Here’s the part most beginners get completely wrong. They obsess over product selection, pricing, and logistics. But the real damage in export business doesn’t happen at the factory or port. It happens when the payment doesn’t come in.

You can ship perfectly, deliver on time, and still lose money if your payment terms are weak. That’s not a rare situation. It’s common. In the export business, profit is decided by how you get paid, not just what you sell.

This is exactly where advance payment comes in.

A lot of people treat it like a “strict” or “old school” option. That’s a mistake. Advance payment isn’t about being strict. It’s about controlling risk before it controls you. When you structure deals around advance payment, you’re not being difficult. You’re protecting your cash flow, your time, and your business stability.

This guide isn’t theory. You’re not going to get textbook definitions or generic advice.

You’re going to understand:

- what advance payment actually means in real export transactions

- how it works step by step

- where it fits among other export payment terms

- and when you should actually use it

If you’re serious about building a sustainable export business, this is one of the first things you need to get right.

Table of Contents

What Is Advance Payment in Export Business?

Let’s strip this down to basics.

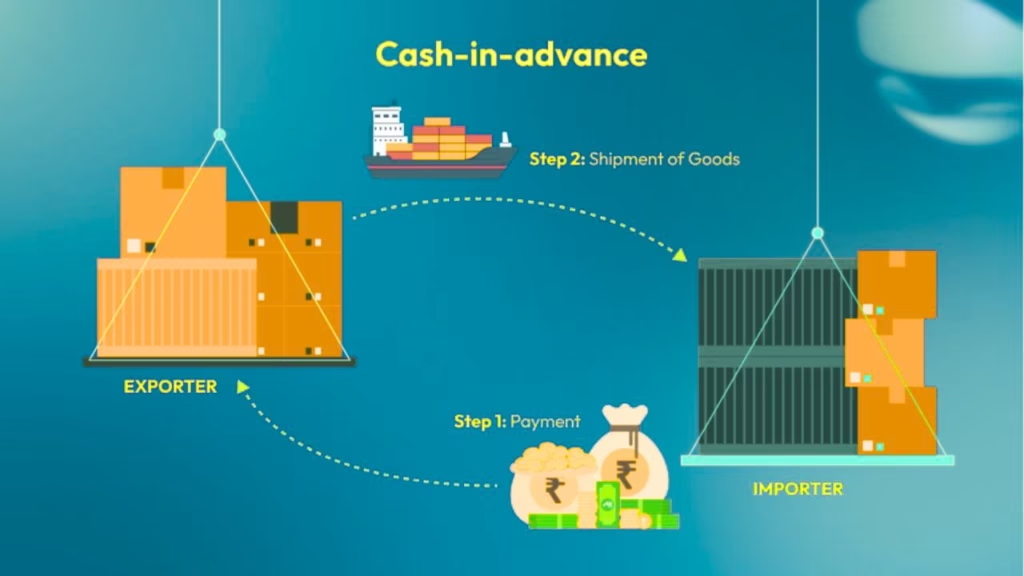

Advance payment in export business means the buyer pays you before you ship the goods. That’s it. Money comes first. Shipment comes later.

Depending on the deal, this payment can be:

- Full advance payment – 100% paid before shipment

- Partial advance payment – a portion paid upfront (like 30% or 50%), with the rest paid later

In practical terms, once the payment reflects in your bank account, you move ahead with production or dispatch. Until then, nothing moves.

This is why advance payment is often called:

- cash in advance payment term

- or simply advance payment term in export

Now let’s talk about how the money actually moves.

In most export transactions, advance payment is received through:

- TT (Telegraphic Transfer)

- SWIFT remittance

- International wire transfer

These are direct bank to bank transfers, which makes the process straightforward and fast compared to other payment methods. If you’re trying to understand the advance payment meaning in one line, here it is

It’s a payment method where the exporter eliminates non-payment risk by receiving money before shipping the goods. And that single shift changes everything about how safe or risky your export business is.

Advance Payment Term Meaning

Let’s clear the confusion properly, because most people overcomplicate this. Advance payment terms mean you get paid before you ship. No exceptions.

There is:

- no credit period

- no waiting for documents to be accepted

- no chasing the buyer after shipment

Once the money hits your account, you move. Until then, you don’t. That’s why this method is also called cash in advance in export. The logic is brutally simple payment first, performance later. Now compare that with how most other export payment terms work.

In post shipment methods:

- you ship goods first

- documents go through banks

- buyer reviews or accepts documents

- payment comes later

This means you’re already exposed before you see the money. With advance payment, that entire chain disappears.

You remove dependency on:

- buyer behavior

- document acceptance

- bank processing delays

you’re not waiting to get paid after delivery, you’re deciding to get paid before taking any risk.

That’s the core difference.

How Advance Payment Works (Step by Step Process)

Now let’s break down the export advance payment process the way it actually happens in real transactions.

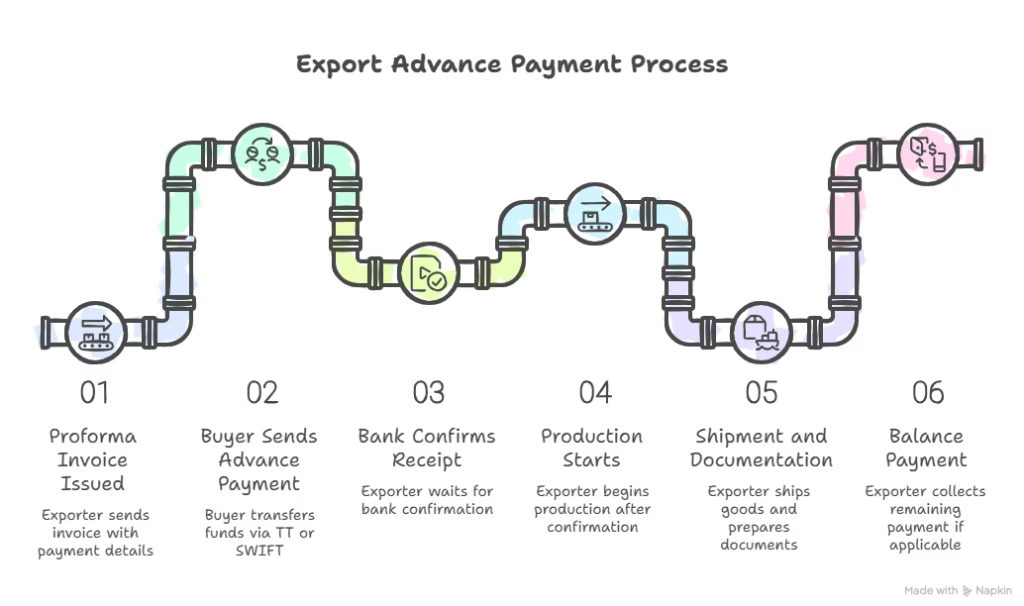

Step 1: Proforma Invoice is Issued

You send a proforma invoice to the buyer with:

- product details

- price

- advance percentage (full or partial)

- bank details

This is not just a formality. It sets the payment expectation clearly.

Step 2: Buyer Sends Advance Payment

The buyer transfers money through:

- TT (Telegraphic Transfer)

- SWIFT

- international wire transfer

At this point, the deal becomes serious. No payment, no movement.

Step 3: Bank Confirms Receipt

You don’t rely on screenshots or buyer messages.

You wait for:

- actual credit in your bank account

- confirmation from your bank

This is where most beginners mess up. They trust “payment sent” instead of “payment received”.

Step 4: Production or Order Processing Starts

Only after confirmation, you:

- begin production

- prepare goods

- arrange packaging

You’re now working with secured funds, not assumptions.

Step 5: Shipment and Documentation

Once goods are ready:

- shipment is executed

- export documents are generated (invoice, packing list, etc.)

- documents are submitted to your bank if required

Step 6: Balance Payment (If Partial Advance)

If it’s not 100% advance:

- remaining amount is collected before shipment or against documents

This depends on your agreed terms. If someone asks “how advance payment works in export”, the clean answer is:

You secure payment → confirm funds → execute order → complete shipment.

No chasing. No dependency. No surprises.

Why Advance Payment Matters More Than You Think

Most people underestimate how fragile export transactions actually are. On paper, everything looks smooth. You find a buyer, agree on price, ship the goods. Done.

Reality is messier.

- Payments get delayed.

- Buyers go silent after shipment.

- Documents get rejected for small errors.

- Banks hold payments longer than expected.

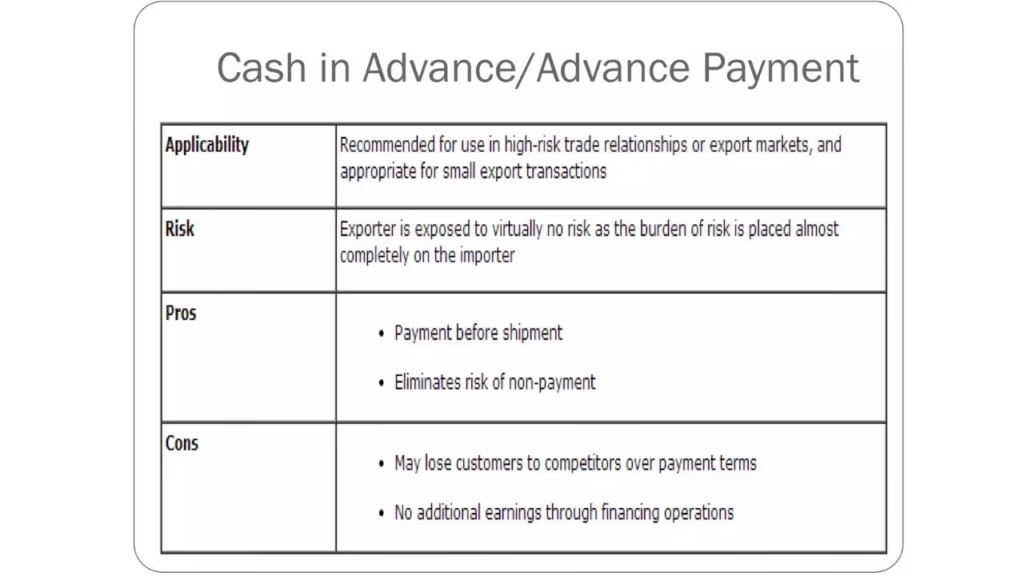

And in the worst cases, the buyer simply doesn’t pay. This means you can do everything right operationally and still lose money financially. That’s why advance payment isn’t just another option in export. It’s a survival tool, especially when you’re starting out.

As a beginner, you don’t have:

- strong legal backup in foreign countries

- deep relationships with buyers

- enough cash flow to absorb losses

So taking unnecessary payment risk is just bad judgment. Advance payment flips that situation. Instead of hoping the buyer pays after shipment, you secure your position before you commit resources. It won’t make every deal easier. Some buyers will push back. But it will make your business far more stable.

And early on, stability matters more than volume.

Advantages of Advance Payment in Export

Let’s cut the fluff and get straight to what actually matters.

1) Zero Payment Risk

This is the biggest advantage. You already have the money before shipping.

There’s no:

- chasing payments

- dependency on buyer honesty

- uncertainty after dispatch

From a risk standpoint, this is as safe as it gets.

2) Strong Cash Flow

Exporting isn’t cheap.

You’re paying for:

- raw materials

- packaging

- logistics

- documentation

With advance payment:

- you’re not using your own capital

- you’re not depending on loans

- your working capital cycle stays healthy

That’s a major advantage most beginners ignore.

3) No LC or Bank Complexity

Letter of Credit sound secure but

They come with:

- heavy documentation

- strict compliance

- bank charges

- delays due to discrepancies

Advance payment removes all of that. No complex bank coordination. No unnecessary costs.

4) Faster Execution

Once payment is received:

- production starts immediately

- no waiting for approvals

- no back and forth with banks

This speeds up the entire export cycle. Time saved here directly improves your operational efficiency.

5) Better Buyer Filtering

This is underrated, but critical.

Buyers who agree to advance payment are usually:

- serious

- financially capable

- committed to the order

Casual or risky buyers hesitate or disappear. What this really does is filter your pipeline. You end up working with better quality clients without trying too hard.

If you’re looking at the advantages of advance payment in export or the real benefits of advance payment, it comes down to this, you remove uncertainty, strengthen cash flow, and deal only with serious buyers. That combination is what makes it powerful.

Disadvantages of Advance Payment

Let’s not pretend this method is perfect. It’s safe for you, but that safety comes at a cost.

1) Buyer Resistance

Many buyers will push back immediately.

From their perspective:

- they’re taking all the risk

- they’re paying before seeing the goods

- they don’t know if you’ll deliver as promised

So when you ask for full advance, expect hesitation especially from first time buyers.

2) Reduced Competitiveness

Here’s the uncomfortable truth.

If your competitors offer:

- credit terms

- partial payments

- flexible options

and if you insist on 100% advance, you will lose some deals. Not because your product is bad, but because your terms are stricter.

That’s the trade-off:

- more safety = fewer deals

- more flexibility = more risk

You need to decide where you stand.

3) Trust Barrier

Advance payment exposes one major weakness early. If your business doesn’t look credible, buyers won’t pay upfront. No strong presence, no proof, no clear communication then advance payment becomes almost impossible to negotiate.

So the real issue isn’t just the payment term. It’s whether you’ve built enough trust to justify it. If you ignore these disadvantages, you’ll make bad decisions. Advance payment works, but only when you understand where it fails.

Advance Payment vs Other Export Payment Terms

This is where things get practical.

You don’t choose payment terms based on theory. You choose based on risk, trust, and deal size.

Let’s break down the export payment terms comparison properly.

Advance Payment vs Letter of Credit (LC)

Advance Payment:

- money received before shipment

- no bank dependency

- minimal documentation

- fastest execution

Letter of Credit (LC):

- bank guarantees payment

- strict documentation rules

- higher costs (opening, amendment, discrepancies)

- delays if documents don’t match perfectly

This means:

- Advance payment = simpler and safer for exporter

- LC = structured safety but operational headache

If you’re comparing LC vs advance payment, the real difference is:

- LC reduces risk through banks

- advance payment removes risk completely upfront

Advance Payment vs TT (Post Shipment)

Both use bank transfers, but timing changes everything.

Advance TT:

- payment before shipment

- no exposure to buyer risk

Post-Shipment TT:

- goods shipped first

- payment comes later

- depends on buyer honesty

This is where beginners get trapped. They hear “TT payment” and assume it’s safe. It’s not.

If it’s post-shipment TT:

- you’ve already shipped

- you’re waiting for money

- you’re exposed

So in this comparison:

- Advance payment = controlled and secure

- Post-shipment TT = faster than LC, but still risky

Advance Payment vs DP / DA

Now we’re getting into higher risk territory.

DP (Documents Against Payment):

- buyer pays to receive documents

- goods already shipped

DA (Documents Against Acceptance):

- buyer accepts documents

- pays later (credit period)

What this means in reality:

- DP = moderate risk (still dependent on buyer action)

- DA = high risk (you’re giving credit without control)

Compared to that:

- Advance payment = zero exposure before shipment

If you’re looking at DP DA vs advance payment, the gap is clear:

- DP/DA = payment uncertainty exists

- Advance payment = payment certainty before execution

Bottom line from this export payment terms comparison:

Advance payment gives you control.

Everything else introduces some level of dependency.

The only question is how much risk you’re willing to tolerate.

When Should You Use Advance Payment?

Most people treat advance payment like a rule instead of a strategy. You don’t use it everywhere. You use it where risk is high and control matters.

1) New Buyers

If you don’t know the buyer, you don’t trust the buyer. Simple. No track record. No past transactions. No leverage if something goes wrong. Advance payment forces commitment upfront. If they’re serious, they’ll pay. If they disappear, you just avoided a bad deal.

2) High Risk Countries

Not all markets are equal.

Some countries have:

- weak legal enforcement

- payment delays as a norm

- higher fraud probability

In these cases, offering credit terms is just careless. Advance payment protects you when recovery options are limited or practically useless.

3) Custom Products

If you’re making something specific for a buyer, you’re exposed the moment production starts.

You can’t easily:

- resell the product

- modify it for another buyer

So if the buyer backs out, you’re stuck with dead inventory. Advance payment ensures you’re not funding someone else’s order blindly.

4) Small Orders

This is where people overthink.

For low value shipments:

- the effort of recovery isn’t worth it

- legal action makes no sense

- chasing payment wastes time

Advance payment keeps things clean and efficient.

What this really comes down to:

Use advance payment when the downside of not getting paid is higher than the upside of closing the deal. If you ignore that, you’ll win orders and lose money at the same time.

Is Advance Payment Really Risk Free?

Short answer: for exporters, mostly yes.

But don’t be lazy with that conclusion. Because risk doesn’t disappear. It just moves from you to the buyer.

Exporter Side: Minimal Risk

Once payment is received:

- no non-payment risk

- no dependency on buyer after shipment

- no financial uncertainty

That’s why advance payment is considered the safest option for exporters.

Importer Side: High Risk

From the buyer’s perspective:

- they’ve paid without receiving goods

- they’re trusting you to deliver

- they have limited control if something goes wrong

That’s a real risk, not a theoretical one.

The Reality Most People Ignore

Advance payment is not “risk free trade”.

It’s a risk transfer.

- In LC → bank shares risk

- In DP/DA → exporter takes risk

- In advance payment → importer takes risk

That’s the actual equation. If you want advance payment, you need to justify it.

Not by arguing.

But by:

- clear communication

- professional documentation

- consistent delivery

Because the moment the buyer feels unsafe, they won’t agree. And if you can’t get buyers to trust you, advance payment won’t work no matter how “safe” it is on paper.

Partial Advance Payment: The Practical Middle Ground

Full advance sounds great in theory. In reality, many buyers won’t agree, especially in the first deal. This is where partial advance payment in export becomes the smart move.

Instead of pushing for 100%, you structure the deal like this:

- 30% advance before production

- 70% before shipment or against documents

This is what most real export deals look like when both sides are trying to reduce risk.

When Should You Use Partial Advance?

Use this approach when:

- the buyer is new but shows genuine intent

- order value is moderate

- buyer pushes back on full advance

- you want to close the deal without taking full exposure

It’s not about compromising blindly. It’s about adjusting without losing control.

Why It Works Better in Real Deals

Here’s the practical advantage.

- You still secure upfront commitment (advance)

- Buyer feels less pressure compared to full payment

- Risk is shared instead of dumped entirely on one side

This balance increases your chances of closing deals without exposing yourself fully. Also, it signals professionalism. You’re not rigid, but you’re not careless either. If you’re thinking in terms of advance payment percentage in export, there’s no fixed rule.

But common structures are:

- 20%–30% advance for standard goods

- 40%–50% for customized or higher risk orders

The exact number depends on:

- buyer credibility

- product type

- market conditions

Partial advance payment is how real exporters operate when full advance isn’t practical but risk still needs to be controlled.

Documents Required for Advance Payment in Export

One reason advance payment works well is because the documentation is simple. But simple doesn’t mean optional. If you skip this, you create problems later with banks and compliance.

Let’s break down the key documents for advance payment export.

1) Proforma Invoice

This is the starting point.

Before payment, you issue a proforma invoice with:

- product details

- quantity and price

- advance amount or percentage

- bank details

This document sets the payment terms clearly. No ambiguity.

2) FIRC (Foreign Inward Remittance Certificate)

Once you receive the advance, your bank issues FIRC.

It acts as:

- proof of foreign payment received

- record for compliance and accounting

Without this, your transaction isn’t properly documented.

3) Shipping Documents

After production and shipment, you generate standard export documents.

Like:

- commercial invoice

- packing list

- bill of lading / airway bill

Even if payment is already received, documentation is still mandatory.

4) e-BRC (Electronic Bank Realization Certificate)

This is issued after export proceeds are realized and reported through the banking system.

It is important for:

- export compliance

- claiming incentives

- closing the transaction officially

If someone is searching for export documentation for advance payment, the key takeaway is the process is simple, but you still need clean documentation to stay compliant with RBI and banking rules. Ignore that, and you’ll face issues not with buyers, but with your own system.

RBI & FEMA Rules for Advance Payment in India

Most exporters ignore this part until something goes wrong. That’s a mistake. You’re not just dealing with a buyer. You’re dealing with RBI compliance, FEMA regulations, and banking systems. If you don’t follow the rules, your payment can get stuck or flagged.

Let’s break down the important RBI rules for advance payment in export without unnecessary jargon.

1) Shipment Timeline (Critical Rule)

If you receive advance payment, you are expected to complete the shipment within the allowed time frame.

- Current rule shipment should happen within 3 years from the date of receiving advance

- If you fail to ship, banks may question the transaction

This isn’t optional. It’s tracked.

2) Export Realization Rules

Even though you already received an advance, the transaction still needs to be formally completed.

- Export proceeds must be properly realized and reported

- Typically, the export cycle must be completed within 15 months from the date of export

What this means is:

- payment alone doesn’t close the transaction

- documentation + reporting completes it

3) Interest Limits

If there’s any interest component involved (rare, but possible in structured deals)

- It must stay within limits defined by RBI

- Generally capped around LIBOR + 100 basis points

For most small exporters, this won’t apply. But if you scale, you need to know it exists.

4) Compliance Basics

To stay clean under FEMA advance payment rules:

- Route payments through an authorized dealer bank (AD bank)

- Maintain proper documentation (invoice, FIRC, shipping docs)

- Ensure timely shipment and reporting

If you skip compliance:

- your bank can block transactions

- you may face penalties

- future exports become harder

Advance payment is simple operationally, but it still sits inside a strict regulatory framework. Ignore that, and you create problems for yourself.

Risks & How to Mitigate Them

Let’s be clear.

Advance payment reduces risk, but it doesn’t eliminate all problems. Different risks still exist, you just need to manage them properly.

1) Buyer Non Trust

Biggest barrier.

Buyers hesitate because:

- they’re paying before receiving goods

- they don’t know if you’ll deliver

- they don’t have control after payment

If you can’t build trust, you won’t get advance deals.

2) Order Cancellation After Payment

Yes, this happens.

Even after paying, buyers may:

- change requirements

- delay confirmations

- create unnecessary friction

If you’re not structured, this turns into operational chaos.

3) Compliance Issues

This is the silent risk.

- delayed shipment

- missing documents

- incorrect reporting

These don’t affect the buyer. They hit you, through banks and regulators.

How to Mitigate These Risks

Now the practical part. No theory.

1) Strong Contracts + Incoterms

Don’t rely on WhatsApp conversations.

Use:

- clear written agreements

- defined delivery timelines

- proper Incoterms (FOB, CIF, etc.)

This reduces ambiguity and protects both sides.

2) ECGC Insurance

If you’re scaling or dealing with riskier markets

- ECGC (Export Credit Guarantee Corporation) provides coverage

- protects against payment and country risk

It’s not mandatory, but it adds a safety layer when deals get bigger.

3) Buyer Due Diligence

Stop trusting blindly.

Check:

- company background

- website and business activity

- trade references

A quick check upfront saves you from bigger issues later. Advance payment reduces financial risk, but you still need systems to manage trust, execution, and compliance. If you ignore that, you won’t lose money but you will lose control.

Common Mistakes Exporters Make

This is where most exporters don’t like the truth. Advance payment works, but only if you don’t screw up the basics.

1) Asking Full Advance Blindly

Some exporters treat 100% advance like a default setting. No context. No flexibility. No reading the situation.

Result:

- serious buyers walk away

- deals die before they start

You don’t demand full advance. You justify it based on risk. If the buyer is new, product is customized, or country risk is high then yes, push hard. If not, use partial advance and close the deal.

2) Poor Communication

You can’t ask for upfront money and then communicate like an amateur.

Common mistakes:

- slow replies

- vague answers

- no clarity on timelines

From the buyer’s side, this screams risk. If you want advance payment.

Your communication needs to feel:

- structured

- responsive

- reliable

Otherwise, they won’t pay. Simple.

3) Delaying Shipment After Payment

This one destroys trust faster than anything. You’ve taken the buyer’s money. Now they’re watching every move.

If you:

- delay production

- miss timelines

- stop updating

you’re done. Not just for this deal, but for future referrals too. Advance payment gives you safety. It also puts you under pressure to deliver properly.

4) Ignoring Compliance

A lot of exporters think:

“Money received, work done.”

Wrong. If you:

- delay shipment beyond allowed timelines

- don’t submit documents properly

- ignore bank requirements

You’ll face issues from your own system, not the buyer. And those problems don’t go away easily. Advance payment protects you from the buyer. It doesn’t protect you from your own mistakes.

Does Advance Payment Work With Foreign Buyers?

Short answer: yes.

But not automatically. Whether it works or not depends on how you position it, not just what you ask.

When Buyers Agree

Buyers are more likely to accept advance payment when:

- order value is small

- product is in demand or specialized

- you present yourself professionally

- communication is clear and fast

In these cases, the buyer sees low risk and moves forward.

When Buyers Push Back

Pushback usually happens when:

- you’re a new supplier with no track record

- order value is high

- product is easily available elsewhere

- you sound uncertain or unstructured

At that point, from their side, paying upfront feels unnecessary and risky.

How to Convince Them

You don’t convince buyers by arguing. You convince them by reducing their doubt.

Focus on:

- Clarity → clear quotation, clear timelines, no confusion

- Proof → company details, past work, certifications if available

- Structure → proper invoices, formal communication

- Flexibility → offer partial advance if needed

What this means:

You’re not selling the product first. You’re selling confidence.

Once that’s established, advance payment becomes a lot easier to close. If buyers consistently refuse advance payment, the issue is not the method. It’s how you’re presenting yourself.

Should Beginners Start with Advance Payment?

Yes. But don’t be stupid about it.

Starting with advance payment is the safest move when you’re new. You don’t have experience, systems, or backup to handle losses. So taking payment upfront protects you while you’re still figuring things out.

But here’s where people mess up.

They either:

- become too rigid and lose deals

- or become too flexible and take unnecessary risk

You need a middle path.

The Right Strategy: Start Strict → Loosen Later

In the beginning:

- aim for 100% advance or strong partial advance

- prioritize safety over volume

- work only with buyers who agree to your terms

As you gain:

- experience

- repeat buyers

- better cash flow

you can gradually adjust:

- move to partial advance

- offer better terms to trusted buyers

- negotiate based on relationship, not desperation

In the early stage, your goal is not maximum sales. It’s controlled growth. Advance payment gives you that control. Once your foundation is strong, you earn the right to be flexible.

Final Take

Advance payment is not outdated. It’s not unprofessional. And it’s definitely not a barrier to growth.

It’s protection.

It protects your:

- cash flow

- time

- business stability

The mistake is not using it. The mistake is using it without thinking. If you apply it blindly, you lose deals.

If you avoid it completely, you take unnecessary risk.

So the real answer is simple:

Use advance payment strategically, not emotionally. That’s how you stay in the game long enough to actually grow.

FAQs

1) Will foreign buyers agree to advance payment?

Some will, some won’t. It depends on how you position yourself. Buyers are more likely to agree when the order value is small, the product is in demand, and you come across as professional and reliable.

They usually push back when you’re new, the order size is large, or they have multiple supplier options. If you keep hearing no, the issue is rarely the payment method. It’s how you’re presenting your business.

2) Is advance payment safe in export?

For exporters, yes. It’s the safest option because you receive the money before shipping the goods, which removes non-payment risk completely. But calling it “risk-free” is misleading. The risk doesn’t disappear, it shifts to the buyer. That’s why trust and communication play a big role in making this method work.

3) What happens if shipment is delayed?

Delays are not uncommon in export. What matters is how you handle them. If there’s a delay, you need to inform the buyer early and give a clear revised timeline. If delays go on for too long, banks may start asking questions and compliance issues can come up. The biggest mistake is going silent. That’s what breaks trust, not the delay itself.

4) Can I take 100% advance payment?

Yes, you can. There’s no restriction on taking full advance payment. But whether it works depends on the situation. For new buyers or higher-risk deals, it makes sense. For larger or long-term relationships, pushing for 100% can hurt your chances of closing the deal. That’s where partial advance becomes more practical.

5) Do I need to issue any document after receiving advance payment?

Yes, and ignoring this creates problems later. You should already have a proforma invoice before receiving payment. After the payment comes in, your bank issues FIRC as proof of remittance. Once the shipment is done, proper export documents complete the process. This isn’t just paperwork, it’s what keeps your transaction compliant and clean.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

2 thoughts on “What Is Advance Payment in Export? Meaning, Process & Real Risks Explained”