Venturing into international trade offers immense opportunities access to large markets, foreign currency earnings, and the potential for unlimited scaling. However, the reality is far less glamorous. Exporters often ship goods worth lakhs or crores, wait 30 to 180 days for payment, and navigate the complexities of dealing with buyers in unfamiliar legal and political environments.

One delayed payment, a bankrupt buyer, or a sudden policy restriction in the importing country can wipe out months of profit. This is where ECGC insurance becomes a game changer for Indian exporters. The Export Credit Guarantee Corporation of India (ECGC), a government backed enterprise and the seventh largest credit insurer globally, provides a crucial safety net for businesses and banks engaged in global commerce.

ECGC insurance shields exporters from both commercial and political payment risks, ensuring that they recover a significant portion of their dues even if an overseas buyer fails to pay. In essence, this export credit insurance transforms uncertain global transactions into predictable, manageable business operations.

But Export Credit Guarantee Corporation of India insurance is more than just a defensive tool it’s a strategic advantage. With an active ECGC policy, exporters gain credibility with banks, access easier working capital financing, and confidently expand into new international markets without exposing themselves to major payment risks.

Whether you’re a first time exporter, a growing MSME(Micro, Small, and Medium Enterprises), a service provider, or a large project supplier, ECGC coverage empowers you to turn global expansion into a practical and secure growth strategy.

This guide will explore the essential ECGC products and explain how leveraging this export credit insurance framework can protect your business while unlocking new opportunities in international trade. By the end, you’ll understand why ECGC insurance is not just a necessity but a foundation for building a robust and thriving export business.

Table of Contents

What is ECGC Insurance?

The ECGC insurance meaning starts with a simple idea that international trade carries payment risk, and Export Credit Guarantee Corporation of India exists to absorb a large portion of that risk. Export Credit Guarantee Corporation of India insurance is an export credit insurance system that protects Indian exporters and lending banks against losses arising from buyer default, delayed payments, insolvency, or political disruptions in the importing country.

The organization responsible for providing this protection is the Export Credit Guarantee Corporation of India, a government owned enterprise operating under the Ministry of Commerce and Industry. Its primary role is to strengthen India’s export ecosystem by offering credit risk insurance covers, guarantees to banks, and trade related financial risk advisory services.

By doing this, the Export Credit Guarantee Corporation of India enables exporters to trade confidently even in unfamiliar or high risk markets.

Government ownership gives Export Credit Guarantee Corporation of India a strong regulatory and financial foundation, making its guarantees highly trusted by banks and financial institutions. When exporters hold an active ECGC policy, banks face significantly reduced lending risk, which improves exporters access to working capital, packing credit, and post shipment financing.

Protection works at two levels. Exporters receive coverage against commercial risks such as buyer bankruptcy or refusal to pay, while banks receive guarantees that secure the loans extended to exporters. This dual layer protection stabilizes the entire export financing chain, allowing businesses to focus on market expansion rather than payment uncertainty.

History of Export Credit Guarantee Corporation of India

The ECGC history dates back to July 1957, when the Government of India established the Export Risks Insurance Corporation (ERIC) to support exporters facing growing international trade risks. As India’s export economy expanded, the organization evolved in both structure and mandate.

In 1964, ERIC was renamed the Export Credit and Guarantee Corporation Ltd., reflecting its broader role in providing both insurance and credit guarantees. Later, in 1983, it adopted the name Export Credit Guarantee Corporation of India Ltd, aligning its identity more closely with its national export promotion mission. In 2014, the institution formally became ECGC Limited.

Today, Export Credit Guarantee Corporation of India stands among the largest export credit insurers globally in terms of export coverage, supporting thousands of exporters and financial institutions across multiple sectors. The organization operates nationwide through regional and branch offices, with its headquarters located at the ecgc mumbai office, which functions as the strategic and administrative center of operations.

Over decades, Export Credit Guarantee Corporation of India has grown from a risk protection initiative into a critical pillar of India’s export infrastructure, playing a central role in enabling exporters to enter global markets with confidence while strengthening the country’s international trade competitiveness.

Purpose of ECGC Insurance

The primary purpose of ECGC insurance is to provide export payment risk protection so exporters can operate in global markets without exposing their businesses to unpredictable financial losses. International trade involves multiple uncertainties such as unfamiliar buyers, long credit periods, currency fluctuations, and geopolitical instability.

Export Credit Guarantee Corporation of India addresses these uncertainties by transferring a significant portion of the risk from exporters and banks to a government backed insurance framework. One major objective is protection against commercial risks. These include situations where the foreign buyer becomes bankrupt, refuses to accept the shipment, delays payment beyond the agreed credit period, or simply defaults due to financial failure.

Without insurance, exporters must absorb the entire loss. With ECGC coverage, a large percentage of the unpaid amount is reimbursed, reducing the financial impact. Another equally important function is coverage against political risks. Events such as war, import restrictions, sudden foreign exchange shortages, government payment bans, or civil unrest in the buyer’s country can prevent legitimate payments from reaching exporters.

ECGC insurance ensures that exporters are compensated even when payment failure occurs due to country level disruptions rather than buyer level issues. Beyond risk protection, ECGC plays a critical role in improving export financing. Banks are more willing to extend packing credit, post shipment finance, and export working capital when transactions are insured.

This improves liquidity for exporters and enables them to scale operations faster. One of the strongest export credit insurance benefits is that policies typically cover around 80-90% of potential losses, providing substantial financial security while still encouraging responsible trade practices.

How ECGC Insurance Works

Understanding the ecgc policy process helps exporters see how coverage operates from application to claim settlement. The system is designed to evaluate buyer risk, insure shipments, and compensate exporters if payment problems arise.

Exporter Applies for Policy

The exporter first applies for a suitable ECGC policy depending on the type of export activity, shipment frequency, and credit period. Basic documentation includes exporter registration details, shipment turnover estimates, and information about major overseas buyers.

Buyer Credit Assessment

After the policy is issued, exporters submit details of specific overseas buyers for credit limit approval. ECGC evaluates the financial strength, payment history, and country risk associated with the buyer before assigning an approved credit limit. This step ensures that exporters transact within insured limits.

Shipment and Coverage

When the credit limit is approved, shipments to the buyer are covered automatically. The exporter must still follow policy terms such as reporting shipments, maintaining documentation, and adhering to payment timelines.

During this period, the exporter continues normal trade operations while the policy safeguards against payment failure.

Claim Settlement

If the buyer fails to pay within the specified waiting period, the exporter can file an export credit insurance claim with supporting documents such as invoices, shipping proofs, and payment follow up records. After verification, ECGC compensates the insured percentage of the loss and may also assist in recovery proceedings from the defaulting buyer.

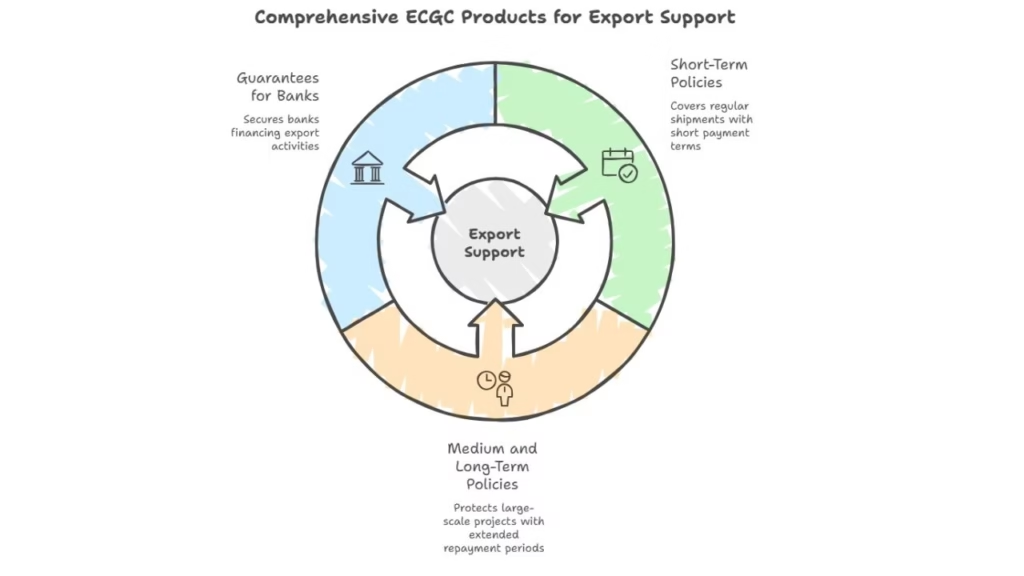

Types of ECGC Products

To address the diverse needs of exporters, ECGC offers multiple ecgc products designed for different transaction sizes, export durations, and financing requirements.

These ecgc export policies form a structured set of export credit insurance schemes that cover everything from small recurring shipments to long term infrastructure projects and bank backed export financing.

Short Term Policies

Short term policies are designed for exporters dealing with regular shipments where payment credit periods usually range from a few weeks to up to one year.

Shipment Comprehensive Risk (SCR) Policy

This policy covers exporters making frequent shipments to multiple overseas buyers. It provides continuous protection against both commercial and political risks across the exporter’s entire insured turnover, making it one of the most widely used ECGC products for routine export businesses.

Single Shipment Policy (SSP)

This policy is suitable for exporters handling occasional or one time export transactions. Instead of covering the entire turnover, it insures a specific shipment against payment risks, offering flexibility for businesses that export irregularly.

Service Policies

Service exporters such as IT companies, consultants, or technical service providers can obtain coverage under service export policies. These protect receivables arising from international service contracts, ensuring that payment defaults do not affect operational cash flow.

Medium and Long Term Policies

For large scale contracts where repayment periods extend beyond one year, Export Credit Guarantee Corporation of IndiaExport Credit Guarantee Corporation of Indiaprovides specialized long duration coverage.

Project Export Coverage

This policy protects exporters involved in supplying machinery, equipment, or turnkey projects with long credit periods. It safeguards against both buyer default and country level risks over the extended repayment cycle.

Construction Works Policy (CWP)

Designed for contractors executing overseas civil construction or infrastructure projects, this policy covers risks associated with payment failures during project execution and post completion payment schedules.

Guarantees for Banks

In addition to exporter focused policies, several ECGC products are structured as guarantees that protect banks financing export activities.

Packing Credit Guarantee

Banks providing pre shipment finance to exporters receive protection against exporter default, encouraging them to extend working capital support more confidently.

Performance Guarantee

This protects banks when they issue performance guarantees on behalf of exporters participating in international contracts or tenders.

Factoring Guarantee

This facility covers financial institutions engaged in export receivable factoring, reducing the risk associated with advancing funds against export invoices.

Together, these structured export credit insurance schemes create a comprehensive ecosystem that protects exporters, strengthens bank confidence, and supports India’s international trade expansion.

Benefits of ECGC Insurance for Exporters

The real value of ECGC insurance lies in its ability to transform uncertain global trade transactions into predictable business operations. Among the key export insurance benefits is direct protection from buyer default.

If an overseas buyer becomes bankrupt, refuses to pay, or delays payment beyond agreed timelines, Export Credit Guarantee Corporation of India compensates a significant portion of the loss, preventing severe cash flow disruption.

Another major ecgc advantage is improved access to bank financing. Exporters holding insured receivables are viewed as lower risk borrowers, which often results in easier approval of packing credit, post-shipment finance, and export working capital limits.

This financing support enables exporters to handle larger orders without liquidity constraints.

ECGC coverage also allows businesses to expand into new or higher risk markets. Without insurance, exporters often restrict trade to familiar buyers or low risk countries. With coverage in place, they can confidently approach new international customers, diversify revenue sources, and reduce dependence on limited markets.

Finally, insurance coverage supports more competitive pricing strategies. Since a large share of payment risk is insured, exporters can offer better credit terms to international buyers without exposing themselves to excessive financial danger.

This flexibility improves their competitiveness in global tenders and long term supply contracts, strengthening their position in international trade.

Benefits for Banks and Financial Institutions

ECGC insurance does not only protect exporters; it plays a critical role in strengthening the banking system that finances international trade. One of the biggest advantages is the export credit guarantee for banks, which significantly reduces the lending risk associated with export transactions.

When banks finance pre shipment or post shipment export activities, the possibility of exporter default or overseas buyer non-payment can expose them to financial losses. It guarantees absorb a substantial portion of this risk, making export lending safer and more predictable.

Another key benefit is the improvement in overall export credit flow. Because ECGC backed transactions carry lower risk, banks are more willing to extend working capital limits, packing credit, and export bill discounting facilities.

This increases the availability of credit to exporters, particularly small and medium enterprises that might otherwise struggle to secure funding due to limited deposit or short financial histories.

Guarantee protection also strengthens confidence in long term export financing. For large project exports, infrastructure supplies, or overseas service contracts where repayment periods extend over several years, ECGC guarantees provide banks with security against commercial and political risks affecting repayment.

As a result, financial institutions can support larger export transactions without exposing their balance sheets to excessive uncertainty, creating a stable financing ecosystem for international trade.

Who Should Take ECGC Insurance?

In practice, ecgc insurance for exporters is useful across almost every export category, but it becomes especially important for businesses operating with extended credit periods or entering unfamiliar global markets.

New exporters should strongly consider ECGC coverage because they often lack historical buyer payment data and established international credit networks. Insurance allows them to take initial export orders without risking severe financial damage if a buyer fails to pay.

MSME exporters benefit significantly from ECGC policies since smaller businesses typically operate with tighter working capital margins. Even a single payment default can disrupt operations, and insurance ensures continuity of cash flow while also improving access to bank finance.

Service exporters, including IT service providers, consultants, and technical contractors, also face receivable risks when dealing with overseas clients. ECGC policies covering service exports protect their invoices in the same way goods exporters protect shipment payments.

Project exporters handling large engineering, construction, or equipment supply contracts require long-term protection because payment cycles often stretch over months or years. ECGC coverage secures these high value transactions, making it possible for exporters to undertake complex international projects with manageable financial exposure.

ECGC Policy Eligibility and Documents Required

Understanding ecgc policy eligibility is straightforward. ECGC policies are designed for legally registered exporters who are engaged in the export of goods, services, or project supplies and who extend credit terms to overseas buyers.

Eligibility primarily depends on export registration status, financial standing, and the ability to provide verifiable buyer transaction information.

Export Registration

Applicants must be registered exporters operating under Indian export regulations. Businesses involved in manufacturing, merchant exporting, service exports, or project exports can apply, provided their export activities are genuine and documented.

IEC Requirement

A valid Import Export Code (IEC) issued by the Directorate General of Foreign Trade is mandatory. The IEC functions as the primary identification number for all international trade transactions and is essential for obtaining ECGC coverage.

Financial Documents

Exporters are required to submit financial statements such as balance sheets, profit and loss accounts, and turnover details. These documents help ECGC assess the financial stability of the applicant and determine appropriate policy coverage limits.

Buyer Details

Information about overseas buyers, including transaction value, payment terms, country location, and past payment history (if available), must be provided for credit limit approval. This enables ECGC to evaluate risk exposure before granting coverage for shipments to specific buyers.

Meeting these documentation requirements ensures faster policy approval and smoother credit limit processing for insured transactions.

ECGC Premium Structure (How Pricing Works)

The export credit insurance cost under ECGC policies is calculated using a structured risk based pricing model rather than a fixed universal fee. The ecgc premium rate varies depending on several factors that determine the level of payment risk associated with the export transaction.

Factors Affecting Premium

Premiums are influenced by shipment volume, credit period length, type of goods or services exported, and the nature of the selected ECGC policy. Higher exposure transactions or longer credit durations generally attract higher premium rates because of increased default probability.

Country Risk Rating

It assigns risk categories to importing countries based on political stability, economic conditions, foreign exchange availability, and historical payment behavior. Exports to low risk countries typically carry lower premium rates, while shipments to politically unstable or economically volatile regions may involve higher insurance charges.

Buyer Risk Rating

The financial strength and creditworthiness of the overseas buyer also play a significant role. Buyers with strong financial records and reliable payment histories receive better risk ratings, reducing the premium payable for shipments made to them.

Turnover Based Premium

For exporters using turnover policies such as comprehensive shipment coverage, premiums are often calculated as a percentage of the insured export turnover during the policy period. This structure allows exporters to align insurance cost directly with export volume, ensuring scalable pricing as their international business grows.

ECGC Claim Process

The purpose of ECGC coverage becomes most visible when a payment default occurs. Understanding how export insurance claims work ensures exporters can recover losses quickly and correctly. The ecgc claim settlement process follows a structured timeline designed to verify the default, compensate the exporter, and initiate recovery actions.

When Claim Can Be Filed

A claim can be filed when the overseas buyer fails to make payment within the agreed credit period and the additional waiting period specified under the policy. Claims may also arise if the buyer becomes bankrupt, refuses to accept goods without valid reasons, or if political events in the importing country prevent payment transfer.

Waiting Period

ECGC policies include a defined waiting period after the due date of payment. This period allows time for normal recovery efforts such as reminders, negotiations, or bank intervention. Only after the waiting period ends can the exporter formally initiate the claim process.

Claim Settlement Timeline

Once the claim application and supporting documents are submitted, ECGC reviews shipment details, payment records, buyer status, and compliance with policy terms. After verification, compensation for the insured portion of the loss is released according to the approved coverage percentage.

Settlement timelines vary depending on case complexity but are generally structured to ensure timely exporter support.

Recovery Assistance

Even after settlement, ECGC continues recovery efforts from the defaulting buyer or relevant authorities in the importing country. If any amount is later recovered, it is shared between Export Credit Guarantee Corporation of India and the exporter based on the policy agreement.

This recovery support reduces the long term financial burden on exporters while improving the effectiveness of international debt collection.

Export Credit Guarantee Corporation of India Online Services

To simplify policy management and reduce paperwork, ECGC provides a comprehensive digital platform offering multiple ecgc online services for exporters, banks, and policyholders.

Login Process

Users can access the official portal through the ecgc login section by registering their exporter or institutional account. After authentication, policyholders can manage policies, submit reports, check buyer credit limits, and track claim status directly from their dashboard.

Online Policy Application

Exporters can apply for suitable policies through the online portal by uploading required documents, selecting policy types, and providing export turnover estimates. This digital process significantly reduces approval time compared to traditional manual applications.

Online Claim Filing

In the event of payment default, exporters can initiate claim submission through the portal by uploading shipment invoices, payment follow up records, and buyer communication proofs. Online submission ensures faster document processing and smoother claim tracking.

Digital Services Portal

The ECGC digital services system integrates policy management, credit limit requests, claim processing, and policy renewal functions into a centralized platform. This allows exporters to handle all insurance-related activities electronically, improving transparency, speed, and operational efficiency in export risk management.

ECGC Offices and Contact Information

The Export Credit Guarantee Corporation operates through a nationwide network of regional and branch offices to support exporters, banks, and policyholders. The headquarters, commonly referred to as the ecgc mumbai office, serves as the central administrative and policy decision making hub where national-level operations, risk evaluation frameworks, and export credit programs are managed.

In addition to the head office, ECGC maintains regional offices across major export centers such as Delhi, Chennai, Kolkata, Bengaluru, Ahmedabad, and Hyderabad. These offices provide direct assistance for policy applications, buyer credit limit approvals, claim submission support, and exporter advisory services.

Exporters can approach the nearest regional office for faster resolution of operational issues and policy-related queries.

For customer assistance, exporters and financial institutions can access official ecgc contact details through the organization’s website, which provides updated phone numbers, email addresses, and office locations.

Dedicated support teams assist with policy selection, premium clarification, claim procedures, and online portal guidance, ensuring exporters receive both technical and operational support when managing their insurance coverage.

ECGC Career and Recruitment

Apart from export risk protection services, ECGC is also a recognized government sector employer that periodically conducts recruitment for various positions, most notably the Probationary Officer (PO) role.

The recruitment process generally begins with an official notification announcing eligibility criteria, application timelines, examination schedules, and selection procedures. Candidates interested in government insurance and financial risk management careers typically monitor announcements to ecgc po apply within the application window.

After submitting the application, candidates receive the ecgc admit card required to appear for the written examination. The hall ticket, commonly referred to as the ecgc po admit card, is released online and must be downloaded before the exam date.

Many candidates also search for previous recruitment resources such as ecgc po admit card 2022 download to understand exam patterns and selection stages from earlier cycles.

Following the examination and interview process, the organization publishes the ecgc po results on the official portal, listing selected candidates and further joining instructions. One of the major attractions of the position is compensation.

The ecgc probationary officer salary packages typically include basic pay, allowances, performance incentives, and additional government sector benefits, making it a competitive financial services career option. Salary structures are often listed in recruitment notifications and summarized in official ecgc sal list or ecgc sal documents issued for reference.

ECGC vs Private Export Insurance (Comparison)

When exporters evaluate insurance options, an export credit insurance comparison between ECGC and private insurers helps clarify which solution fits their risk profile and financing needs.

Government Backing Advantage

ECGC operates as a government owned institution, which gives its guarantees higher acceptance among Indian banks and financial institutions. Because policies are backed by sovereign credibility, lenders often prefer ECGC covered transactions when extending export credit.

Private insurers, while efficient in certain specialized sectors, may not always provide the same level of institutional acceptance in export financing arrangements.

Coverage Differences

ECGC policies are specifically designed for exporters and banks engaged in international trade, covering both commercial risks such as buyer insolvency and political risks such as import restrictions, currency transfer delays, or geopolitical disruptions.

Some private insurers primarily focus on commercial risk coverage and may offer limited political risk protection depending on the policy structure. ECGC also integrates buyer credit assessment, country risk ratings, and recovery assistance into its coverage framework, making it more aligned with export focused risk management.

Cost Comparison

Premium costs vary based on shipment volume, country risk, and buyer profile in both systems. ECGC pricing is often structured to support export promotion objectives, which can make it more competitive for MSMEs and new exporters.

Private export insurance products may offer customized pricing for large corporations or sector specific transactions, but the absence of government backed guarantees can sometimes lead to stricter underwriting or higher premiums for high risk markets.

Exporters typically evaluate both coverage scope and financing advantages before deciding which policy delivers better overall value.

Real World Example of ECGC Insurance Protection

Understanding how coverage works in practice becomes clearer through real transaction scenarios. These export credit insurance examples illustrate how ECGC protection prevents financial losses when unexpected events disrupt payments.

Example 1: Buyer Bankruptcy Case

An engineering equipment exporter supplies machinery worth several crores to an overseas distributor on a 120 day credit basis. Two months after shipment, the distributor enters bankruptcy proceedings and becomes unable to pay outstanding invoices.

Because the exporter had insured the transaction under an ECGC policy, the unpaid amount qualifies for coverage after the waiting period. Following documentation review and verification, Export Credit Guarantee Corporation of India compensates the insured portion of the invoice value, ensuring the exporter’s cash flow remains stable despite the buyer’s financial collapse.

Example 2: Political Instability Payment Delay Case

A textile exporter ships goods to a buyer located in a country experiencing sudden foreign exchange restrictions due to economic instability. Although the buyer is financially capable of paying, government-imposed currency transfer controls prevent the payment from being remitted to India.

Under political risk coverage, the exporter files a claim after the specified waiting period. ECGC processes the claim and settles the insured portion of the delayed payment, protecting the exporter from losses caused by external political events beyond the buyer’s control.

Limitations of ECGC Insurance

While ECGC coverage significantly reduces export payment risk, exporters should clearly understand ecgc policy limitations to avoid claim disputes or coverage misunderstandings.

Coverage Conditions

Insurance protection applies only when exporters strictly follow policy terms, including shipment reporting timelines, approved buyer credit limits, and proper documentation maintenance. Transactions made outside approved credit limits or shipments not declared within required reporting periods may not qualify for claim settlement.

Excluded Risks

Certain situations are typically excluded from coverage. Losses arising from disputes related to product quality, contractual disagreements, pricing conflicts, or exporter negligence generally do not fall under insurance protection.

Similarly, non compliance with export regulations or incomplete shipping documentation can lead to claim rejection, even if the buyer fails to pay.

Compliance Requirements

Exporters must continuously comply with policy obligations such as timely premium payment, submission of shipment declarations, prompt reporting of overdue payments, and cooperation in recovery proceedings.

Failure to meet these compliance standards can reduce the insured percentage or delay settlement. Understanding these operational responsibilities is essential for using ECGC insurance effectively as a financial risk management tool.

Conclusion

International trade creates massive growth opportunities, but it also exposes exporters to unpredictable payment risks that can severely disrupt cash flow. This is why ecgc insurance has become an essential protection mechanism within the export credit insurance India ecosystem.

By covering a substantial portion of losses caused by buyer bankruptcy, delayed payments, or political disruptions, ECGC allows exporters to operate confidently across global markets without exposing their businesses to major financial setbacks.

Businesses that extend credit terms to overseas buyers, particularly new exporters, MSMEs, service exporters, and companies entering unfamiliar international markets, should strongly consider obtaining ECGC coverage early in their export journey.

The policy not only protects receivables but also improves access to bank financing, enabling exporters to scale operations faster and handle larger international orders with reduced financial risk. At a broader level, widespread adoption of export credit insurance strengthens the country’s export infrastructure.

When exporters can safely expand into new markets and banks can finance international transactions with lower lending risk, the entire trade ecosystem becomes more competitive. In this context, ECGC insurance is not just a safety measure; it is a strategic instrument that supports sustainable export growth and long term participation in global trade.

Frequently Asked Questions (FAQs)

1. Is ECGC insurance mandatory for exporters in India?

No, ECGC insurance is not legally mandatory for all exporters. However, many banks require ECGC backed coverage before providing export packing credit or post shipment finance, especially for new exporters or high risk international markets.

2. How much loss does ECGC insurance typically cover?

Most Export Credit Guarantee Corporation of India policies cover approximately 80% to 90% of the insured export value, depending on the type of policy, buyer risk profile, and country risk category. The exact percentage is defined in the policy terms.

3. Can small exporters or freelancers apply for ECGC insurance?

Yes. MSME exporters, individual exporters, service exporters, and freelancers involved in international service contracts can apply for suitable Export Credit Guarantee Corporation of India policies designed for smaller export turnovers.

4. How long does ECGC claim settlement take?

Claim settlement timelines depend on document verification and case complexity. After the waiting period and submission of complete claim documentation, settlement is processed according to policy rules, with partial payments often released earlier in certain cases.

5. Does ECGC insurance cover disputes related to product quality?

No. ECGC policies generally do not cover losses arising from quality disputes, contractual disagreements, or exporter negligence. Coverage applies primarily to commercial risks like buyer insolvency and political risks affecting payment transfer.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

Thank you SriHarsha

I am a ECGC Consultant, and this help me alot.

Appreciate that, Bhaskar.

Coming from an ECGC consultant, that actually means a lot. If you have any specific ECGC related insights or real world cases, feel free to share here. Would add a lot of value for readers.