What DP and DA Really Mean in Real Export Transactions

Knowing how DP vs DA in export actually works can save exporters from unpaid shipments, broken buyer relationships, and years of legal follow ups that lead nowhere.

On paper, DP and DA payment terms look simple. Banks explain them in a few easy lines, exporters nod along, and shipments move.

In reality, DP and DA are among the most misunderstood export payment terms, especially by first time exporters.

From what I’ve seen across real export transactions, exporters don’t lose money because they choose DA instead of DP. They lose money because they don’t understand where the bank’s responsibility ends and their risk begins.

This guide explains DP vs DA payment terms in export the way exporters experience them on the real ground not how banks describe them in brochures.

We’ll break down:

- What DP and DA actually mean

- How DP and DA work step by step

- Where exporters assume they are protected (but aren’t)

- Why banks rarely explain the real risks

- And how to decide when to use DP or DA safely

No hype. No fear mongering. Just export reality.

Table of Contents

Why DP and DA Confuse New Exporters So Much

Most exporters first hear about DP and DA when:

- A buyer rejects advance payment

- A buyer says “LC is too expensive”

- A bank suggests “documentary collection”

That’s when exporters are told:

- DP is safer

- DA is riskier

- Bank will handle documents

That explanation is incomplete.

In real export trade, banks do not guarantee payment under DP or DA. They only handle documents. This single misunderstanding causes more export losses than almost any other payment term.

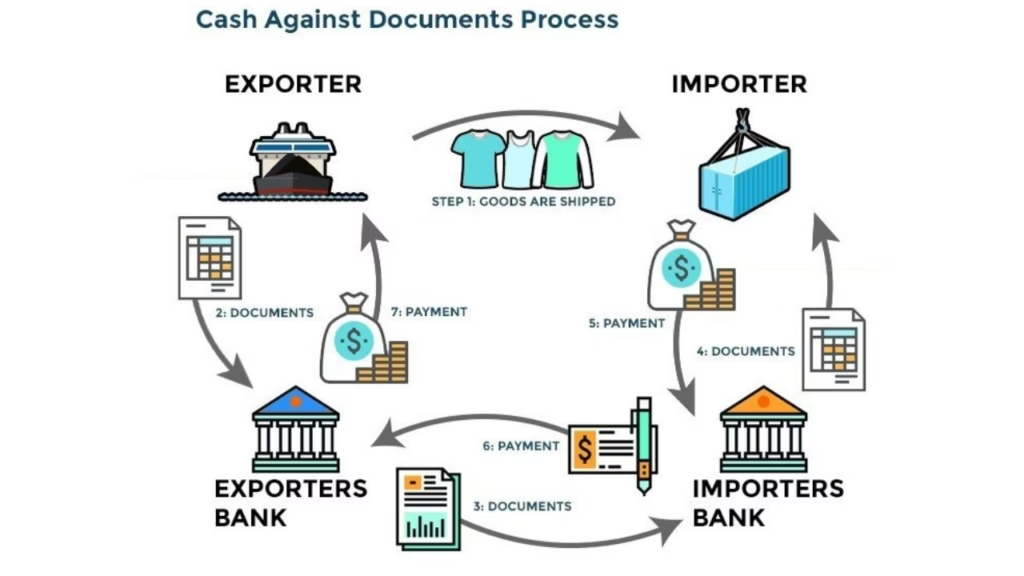

What Is DP Payment Terms in Export? (Documents Against Payment)

Let’s start with DP payment terms in export, also known as:

- Documents Against Payment export

- Cash Against Documents (CAD)

- DP at sight payment terms

DP Meaning in Payment Terms (Simple Explanation)

Under DP payment terms, the exporter ships the goods and submits shipping documents to the bank. The buyer can collect those documents only after making payment.

Sounds safe, right?

This is why many beginners assume:

“DP means payment is guaranteed.”

That assumption is dangerous.

How DP Payment Terms Work in Export (Actual Flow)

Here’s the real process exporters go through:

- Exporter ships the goods

- Exporter submits documents to their bank

- Exporter’s bank sends documents to buyer’s bank

- Buyer’s bank informs the buyer

- Buyer pays

- Buyer gets documents

- Buyer clears cargo

Important point:

The bank does not promise the buyer will pay

If the buyer refuses to pay, the bank does nothing except return documents.

Exporter Reality (DP)

From real DP shipments:

- Buyers delay payment

- Buyers renegotiate price

- Buyers ask for discounts

- Buyers simply walk away

The bank does not:

- Force payment

- Compensate exporter

- Take responsibility for cargo

This is where DP payment term meaning in export differs from exporter expectations.

What Is DA Payment Terms in Export? (Documents Against Acceptance)

Now let’s look at DA payment terms in export, also called:

- Documents Against Acceptance export

- Time draft DA export

- DA 30 / 60 / 90 days payment terms

DA Export Payment Term Meaning (Simple Explanation)

Under DA payment terms, the buyer does not pay immediately.

Instead, the buyer:

- Accepts a time draft (promise to pay later)

- Receives documents immediately

- Clears the goods

- Pays after agreed credit period (e.g., 60 days)

This is why DA is often used when buyers demand credit.

How DA Payment Terms Work in Export (Actual Flow)

Here’s what really happens:

- Exporter ships goods

- Documents go to buyer’s bank

- Buyer signs acceptance

- Buyer gets documents

- Buyer clears goods

- Buyer is supposed to pay later

Key exporter risk:

Once documents are released, exporter has no control. If the buyer defaults later, recovery is extremely difficult.

DP vs DA Payment Terms: Core Difference (Exporter View)

On paper:

- DP = payment first, documents later

- DA = documents first, payment later

In real export transactions:

- Both rely on buyer honesty

- Neither offers bank payment guarantee

- Both fall under documentary collection, not credit protection

This is why experienced exporters treat DP vs DA payment comparison as a risk decision, not a banking formality.

What Banks Actually Do in DP and DA (Important Clarity)

Banks handle:

- Document forwarding

- Collection instructions

- Payment routing (if buyer pays)

Banks do NOT:

- Guarantee payment

- Enforce buyer obligation

- Cover exporter losses

- Take cargo responsibility

This is the single biggest misunderstanding in export documentary collection DP DA.

Why Banks Don’t Explain DP and DA Risks Clearly

From experience, banks:

- Assume exporters understand trade risk

- Avoid discouraging transactions

- Focus on compliance, not commercial outcomes

Banks are service providers, not business partners.

If a DP or DA deal fails:

- Exporter loses money

- Bank still earns charges

That’s the uncomfortable truth new exporters learn late.

Where DP Feels Safe (But Isn’t Always)

DP is safer than DA but not risk free.

Common DP risk situations:

- Buyer delays payment intentionally

- Buyer uses cargo as negotiation leverage

- Buyer disappears after shipment arrives

- Buyer’s country imposes sudden restrictions

If payment doesn’t happen:

- Cargo sits at port

- Storage costs increase

- Exporter pays demurrage

- Re-export is expensive

This is why is DP safe in export business? depends on buyer credibility, not the payment term alone.

Where DA Becomes Extremely Risky

DA risks increase when:

- Buyer is new

- Market is volatile

- Buyer’s country has weak legal enforcement

- Exporter depends on one buyer

DA default risk in export payment is real and common.

Once documents are released:

Exporter loses all leverage

Exporter Mindset Shift (Very Important)

Experienced exporters don’t ask:

“Is DP or DA allowed?”

They ask:

“What happens if the buyer doesn’t pay?”

That mindset alone changes how DP and DA are used.

The Real Risks Behind DP and DA Payment Terms

By now, you understand what DP payment terms in export and DA payment terms in export technically mean.

Now we move into the part that actually hurts exporters:

what goes wrong after shipment leaves India.

This is where theory ends and losses begin.

Risk #1: Banks Do NOT Guarantee Payment (Most Dangerous Assumption)

This is the biggest and most costly misunderstanding in DP vs DA export payment meaning.

Many new exporters believe:

“The bank is handling documents, so payment is safe.”

That is false.

Under both documents against payment export and documents against acceptance export, banks only act as document handlers, not payment guarantors.

If the buyer:

- refuses to pay (DP)

- delays payment (DA)

- disappears completely

the bank simply returns documents or closes the case.

From real export cases I’ve seen:

- Exporters wait months

- Banks send reminders

- Nothing happens

- Exporter absorbs the loss

This single misunderstanding explains most export documentary collection risks.

Risk #2: DP Is Not “Pay First, Then Ship” (Timing Trap)

Many exporters wrongly think DP means:

“Buyer pays before shipment.”

In reality:

- Shipment is already on the water

- Cargo has already arrived

- Buyer knows exporter is under pressure

This creates leverage for the buyer.

Common DP manipulation tactics buyers use:

- “Market price dropped, reduce invoice”

- “Quality issue, pay less”

- “We’ll pay next week” (and delay)

Meanwhile:

- Storage charges increase

- Demurrage starts

- Exporter loses negotiation power

So yes, DP payment term meaning in export still carries risk.

Risk #3: DA Payment Terms Destroy Cash Flow (Silent Killer)

DA payment terms in export look attractive because:

- Buyer agrees quickly

- Order size increases

- Relationship feels “strong”

But here’s the reality.

Under DA 30 / DA 60 / DA 90 payment terms:

- Exporter pays supplier

- Exporter pays freight

- Exporter pays GST

- Exporter pays bank charges

But receives no money for months.

If the buyer delays even by 30 days:

- Cash cycle breaks

- Working capital locks

- Exporter struggles to fund his next shipment

This is why DA export payment risk is not just default it’s liquidity.

Risk #4: Once Documents Are Released (DA), Control Is Gone

This is the point of no return.

In DA payment terms, once the buyer accepts the draft:

- Documents are released

- Buyer clears goods

- Exporter loses leverage

If buyer doesn’t pay later:

- Legal action is costly

- Cross border recovery is slow

- Often not worth pursuing

From what I’ve seen:

- Many DA defaults are not fraud

- Buyers simply delay indefinitely

- Exporters keep “following up”

This is the reality of DA default risk in export payment.

Risk #5: Buyer Country Risk Is Ignored (Big Mistake)

Banks process DP and DA the same way regardless of:

- Country enforcement strength

- Political risk

- Currency controls

Exporters shouldn’t.

High risk DA situations include:

- Weak legal systems

- Currency shortages

- Import restrictions

- Sudden policy changes

In such cases:

- Even honest buyers may not pay on time

- Funds get stuck

- Exporter bears loss

This is why DA vs DP payment terms international trade must be evaluated country wise, not just buyer wise.

Risk #6: Payment Terms TT LC DA DP Are NOT Equal

Exporters often see lists like:

payment terms tt lc da dp And assume all are similar. They are not.

Quick comparison:

- TT Advance → Lowest risk

- LC → Conditional safety

- DP → Moderate risk

- DA → High risk

Yet many exporters move from:

TT → DP → DA

without understanding how much protection they are giving up.

This is how exporters unknowingly downgrade their risk position.

Risk #7: Banks Still Earn Fees When Exporters Lose Money

This is uncomfortable, but important.

Under export bank documentary collection DP DA:

- Bank earns handling charges

- Bank earns remittance fees

- Bank earns document fees

Whether:

- Buyer pays

- Buyer delays

- Buyer defaults

The bank’s income is unaffected. So banks rarely warn exporters strongly unless asked. That’s why banks never explain DP vs DA risks clearly they are not incentivized to.

DP vs DA Export Payment Comparison (Risk View)

| Factor | DP | DA |

| Payment timing | Before document release | After document release |

| Exporter control | Medium | Very low |

| Cash flow impact | Moderate | High |

| Default risk | Medium | High |

| Suitable for new buyers | Sometimes | No |

| Bank guarantee | No | NO |

This table alone explains why experienced exporters treat DA very cautiously.

When DP Makes Sense (Real Export Use)

DP works best when:

- Buyer is known

- Country risk is low

- Cargo can be diverted if needed

- Exporter can absorb delays

Even then, exporters often add:

- partial advance

- strict timelines

- buyer penalties

When DA Should Be Avoided

Avoid DA when:

- Buyer is new

- Order value is high

- Exporter depends on cash flow

- Legal recovery is weak

From real exporter experience:

One bad DA deal can wipe out profits from multiple successful shipments.

When to Use DP or DA Safely (and When to Walk Away)

By now, one thing should be clear:

DP and DA are not payment guarantees. They are trust based systems.

The mistake beginners make is treating DP vs DA payment terms as banking formalities. Experienced exporters treat them as risk decisions.

This final part focuses on:

- when DP actually works

- when DA becomes dangerous

- how exporters reduce DP and DA risks

- and how DP compares with LC and TT in real trade

When DP Payment Terms Make Sense (Exporter Reality)

Despite the risks, DP payment terms in export are widely used and they work when applied correctly.

DP is suitable when:

- Buyer is known and verified

- Exporter has done multiple successful shipments

- Buyer’s country has stable banking systems

- Cargo can be diverted or resold

- Exporter can absorb short payment delays

From what I’ve seen, DP works best in:

- repeat buyer relationships

- short transit routes

- commodities with alternate buyers

Even then, smart exporters rarely rely on DP alone.

They add:

- partial advance (20–30%)

- strict payment timelines

- demurrage responsibility clauses

DP is not “safe.” It is manageable when structured properly.

When DA Payment Terms Should Be Used (With Extreme Caution)

DA payment terms in export are often requested by buyers who want credit.

DA can make sense only when:

- Buyer is long term and proven

- Exporter understands buyer’s cash cycle

- Exporter has strong working capital

- Country legal enforcement is reliable

- Credit period is short (DA 30, not DA 90)

Even then, exporters limit:

- shipment value

- credit exposure

- shipment frequency

From real export experience:

DA is not a payment method. It is a credit decision. If you wouldn’t give the buyer an unsecured loan, DA should not be offered.

When Exporters Should Say NO to DA

Many exporters accept DA because:

- buyer pressures them

- competitors agree to DA

- order value looks attractive

This is where businesses collapse.

Avoid DA when:

- buyer is new

- order value is high

- exporter depends on cash flow

- market prices are volatile

- buyer’s country has currency controls

One unpaid DA shipment can:

- block capital

- delay salaries

- stop future shipments

This is the real DA export payment risk banks rarely discuss.

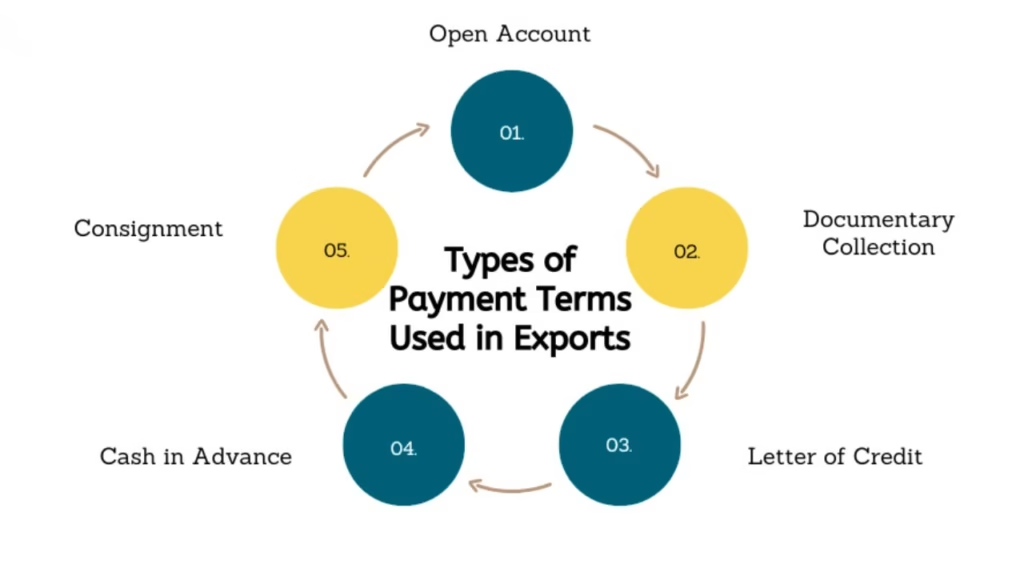

DP vs DA vs LC: What Exporters Actually Choose

Exporters often compare:

payment terms TT LC DA DP

But these are not equal.

Here’s the real exporter hierarchy:

TT Advance

- Safest for exporter

- Risk entirely on buyer

- Rare for new buyers

Letter of Credit (LC)

- Conditional protection

- Expensive

- Complex documentation

- Still safer than DP/DA

DP (Documents Against Payment)

- Moderate risk

- Buyer controls timing

- No guarantee

DA (Documents Against Acceptance)

- High risk

- Credit based

- No control after document release

This is why experienced exporters often say:

“If LC is not possible, DP is the last acceptable option. DA is credit.”

DP vs Letter of Credit

Many buyers say:

“LC is costly, let’s do DP.”

What exporters should understand:

- LC transfers payment obligation to bank (if compliant)

- DP does not transfer obligation at all

- LC protects against buyer refusal

- DP does not

So while DP looks similar to LC on paper, risk exposure is completely different.

How Exporters Reduce DP and DA Risks (Real Techniques)

Exporters who survive long term don’t avoid DP and DA they control them.

Common risk mitigation methods:

- Partial advance + DP

- Smaller shipment values

- Shorter DA periods

- Export credit insurance

- Buyer financial checks

- Country risk assessment

- Diversifying buyers

From real operations:

- Risk is acceptable when it is calculated.

- Risk is fatal when it is assumed away.

Bank Role in DP and DA Payments (Reality Check)

Banks:

- process documents

- follow instructions

- send reminders

Banks do NOT:

- verify buyer intent

- ensure payment

- recover money

- compensate exporter

Understanding this clearly changes how exporters use export documentary collection payment.

Common Beginner Mistakes with DP and DA

Let’s call them out directly:

- Treating DP as guaranteed payment

- Offering DA too early

- Trusting buyer assurances over cash history

- Ignoring country level risk

- Confusing bank involvement with protection

Every exporter who loses money under DP or DA usually makes at least two of these mistakes.

Final Note

DP and DA are not “bad” payment terms. They are honest terms they expose the real nature of trade: trust, timing, and risk.

Exporters fail not because they used DA. They fail because they used DA without understanding what it is and how it works.

If you can remember just one point from this guide, remember this:

Banks manage documents. Exporters manage risk. Once you accept that, DP and DA stop being scary and start being strategic.

Frequently Asked Questions

What is DP vs DA in export?

DP and DA are documentary collection payment terms where banks handle documents but do not guarantee payment.

What is the difference between DP and DA payment terms?

Under DP, payment is required before document release. Under DA, documents are released against a promise to pay later.

Is DP safe in export business?

DP is safer than DA but still carries risk. Buyer credibility and country risk matter more than the term itself.

What is DA payment terms in export?

DA allows the buyer to clear goods immediately and pay after an agreed credit period.

What are export documentary collection risks?

Risks include buyer refusal, delayed payment, default, cash flow blockage, and lack of bank guarantee.

When should exporters avoid DA?

Avoid DA for new buyers, high value shipments, weak legal markets, or when working capital is limited.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining export business topics in a practical, beginner friendly way, based on how Indian exports actually work on the real ground especially documentation, quality control, and buyer expectations.

1 thought on “DP vs DA in Export: 7 Critical Risks Banks Never Explain to New Exporters”