Shocking but true hidden fees in international TT payments can consume up to 9% of every transaction you make across borders. In 2022 alone, over $150 trillion flowed through the global financial system, with businesses unknowingly losing significant portions to hidden charges.

When we examine telegraphic transfer (TT) payment terms closely, the reality becomes even more concerning. Banks typically add 3-6% to exchange rates for international payments, while African businesses dealing with volatile currency pairs can face surcharges reaching 8-10%.

Additionally, you’ll encounter various fees including currency conversion charges (1-3% of transaction value), intermediary bank costs ($10-30 per bank), and receiving bank fees. Consequently, on just $100,000 in annual international payments, your business could be losing $8,000-$10,000 to exchange rate markups alone.

In this guide, we’ll unpack what TT payment means for exporters, reveal the seven most common hidden charges, and provide practical strategies to significantly reduce your international payment costs.

Whether you’re new to TT payment terms in export or looking to optimize your existing processes, this article will help you keep more of your hard earned money.

Table of Contents

What is TT Payment and Why It Matters for Exporters

TT payments remain the backbone of international trade finance despite their historical name. The TT payment full form “Telegraphic Transfer” traces back to an era when banks used telegraph systems to communicate cross border payments a practice now replaced by smart digital networks.

TT payment meaning

Telegraphic Transfer (TT) is an electronic method of transferring funds between banks, primarily used for international transactions. Despite its name suggesting outdated technology, modern TT payments operate through secure electronic networks.

In some regions like the UK, Australia, and New Zealand, the term “telegraphic transfer” is commonly used, whereas Americans typically refer to the same process as “wire transfers”.

Essentially, when exporters mention TT payment terms, they’re referring to international bank to bank transfers that typically process within 1-5 business days. The term has evolved from its historical origins when actual telegraphs transmitted payment instructions to become identical with SWIFT transfers in today’s digital banking landscape.

How TT payments work in international trade

When processing a TT payment, exporters initiate an electronic funds transfer through their bank. The transaction then travels through the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network, which connects financial institutions globally.

To complete a TT transfer, several pieces of information are required:

- Recipient’s full name and account number

- Recipient’s bank name, address, and branch

- SWIFT/BIC code for international identification

- Transfer amount and currency

- Purpose of payment (particularly for large transfers)

The funds don’t physically move between banks. Instead, payment instructions travel electronically, typically passing through 1-3 intermediary banks before reaching the final destination.

This multi bank process explains why TT payments take 1-5 business days to clear and often incur various charges at different stages of the transfer.

Why exporters rely on TT payments

For exporters navigating international markets, TT payments offer several distinct advantages that make them necessary:

First, TT transfers provide exceptional security and regulatory compliance. Each transfer generates a complete audit path with unique reference numbers and confirmation documentation essential for meeting cross border regulatory requirements.

This traceability proves particularly valuable during customs checks or tax audits.

Moreover, TT payments are universally accepted across global markets. This widespread adoption makes them practical for businesses dealing with international clients regardless of location.

For high value transactions or custom orders where supplier risk exists, TT payments allow exporters to request advance payment before manufacturing or shipping.

Primarily, TT payments create valuable financial records beyond simple transactions. Exporters can leverage these documented payment histories to build creditworthiness with partners, strengthen loan applications, or demonstrate stable cash flow to potential investors.

Finally, TT offers flexibility in payment timing, exporters can request payment before shipping (TT in advance), upon receipt of goods (TT in sight), or after a specified period (TT at X days). This adaptability allows businesses to adjust terms based on relationship trust and transaction risk.

Unlike other payment methods, TT transfers put exporters in control of risk when using advance payment terms, funds arrive before shipment, ensuring goods only leave after payment confirmation.

The Real Cost of TT Payments: 7 Hidden Charges Explained

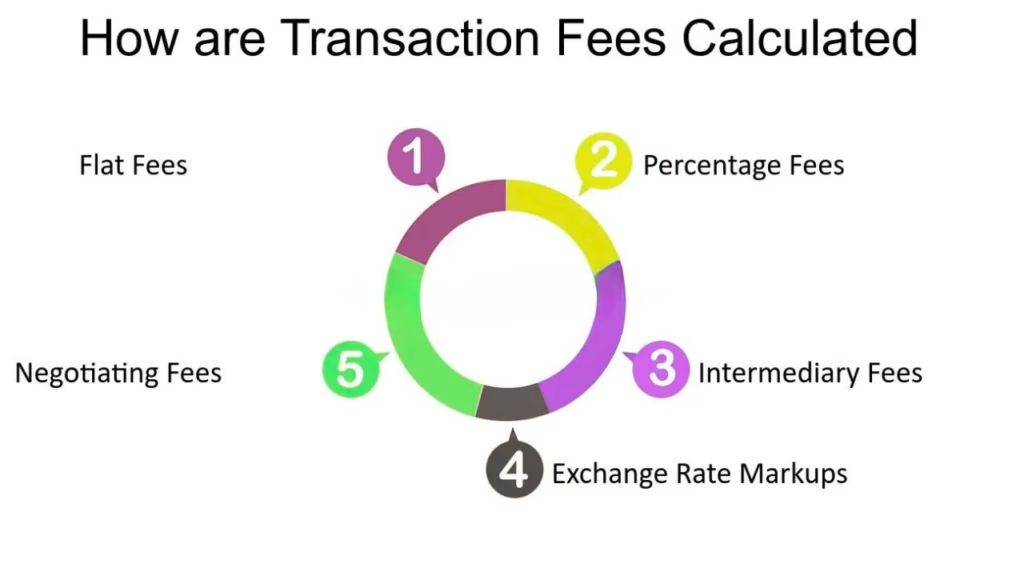

Behind every TT payment lies a complex web of charges that most exporters never see until it’s too late. These hidden costs can significantly reduce the actual amount received by your international partners.

1. Exchange rate markup

Banks rarely offer the true mid market exchange rate for TT payments. In fact, they typically add markups ranging from 1-5% above the mid market rate, with high street banks charging up to 3.5%. This markup is often disguised in what banks call an “all in exchange rate”.

For example, a bank may advertise a seemingly low transfer fee, yet simultaneously apply a 2% margin to your currency conversion. On a $1.27 million transaction, this hidden markup alone could cost you up to $32,000 as expense most businesses never specifically see on their statements.

2. Intermediary bank fees

When your TT payment travels across borders, it typically passes through multiple intermediary banks that facilitate the transfer. Each of these institutions deducts their own fee generally between $15-$50 per transaction.

Surprisingly, as many as five intermediary banks might be involved in a single transfer, creating a chain of deductions from your original amount. Since these fees are deducted as your payment moves through the SWIFT network, your recipient often receives less than you intended to send.

3. Receiving bank charges

Once your payment reaches its destination, the recipient’s bank frequently puts additional charges for processing incoming international funds.

Major US banks like Bank of America, Wells Fargo, and Chase typically charge receiving customers $15 per incoming international transfer.

Importantly, most sending banks have no control over these receiving charges. These fees are particularly problematic for recurring payments or when working with suppliers who expect to receive precise amounts.

4. Currency conversion fees

Besides the exchange rate markup, separate currency conversion fees may apply to your TT payment. These fees are especially significant when dealing with less common currency pairs or countries with less connected banking systems.

Furthermore, currency conversion can add one or more days to your payment processing timeline. This extended processing time not only delays your transaction but also exposes you to potential exchange rate fluctuations during the conversion period.

5. Weekend and holiday rate risks

TT payments initiated near weekends or holidays face unique challenges. Many banks adjust their rates outside normal market hours, adding extra buffers to protect against rate fluctuations.

Additionally, if your payment involves multiple countries, their different weekend schedules and holiday calendars can cause unexpected delays. For instance, weekend definitions vary globally while Western countries typically observe Saturday Sunday weekends, some Middle Eastern countries operate Saturday Thursday.

6. Compliance and regulatory fees

International payments must navigate complex compliance requirements designed to prevent financial crimes. Banks must verify that neither the sender nor recipient appears on government sanctions lists.

These verification processes add both time and cost to TT payments. Financial institutions maintain smart monitoring systems to detect suspicious activity patterns, with the associated compliance costs often passed on to customers through fees that aren’t specifically disclosed.

7. Payment failure and amendment charges

If any payment details are incorrect, your TT payment may be rejected or require manual intervention to complete. Correcting these errors comes at a significant cost amendments typically accept charges of $30 per transaction plus agent bank fees, while cancelations can cost $35 plus additional charges.

If funds need to be returned due to payment failure, you face potential exchange rate losses on the round trip. The original and return transactions might occur at different rates, further reducing the amount you recover.

Worked Example: How Much You Actually Pay on TT Transfer

Let’s analyze the raw numbers of a $5,000 international TT transfer to reveal what truly happens to your money. The advertised fees often tell only a fraction of the story.

Advertised vs actual cost breakdown

Initially, most exporters focus on the base wire fee typically $25-50 for international transfers. For a $5,000 TT payment, a bank might advertise just a $30 sending fee. Yet this represents merely the visible tip of a much larger expense iceberg.

The actual cost structure looks dramatically different:

- Base sending fee: $25-35

- Exchange rate markup (typically 2-3%): $100-150

- Intermediary bank fees (1-3 banks): $15-90

- Receiving bank charges: $15

- Possible weekend/holiday processing premium: $10-20

In reality, what appears as a simple $30 fee balloons into $165-$310 in total charges representing 3.3-6.2% of your transfer amount.

How hidden fees reduce the amount received

Consider this practical calculation: When sending $5,000 abroad, a 3% exchange rate markup immediately reduces the converted amount by $150. Subsequently, if two intermediary banks each deduct $20, and the recipient’s bank charges another $15, the final amount received drops by $205.

This explains why your overseas supplier who expected $5,000 might actually receive only $4,795 creating potential confusion and strained business relationships.

A side by side comparison with alternative providers highlights the difference. According to documented cases, sending $5,000 through a traditional bank might cost $270 in total fees, whereas specialized providers charge substantially less often saving exporters $100 or more per transaction.

Lessons from real exporter scenarios

One business owner described the revelation after discovering she had been paying CAD(cash against documents) $45 for every transfer “I couldn’t believe I was paying CAD $45 for every transfer. That’s when I looked for other options to find a secure way to make payments”.

Notably, many businesses only discover these hidden costs through painful experience. A European company sending €50,000 to Germany was shocked to find €237 in unexpected fees, coupled with a two day delay that strained a crucial business relationship.

Ultimately, the most successful exporters recognize that TT payment costs compound with transaction volume. What seems manageable on a single $5,000 transfer becomes significant when multiplied across dozens of monthly payments.

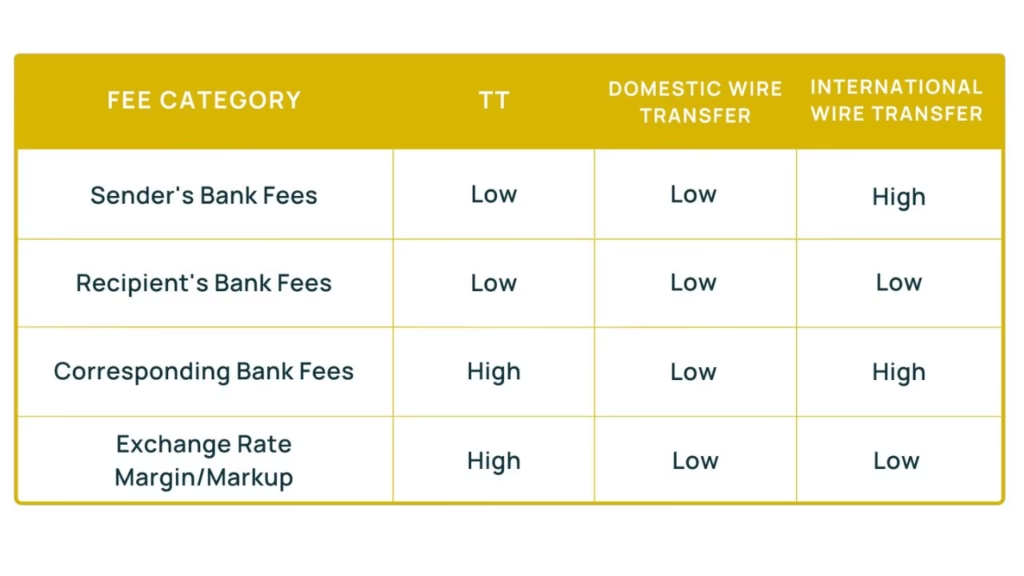

Comparing TT Payment Methods: Banks vs Fintech Platforms

When it comes to transferring money internationally, exporters now have three different TT payment options, each with unique cost structures and benefits.

Traditional bank TT transfers

Banks remain the most widely used TT payment method, Although not the most cost effective. The legacy system typically involves fees ranging from 3-6% of each transaction alongside lengthy settlement periods of 2-5 days.

Traditional international payments operate through the SWIFT network, requiring your payment to pass through multiple intermediaries each adding their own fees and potential delays. However, banks offer exceptional security and regulatory compliance, making them suitable for high value, low frequency transactions where reliability overcomes cost.

Digital platforms (PayPal, Stripe)

Digital payment platforms provide alternatives to traditional bank transfers for international payments. PayPal charges transaction fees with a 49 cent flat fee plus variable percentage amounts.

Comparatively, Stripe charges 2.9% plus $0.30 for online sales. Both platforms support multiple currencies, though Stripe accommodates over 135 currencies while PayPal supports just 25.

The key advantage of digital platforms is their user friendly interface. However, they often impose payment size limits and may not be ideal for large B2B transactions. PayPal has higher brand recognition and allows payments using PayPal or Venmo balances, whereas Stripe offers greater customization options.

Modern fintech solutions (Wise, Skydo, Karbon)

Fintech platforms specifically designed for cross border payments have disrupted the market by slashing costs and accelerating transfers. These solutions enable settlements in minutes rather than days, with total fees typically ranging between 0.5–1.5%.

Wise (formerly TransferWise) charges a conversion fee of 1.7-1.9% of the transaction amount.

Skydo offers a transparent flat fee structure: $19 for payments up to $2,000, $29 for payments between $2,001-$10,000, and 0.3% for larger amounts.

Both convert funds at live forex rates with minimal or no markup, though Skydo provides free instant FIRA documentation while Wise charges approximately $2.50 per FIRA.

Which method is best for your business?

The optimal choice depends on your specific needs:

- Traditional banks work best for businesses requiring maximum security for occasional high value transfers.

- Digital platforms suit companies making frequent smaller payments that prioritize convenience over cost.

- Fintech solutions benefit exporters making regular international transfers who need to minimize fees without sacrificing speed or reliability.

As a result, many exporters now maintain relationships with multiple payment providers, using each strategically based on transaction type, destination, and urgency.

How to Reduce TT Payment Fees as a Smart Exporter

Savvy exporters can slash their TT payment costs with these five proven strategies.

Use mid market rate platforms

Primarily focus on platforms offering the mid market exchange rate the same rate banks use when trading with each other. Wise consistently provides this “real” rate without padding, potentially saving you 3-5% on currency conversion versus traditional banks.

These platforms typically charge transparent fees rather than hiding profits in exchange rate markups, making your actual costs immediately visible.

Ask clients to choose OUR in SWIFT

When initiating TT payments, request the OUR charge code option meaning the sender pays all transfer fees. This ensures your overseas partners receive the exact amount invoiced without unexpected deductions from intermediary banks.

Although this slightly increases your upfront cost, it eliminates payment disputes altogether.

Time your payments strategically

Certainly avoid initiating transfers right before weekends or holidays, which often lead to unfavorable exchange rates plus extended processing times. Currency markets typically offer better rates mid week during overlapping trading hours between major financial centers.

Automate recurring payments

Batch multiple small payments into fewer larger ones to minimize fixed transaction fees. Some providers offer scheduled recurring transfers at locked in exchange rates for up to two years, protecting against market volatility.

Automated payments ultimately save both time and money compared to manual processing.

Verify all fees before invoicing

Compare your provider’s rates against the mid market rate found on Google. This simple check reveals hidden markups that often exceed advertised fees. Many banks offer fee waivers or better rates for businesses with high transaction volumes hence never hesitate to negotiate better terms.

Conclusion

TT payments remain essential for international trade, though hidden costs can significantly impact your bottom line. Throughout this guide, we’ve uncovered how seemingly small fees compound into substantial expenses, potentially consuming 3-6% of each transaction value.

The difference between advertised and actual costs proves particularly startling. Your $5,000 transfer might appear to cost merely $30 in base fees while actually incurring $165-$310 in total charges.

Consequently, these hidden expenses directly reduce profit margins and create confusion with international partners expecting precise payment amounts.

Banks certainly offer security advantages, but alternative platforms like Wise and Skydo now provide comparable reliability at a fraction of the cost. Smart exporters therefore utilize multiple payment methods strategically based on specific transaction needs rather than defaulting to traditional banking channels.

Prepared with the strategies outlined above, you can slash unnecessary fees immediately. Choosing mid market rate platforms, requesting OUR charge codes, timing payments strategically, automating recurring transfers, and verifying all fees before invoicing will help preserve your hard earned revenue.

Undoubtedly, the most successful exporters treat payment processing as a crucial business function worthy of optimization rather than an unavoidable administrative cost. This mindset shift alone can save thousands annually for businesses conducting regular international transactions.

Take action today by comparing your current provider’s rates against mid market alternatives. This simple step will reveal exactly how much your business loses to hidden fees annually.

After all, money saved on unnecessary transfer costs directly translates to improved competitiveness and increased profits in the global marketplace.

FAQs

Q1. What exactly is a TT payment in international trade?

A TT payment, or Telegraphic Transfer, is an electronic method of transferring funds between banks, primarily used for international transactions. Despite its historical name, modern TT payments operate through secure digital networks and are widely used in global trade.

Q2. How do TT payment fees typically work?

TT payment fees can include various charges such as base sending fees, exchange rate markups, intermediary bank fees, and receiving bank charges. These fees can collectively amount to 3-6% of the transaction value, often hidden within the exchange rate or spread across multiple deductions.

Q3. What are the main differences between TT payments and Letters of Credit (LC)?

TT payments are generally faster and simpler, relying on direct bank-to-bank transfers. They offer less security but greater speed compared to Letters of Credit. LCs provide more protection through bank guarantees but involve more documentation and processing time.

Q4. How long does a TT payment usually take to process?

TT payments typically process within 1-5 business days. The exact duration can vary depending on factors such as the banks involved, currency pairs, and any intermediary banks the payment passes through.

Q5. What strategies can exporters use to reduce TT payment fees?

Exporters can reduce TT payment fees by using platforms offering mid-market exchange rates, requesting the OUR charge code option, timing payments strategically to avoid weekends and holidays, automating recurring payments, and thoroughly verifying all fees before invoicing.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

4 thoughts on “TT Payment Charges Explained: A Real Cost Guide for Smart Exporters”