter the country legally and are recorded properly within the financial system.

eBRC and FIRA Documentation

Two important documents are generated when export payments are received.

Foreign Inward Remittance Advice (FIRA) confirms that foreign currency has been received through a banking channel. This document acts as proof that the exporter has received payment from overseas.

The Electronic Bank Realization Certificate (eBRC) is issued by banks after export proceeds are realized. It serves as official confirmation that the exporter has received payment against a specific shipment.

Proper eBRC export payment documentation is essential because it is often required when claiming government export incentives or completing regulatory filings.

GST Refund Linkage

For many exporters, GST paid on inputs can be refunded once export proceeds are realized.

The government typically requires proof of payment through export documentation such as shipping bills and bank certificates. Because of this linkage, receiving payments through official banking channels becomes essential for tax compliance.

Without proper documentation, exporters may face delays or rejection of GST refund claims.

Role of ECGC Insurance

Even with proper payment terms, exporters sometimes face the risk of buyer default. To reduce this exposure, many businesses use insurance provided by the Export Credit Guarantee Corporation of India (ECGC).

ECGC policies protect exporters against losses caused by non-payment due to commercial risks or political disruptions in the buyer’s country.

For exporters entering new markets or dealing with unfamiliar buyers, this insurance can act as an additional safety layer in managing international payment risk.

By following proper banking procedures and maintaining correct documentation, exporters can stay compliant with regulations while ensuring that their international payments are secure and legally recognized.

Common Mistakes Exporters Make With Payment Terms

Many exporters focus heavily on product quality, pricing, and logistics. But the real financial damage in international trade often comes from mistakes in payment terms.

These export payment mistakes usually happen because exporters rush into deals without properly assessing risk or documenting payment conditions. Once the goods leave the country, fixing those mistakes becomes extremely difficult.

Here are some of the most common international trade payment problems exporters face.

Offering Open Account Too Early

One of the biggest mistakes exporters make is offering open account payment terms to new buyers too quickly.

Open account terms mean the exporter ships goods first and receives payment later. While this arrangement can attract buyers, it exposes the exporter to significant financial risk.

Without an established trading history, the exporter has little protection if the buyer delays payment or refuses to pay altogether. Open account terms should usually be reserved for buyers with a strong and reliable payment track record.

Not Verifying Buyer Credibility

Another major mistake is failing to check whether the buyer is financially reliable.

Before agreeing to flexible payment terms, exporters should always verify the buyer’s credibility through available trade information sources. Ignoring this step increases the chances of delayed payments or complete defaults.

Even a legitimate company can face financial difficulties, which may affect its ability to pay on time. Verifying a buyer’s background helps exporters make informed decisions about which payment terms are safe to offer.

Poor Documentation

Payment disputes often arise because important details were never written clearly in the export contract.

If payment timelines, currency, or banking methods are unclear, misunderstandings can quickly turn into disputes. In international trade, resolving those disputes becomes complicated due to legal differences between countries.

Clear documentation reduces the chances of disagreements and ensures both parties understand their obligations.

Not Involving Banks Early

Banks play an important role in securing international payments, yet some exporters attempt to handle payment arrangements without proper banking involvement.

For example, relying entirely on informal agreements without structured banking processes increases exposure to fraud or delayed payments. Using bank supported payment methods, such as Letters of Credit or documentary collections, provides an additional layer of financial protection.

Avoiding these common mistakes helps exporters protect their revenue and build more stable international trading relationships.

Conclusion

Understanding export payment terms is one of the most important parts of running a successful export business.

Every international transaction begins with a simple but critical question how and when will the exporter be paid? The answer determines the level of financial risk, the stability of cash flow, and the overall security of the deal.

Different international trade payment methods exist because exporters and buyers operate in different countries with varying levels of trust and financial exposure. Some methods prioritize security, while others prioritize flexibility.

For beginners, the safest approach is to start with payment structures that offer strong protection, such as advance payment or bank backed arrangements like Letters of Credit. These methods reduce the risk of non-payment and ensure that exporters receive funds for their shipments.

As trading relationships grow and trust develops, exporters may gradually move toward more flexible payment arrangements. However, those decisions should always be based on a clear understanding of the risks involved.

A solid export payment terms guide ultimately helps exporters protect their business, manage financial risk, and build long term international trade partnerships with confidence.

Frequently Asked Questions (FAQs)

What are export payment terms in international trade?

Export payment terms are the agreed conditions that define how and when an exporter receives payment from an international buyer. These terms specify the payment method, timeline, and banking process involved in the transaction. Common methods of payment in international trade include advance payment, letter of credit, documentary collection, and open account.

Which export payment method is safest for exporters?

The safest export payment method for exporters is usually cash in advance, where the buyer pays before the goods are shipped. Another secure option is a Letter of Credit (LC) because the buyer’s bank guarantees payment once the exporter submits the required documents.

What is the difference between LC and TT payment in export?

TT (Telegraphic Transfer) is a direct bank-to-bank transfer where the buyer sends money electronically to the exporter. In contrast, a Letter of Credit involves the buyer’s bank guaranteeing payment once specific shipping documents are verified. TT is faster and simpler, while LC provides stronger payment security.

When should exporters use open account payment terms?

Open account payment terms in export are typically used only with trusted, long-term buyers. Under this method, the exporter ships goods first and the buyer pays later, usually within a fixed period such as 30 or 60 days. Because the exporter carries the payment risk, this method should not be used with new buyers.

What documents prove that export payment has been received in India?

For Indian exporters, banks issue documents confirming that foreign payment has been received. The most important ones are Foreign Inward Remittance Advice (FIRA) and the Electronic Bank Realisation Certificate (eBRC). These documents help demonstrate export payment compliance and are often required for GST refunds and other export-related benefits.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

3 thoughts on “Export Payment Terms Guide: Safest Methods of Payment in International Trade”