If you are running an export business, a freelance gig, or a SaaS company in India, you know the pain of foreign currency conversions. You receive a payment in USD, the bank instantly converts it to INR , and the money hits your account.

But then, a week later, you need to pay for a software subscription, hosting fees, or an overseas vendor. You have to take that INR, convert it back to USD (at a higher rate), and pay the bill. You lose money on the incoming transaction, and you lose money on the outgoing transaction. It feels like burning cash for no reason.

There is a better way. It’s called the EEFC account.

For many business owners, this account is a mystery. Is it legal? Is it hard to open? Do I really need one? In this guide, we are going to break down everything you need to know about the EEFC account, from the eefc account full form to the complex RBI rules, in simple, plain English.

Foreign money doesn’t lose value when you earn it. It loses value when you’re forced to convert it again and again.

Every time foreign currency hits your Indian bank account, it usually gets converted into INR immediately. Then when you need to pay a supplier abroad, import software, or cover overseas expenses, the bank converts it back to dollars or euros. That double conversion is where money quietly leaks out.

That is the real problem the EEFC account exists to solve. Not paperwork. Not compliance. Cost and control.

Repeated currency conversion means:

- You pay conversion margins twice on the same money.

- You lose flexibility on timing when exchange rates are bad.

- You hand control of your cash flow to the bank instead of managing it yourself.

This is where the EEFC account meaning fits into India’s foreign exchange system. It’s a regulatory exception that allows residents earning foreign currency to hold it as foreign currency, instead of being forced into INR immediately. The system accepts one simple reality, exporters and global service providers don’t operate in rupees alone.

Quick clarity:

It’s an account designed for people who earn in foreign currency and don’t want that money chewed up by unnecessary conversions.

Table of Contents

EEFC Account Full Form and Basic Definition

Let’s strip this down to basics.

The EEFC full form in banking is Exchange Earners’ Foreign Currency account.

Not a savings account. Not a fixed deposit. It’s a non interest bearing current account that holds foreign currency.

An EEFC account means:

If you earn dollars, euros, or pounds, you can keep them as dollars, euros, or pounds inside India for a limited time instead of converting them to INR immediately.

In day to day banking terms, the EEFC account meaning is:

- Money comes in from abroad.

- It stays in foreign currency.

- You decide when and if it should be converted to rupees.

Now, how is this different from a normal current account?

Two clear differences:

- Currency

A normal current account holds INR. An EEFC account holds foreign currency. - Purpose

A normal current account is for domestic transactions. An EEFC account exists specifically to manage foreign exchange earnings efficiently.

If you treat an EEFC account like just another bank account, you’ll misuse it. If you treat it as a foreign exchange management tool, it does exactly what it’s meant to do.

Legal and Regulatory Framework Behind EEFC

If you think the EEFC account is some banking “facility” banks offer out of generosity, that’s wrong. It exists because the law allows it. And the law here is not flexible.

The EEFC account operates under FEMA, 1999. FEMA’s core job is simple regulate how foreign exchange enters, moves within, and exits India. The default FEMA logic is strict conversion. Foreign currency earned in India must normally be converted into INR.

The EEFC account is an exception, not the rule.

Under FEMA, residents earning foreign exchange are permitted to temporarily retain those earnings in foreign currency instead of converting immediately. The purpose is narrow and practical reduce avoidable conversion costs and allow better exchange rate management. Nothing more. Nothing less.

Two important implications follow from this:

- EEFC is a regulated privilege, not a right.

- Every rule around credits, debits, and timelines exists to prevent misuse.

Now, let’s talk about who actually enforces this on the ground.

Role of Authorized Dealer Category-I Banks

You don’t open an EEFC account with just any bank branch. Only Authorized Dealer Category-I (AD Category-I) banks can offer it.

These banks act as the gatekeepers of FEMA compliance. Their role is:

- They verify the source of foreign exchange.

- They monitor usage of funds.

- They ensure balances don’t overstay beyond permitted timelines.

Two realities exporters should understand:

- Banks are personally accountable to regulators for violations. That’s why they ask questions that feel excessive.

- If your bank flags misuse, it’s not being difficult. It’s protecting its license.

Oversight by the Reserve Bank of India

At the top of this structure sits the Reserve Bank of India.

The RBI doesn’t deal with individual EEFC account holders directly. Instead, it:

- Issues master directions and circulars under FEMA.

- Audits and supervises AD Category-I banks.

- Tightens or relaxes rules based on macro forex conditions.

What this really means for you:

If RBI policy shifts, EEFC rules can change overnight. Anyone using an EEFC account casually without following RBI directions can quickly land in regulatory troubles.

Who Can Open an EEFC Account? (Eligibility Explained)

Eligibility is broad, but it’s not universal. This is where many people assume wrongly and get rejected.

Resident Individuals, Businesses, and Professionals

Any resident of India earning foreign exchange can open an EEFC account. That includes:

- Exporters of goods

- Service providers earning fees from overseas clients

- Professionals like consultants, freelancers, and IT service providers billing in foreign currency

The key condition is residency and foreign exchange earnings, not business size or turnover.

Two examples to make this concrete:

- A freelance developer billing a US client in USD qualifies.

- A manufacturing exporter receiving export proceeds qualifies.

No foreign income, no EEFC. It’s that simple.

Joint Account Rules for Resident Individuals

Resident individuals can open joint EEFC accounts, but this is tightly controlled.

The joint holder must be a close relative, and the account must be on a “former or survivor” basis. This is about operational continuity, not shared ownership of foreign exchange earnings.

Translation:

- It’s allowed for practical reasons.

- It’s not meant for pooling or redistribution of foreign currency income.

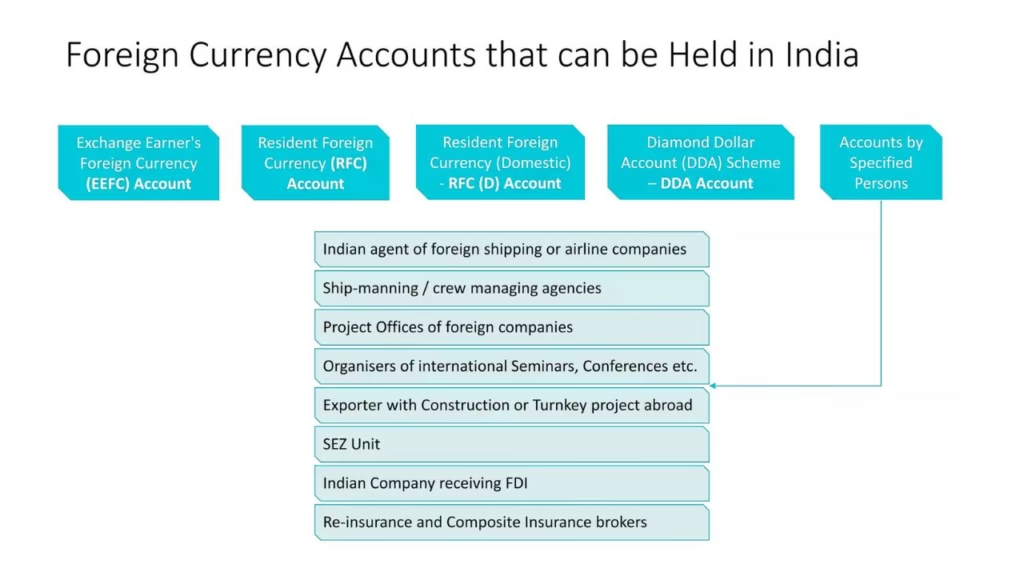

Who Is Excluded and Why SEZ Units Are Treated Differently

Here’s where people get caught off guard.

Units in Special Economic Zones (SEZs) cannot open EEFC accounts.

This is not discrimination. It’s regulatory logic.

SEZ units already operate under a separate foreign currency framework with different privileges and controls. Allowing EEFC accounts on top of that would create overlap and regulatory gaps.

So the rule is clean:

- Non SEZ residents use EEFC accounts.

- SEZ units use foreign currency accounts specifically permitted under SEZ and RBI regulations.

If you’re in an SEZ and try to force an EEFC application through, it will fail. Every time.

Key Features of an EEFC Account

If you’re looking at an EEFC account as a way to earn interest on foreign currency, stop right here. You’re already thinking about it wrong.

Non Interest Bearing Nature and What That Means Practically

An EEFC account does not earn interest. Zero. None. This is intentional. The account exists for currency management, not investment.

What this means in real terms:

- You hold foreign currency for operational use or timing advantage, not for returns.

- Parking money long term in an EEFC account is inefficient.

- The moment you start treating it like savings, you’re misusing it.

Two practical examples:

- Holding USD for a few weeks to pay an overseas supplier makes sense.

- Holding USD for months hoping the dollar appreciates does not.

Currency Holding Rules and Timelines for Conversion to INR

This is the part people mess up most often.

Foreign exchange credited to an EEFC account cannot sit there indefinitely. Any unutilized balance must be converted into INR by the last day of the following calendar month.

Not business month. Not 30 days. Calendar month.

Example one:

- Funds credited on March 10 must be converted by April 30 if unused.

Example two:

- Funds credited on March 31 still face the same April 30 deadline.

Miss this, and you’re no longer talking about convenience. You’re talking about a FEMA violation.

Hedging Options and Forward Contract Flexibility

One underrated feature of the EEFC account is hedging.

Balances in an EEFC account can be hedged against exchange rate risk using forward contracts. Banks also allow these contracts to be rolled over, subject to standard forex rules.

This gives you control:

- Lock in a rate if volatility scares you.

- Delay conversion without gambling on spot rates.

But be clear. Hedging is a risk management tool, not a profit strategy. Anyone treating forwards as speculation usually learns the lesson the expensive way.

EEFC Account Rules You Must Not Ignore

Most problems with EEFC accounts don’t come from what people do intentionally. They come from what people assume is allowed.

Mandatory Conversion Deadline and Consequences of Missing It

Let’s repeat this because it matters. Any balance left unused must be converted into INR by the last day of the next calendar month.

If you miss it:

- The bank may force conversion.

- The transaction can be reported as non compliant.

- Repeated violations invite regulatory inspection.

Banks won’t always remind you. The obligation is yours.

Rules Around Withdrawals and Re Crediting

You can withdraw funds from an EEFC account in INR without restriction. Once withdrawn and converted, that money cannot be reconverted into foreign currency and re credited to the EEFC account.

There is one narrow exception:

- Unutilized foreign currency withdrawals can be re credited if they remain in foreign currency and comply with FEMA rules.

Translation: once you touch INR, that cycle is over.

What You Cannot Do With an EEFC Account (Even If Banks Don’t Warn You)

Here’s where the silent mistakes happen.

You cannot:

- Use EEFC funds for lending in INR.

- Park funds to bypass capital account restrictions.

- Use the account for non FEMA compliant activities.

- Treat it as a workaround to hold foreign currency long term.

Two hard truths:

- Banks won’t always explain these limits clearly.

- Ignorance doesn’t protect you during an audit.

If you respect the rules, an EEFC account is efficient and powerful. If you stretch them, it becomes a liability very fast.

Permissible Credits in an EEFC Account

This is where discipline matters. An EEFC account is not a dumping ground for anything that smells like foreign money. Credits are tightly defined, even if banks don’t spell that out clearly.

Types of Foreign Exchange Earnings Allowed

Only legitimate foreign exchange earnings are allowed to be credited to an EEFC account. The emphasis is on earnings, not receipts.

That includes money that arises directly from:

- Export of goods or services

- Professional or consultancy work for overseas clients

- Trade related foreign inflows permitted under FEMA

If the source doesn’t clearly qualify as foreign exchange earnings, it doesn’t belong here.

Export Proceeds, Professional Fees, and Advance Payments

The most common permissible credits are straightforward:

- Export proceeds received from overseas buyers

- Professional fees earned from foreign clients

- Advance payments received against future exports

Two practical examples:

- A US client pays you $10,000 for software development. That can go into your EEFC account.

- An overseas buyer sends advance payment for goods to be shipped next month. That’s also allowed.

The logic is simple the money is tied to a real cross border transaction.

What Looks Allowed but Actually Isn’t

This is where people get confused.

The following look like foreign currency inflows but are not permitted:

- Foreign currency loans

- Investment proceeds

- Capital injections from abroad not linked to earnings

- Any receipt that violates FEMA or RBI purpose codes

Example one:

- A loan from your overseas parent company cannot be parked in an EEFC account.

Example two:

- Foreign investment money routed through banking channels is not EEFC eligible.

If the inflow creates a future obligation or represents capital, not income, it doesn’t qualify.

Permissible Debits From an EEFC Account

Debits are broader than credits, but they’re not unlimited. The rule of thumb is utility and compliance.

Import Payments and Overseas Obligations

EEFC balances can be freely used for permissible current and capital account transactions, including:

- Import payments for goods and services

- Payments to overseas vendors or contractors

- Trade related obligations abroad

Two clean use cases:

- Paying a foreign supplier without converting to INR first.

- Settling overseas hosting or SaaS bills directly in USD.

This is where EEFC accounts deliver real efficiency.

Payments for Services Within India Using Foreign Currency

Yes, you can use EEFC funds to pay for certain services within India, provided the transaction itself is permitted to be settled in foreign currency.

Common examples include:

- International airfare booked through Indian agents

- Services where FEMA explicitly allows foreign currency settlement

This area is compliance-sensitive. The service must qualify. The currency alone doesn’t make it valid.

Transactions That Trigger Compliance Red Flags

Some debits don’t break rules outright but still attract attention.

Red flags include:

- Frequent transfers unrelated to core business activity

- Using EEFC funds to route money between group entities

- Patterns that resemble lending, parking, or layering

Two warnings:

- Banks monitor EEFC usage more closely than normal accounts.

- Even technically permissible transactions can be questioned if the intent looks off.

If your EEFC debits don’t clearly tie back to foreign exchange earnings or overseas obligations, expect an inspection. That’s not speculation. That’s how the system is designed.

Prohibited Uses and Common Compliance Mistakes

This is where EEFC accounts quietly turn from helpful to dangerous. Not because people intend to break rules, but because they assume silence means permission.

It doesn’t.

Lending and Non FEMA Compliant Activities

An EEFC account is not a workaround for holding or circulating foreign currency inside India.

You cannot:

- Lend EEFC funds in INR to anyone.

- Use the account to route money between related parties.

- Park funds to bypass capital account restrictions.

- Use it for transactions not explicitly permitted under FEMA.

Two examples exporters routinely get wrong:

- Using EEFC money to give short term advances to Indian vendors.

- Transferring EEFC balances to group companies for internal liquidity.

Both look operational. Both are violations.

Misuse That Leads to Account Freezing or Penalties

Banks don’t jump straight to penalties. They escalate.

Misuse typically triggers:

- Enhanced monitoring and queries.

- Forced conversion of balances into INR.

- Temporary debit restrictions.

- Reporting to regulators in serious or repeated cases.

Two real world patterns that cause trouble:

- Letting balances sit past the conversion deadline repeatedly.

- Using EEFC funds for transactions unrelated to foreign earnings.

Once your account is flagged, every transaction gets slower, costlier, and more painful. Clearing your name takes far longer than opening the account.

Where Most Exporters Mess This Up

Most exporters fail in three predictable ways:

- They treat the EEFC account like a savings account.

- They assume banks will warn them before violations.

- They don’t track RBI and FEMA rule updates.

The harsh truth:

Compliance responsibility sits with you, not the bank. The bank just reports.

Benefits of an EEFC Account for Exporters and Professionals

Used correctly, an EEFC account is boring. And that’s a compliment. It quietly does its job.

Reduction in Conversion Losses

This is the primary benefit, not a side effect.

By avoiding unnecessary INR conversions:

- You save on bank spreads.

- You avoid double conversion costs.

- You stop bleeding margin on every cross border cycle.

Two clear wins:

- Receiving USD and paying USD without touching INR.

- Timing conversion when rates are favorable instead of automatic.

Exchange Rate Risk Management

An EEFC account gives you choice, not guarantees.

You can:

- Hold currency briefly during volatile periods.

- Hedge balances using forward contracts.

- Avoid panic conversions during rate swings.

What it doesn’t do:

- Eliminate risk.

- Predict currency movements.

- Magically improve margins.

Risk management is about reducing exposure, not beating the market.

Cash Flow Control and Timing Advantages

This is the benefit experienced operators value most.

EEFC accounts allow you to:

- Match inflows with outflows in the same currency.

- Plan conversions based on business needs, not bank automation.

- Improve working capital predictability.

Two practical advantages:

- Paying overseas expenses instantly without conversion delays.

- Converting only what you need, when you need it.

Bottom line:

An EEFC account doesn’t make you more money. It stops unnecessary loss. If that distinction isn’t clear, you’re not ready to use one properly.

Currencies Supported Under EEFC Accounts

Let’s clear a common misunderstanding first. An EEFC account is not a free for all foreign wallet. Currency support depends on what Indian banks actually clear and settle efficiently.

Commonly Supported Currencies Like USD, EUR, GBP

Most banks support major, liquid currencies. In practice, that usually means:

- USD

- EUR

- GBP

Some banks also allow a few others like JPY or AUD, but availability varies and liquidity drops fast outside the big three.

Two realities to keep in mind:

- Just because a currency exists doesn’t mean your bank wants to hold it.

- Exotic currencies increase compliance checks, spreads, and delays.

If most of your invoices are in USD, keep it simple. Complexity here adds cost, not flexibility.

Why Multi Currency Access Matters in Real Operations

Multi currency access isn’t about convenience. It’s about alignment.

Two concrete examples:

- You earn in USD and pay a US supplier in USD. No conversion. No spread. No timing risk.

- You earn in EUR but converted to INR immediately, then reconvert to EUR a week later. That’s pure loss.

Where multi currency access actually helps:

- Matching inflows and outflows without touching INR.

- Reducing dependency on daily exchange rates.

- Simplifying cross border settlements.

Where it doesn’t help:

- If all your expenses are domestic.

- If you convert everything immediately anyway.

Holding multiple currencies only makes sense if your operations demand it. Otherwise, you’re just adding friction.

EEFC Account vs Normal Current Account

This comparison is where decision making gets real. Ignore the theory. Focus on money movement.

Functional Differences That Actually Impact Money

Here’s the difference that matters.

A normal current account:

- Holds INR only.

- Forces conversion the moment foreign money arrives.

- Works well for domestic operations.

An EEFC account:

- Holds foreign currency.

- Lets you delay conversion.

- Exists to manage forex exposure, not day to day Indian payments.

Two direct financial impacts:

- EEFC reduces conversion losses.

- Current accounts offer zero protection against exchange rate timing.

Everything else is secondary.

When an EEFC Account Makes Sense and When It Doesn’t

An EEFC account makes sense if:

- You regularly earn foreign exchange.

- You have foreign currency expenses.

- Conversion timing affects your margins.

It does not make sense if:

- Your foreign income is occasional.

- You convert immediately anyway.

- You want interest or long term holding.

Hard truth:

If you open an EEFC account just because someone said exporters should have one, you’re wasting effort. If you open it because you understand your currency cycle, it quietly pays for itself.

How to Open an EEFC Account

Opening an EEFC account isn’t complicated, but it is compliance heavy. If you expect speed without paperwork, you’re not being realistic.

Step by Step Overview of the Opening Process

The process mirrors a current account, with extra forex examination.

Step one: Choose an AD Category-I bank

Not every branch handles EEFC accounts well. Pick one that actually deals with exporters and foreign remittances daily.

Step two: Submit the EEFC application form

This is usually bundled with the bank’s current account or foreign exchange forms. Confusion slow everything down.

Step three: Provide KYC and business documents

Individual or entity documents depend on your structure. Banks won’t proceed without full KYC.

Step four: Foreign exchange profile verification

Banks check how you earn foreign currency, from whom, and how frequently.

Step five: Account activation after compliance clearance

Once the compliance team signs off, the EEFC account goes live.

There’s no shortcut. Anyone promising instant activation is lying.

Typical Compliance Checks by Banks

This is where most delays come from, and also where most rejections happen.

Banks typically check:

- Source and nature of foreign exchange earnings

- FEMA eligibility based on residency and activity

- Business model consistency with expected inflows

- Past forex transaction history, if any

Two things banks hate:

- Vague explanations of foreign income

- Mismatch between documents and actual operations

If your story changes between forms and conversations, expect questions.

Timeline Expectations

Best case scenario: 7–10 working days

Average reality: 2–3 weeks

If compliance flags anything:

- Timelines stretch.

- Queries pile up.

- Activation pauses until clarification.

Plan for delays. If your business depends on immediate foreign currency handling, open the account before you need it.

Documents Required for Opening an EEFC Account

Documents aren’t about volume. They’re about credibility.

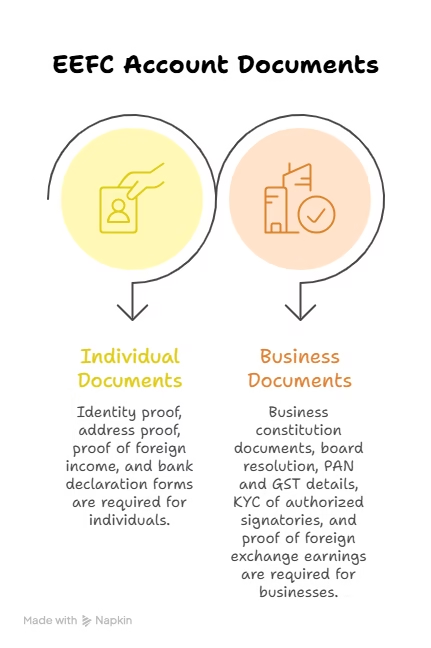

Individual vs Business Documentation

For individuals:

- Identity proof (PAN, passport)

- Address proof

- Proof of foreign income or contracts

- Bank specific EEFC declaration forms

For businesses:

- Business constitution documents (partnership deed, incorporation certificate, LLP agreement)

- Board resolution or authorization letter

- PAN and GST details

- KYC of authorized signatories

- Proof of foreign exchange earnings or export activity

The structure determines the checklist. Don’t mix individual logic with business paperwork.

Proofs Banks Scrutinize the Most

Banks focus hardest on:

- PAN and KYC consistency

- Nature of foreign income

- Contracts, invoices, or export documentation

- Purpose codes linked to expected inflows

Two weak points that cause trouble:

- Generic contracts with no clear service description

- Invoices that don’t align with the declared business activity

If your income source looks unclear, compliance slows to a crawl.

Common Reasons Applications Get Delayed

Most delays are self created.

Top reasons:

- Incomplete or mismatched documents

- Unclear explanation of foreign earnings

- SEZ status confusion

- Frequent back and forth due to vague responses

Hard truth:

Banks don’t delay EEFC accounts for fun. They delay them because bad approvals cost them far more than losing your business.

Banks Offering EEFC Accounts in India

Not all banks are equal when it comes to EEFC accounts. On paper, many offer it. In reality, only a few handle it smoothly.

Availability at Major Private Banks

Most exporters and professionals end up with large private sector banks because they already run strong forex desks.

Common choices include:

- HDFC Bank

- ICICI Bank

- IndusInd Bank

Public sector banks also offer EEFC accounts, but execution varies heavily by branch. Some are excellent. Many are slow. Consistency is the issue.

Two realities you should accept upfront:

- EEFC accounts are relationship driven products.

- Your experience depends more on the branch and forex team than the brand name.

Practical Considerations When Choosing a Bank

Don’t choose a bank based on brochures. Choose it based on how it behaves after the account is opened.

What actually matters:

- Forex desk competence: Can they handle conversions, hedging, and documentation without confusion?

- Compliance responsiveness: Do they resolve queries quickly or let emails rot?

- Digital access: Can you track balances and transactions clearly, or is everything manual?

Two mistakes people make:

- Choosing the bank with the lowest headline charges but terrible execution.

- Opening EEFC accounts across multiple banks without operational need.

Pick one solid bank, build a relationship, and keep it boring. Boring is good in compliance heavy banking.

Final Take Who Should Actually Use an EEFC Account

Let’s end the confusion and kill the hype. An EEFC account is not a badge of being an exporter. It’s a tool. Use it only if the math and operations justify it.

A Clear Decision Framework

Ask yourself three questions. Answer them honestly.

- Do you earn foreign currency regularly?

Not once in a while. Not a lucky client last quarter. Regularly. - Do you also spend in foreign currency?

Suppliers abroad, SaaS tools, hosting, consultants, travel, imports. - Does conversion timing affect your margins or cash flow?

If rates move against you, do you actually feel it?

If the answer is yes to at least two, an EEFC account makes sense.

If the answer is mostly no, stop forcing it.

Who Benefits the Most

EEFC accounts work best for people with clean, repeatable forex cycles.

Two clear winners:

- Exporters who receive in USD or EUR and pay suppliers in the same currency.

- Professionals and agencies billing overseas clients while running foreign expenses.

Why they benefit:

- Fewer conversions.

- Lower bank spreads.

- Better control over when money turns into INR.

For them, EEFC is not optional optimization. It’s basic hygieneSM (simple money management).

Who Should Skip It Despite Eligibility

Eligibility doesn’t equal usefulness. This is where ego gets in the way.

You should skip an EEFC account if:

- Foreign income is occasional or unpredictable.

- You convert everything to INR immediately anyway.

- All expenses are domestic.

- You don’t track compliance deadlines closely.

Two examples of bad fits:

- A freelancer with one foreign client a year.

- A business that earns in USD but spends entirely in INR.

In these cases, EEFC adds paperwork, monitoring, and risk without real savings.

Bottom Line

An EEFC account won’t grow your business.

It won’t increase revenue.

It won’t make you smarter.

What it will do, if used correctly, is stop unnecessary loss.

If you don’t have a clear forex problem, don’t adopt a forex solution. That’s not conservative. That’s disciplined.

Frequently Asked Questions (FAQs)

Q1. Is an EEFC account safe, or can funds get stuck?

It’s safe if you follow the rules. Funds get stuck only when users miss conversion deadlines or misuse the account. Two common traps: letting balances sit past the permitted period, and using EEFC money for non-forex activities. The account doesn’t freeze itself. Bad compliance does.

Q2. Can freelancers and consultants open an EEFC account, or is it only for exporters?

Freelancers and consultants absolutely can open one if they earn foreign exchange regularly. A US client paying monthly qualifies. A one-off overseas project doesn’t justify it. Eligibility is broad. Practical usefulness is not.

Q3. Can I keep converting small amounts from EEFC to INR whenever I want?

Yes, partial conversions are allowed. But don’t abuse this. Converting daily without purpose defeats the whole point and increases scrutiny. Two smart uses: converting only what you need for INR expenses, or converting when rates move in your favor.

Q4. What happens if I accidentally miss the EEFC conversion deadline?

Best case: the bank forces conversion to INR. Worst case: the transaction is reported as non-compliant under FEMA. Miss it once, you’ll get warned. Miss it repeatedly, and the account becomes a liability instead of a tool.

Q5. Should every exporter open an EEFC account by default?

No. That’s lazy advice. Exporters with frequent foreign inflows and outflows benefit. Everyone else just adds compliance work for no gain. If you don’t clearly save money or manage risk better with EEFC, skip it.

About the Author

Hi, I’m Sriharsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

3 thoughts on “EEFC Account Explained: 7 Critical Rules, Benefits, and Mistakes Exporters Must Know”