You can ship goods perfectly and still not get paid if FEMA rules are violated. That’s the part most beginners miss. They focus on product, pricing, and buyers. The real gatekeeper is the bank, and the bank only releases your money if the transaction follows the FEMA Act (Foreign Exchange Management Act, 1999).

Here’s where FEMA shows up in real life:

- Export payments stuck at the bank

Your buyer sends money, but your bank holds it because your shipping bill doesn’t match your invoice or your AD code is missing. - Foreign remittances delayed or rejected

A client pays you from abroad, but the payment is flagged because the purpose code or documentation doesn’t align with FEMA rules.

This is why understanding the FEMA Act, and the foreign exchange management act 1999 is vey crucial if you deal with international money.

What this guide will do is simple:

- Explain the fema meaning in export in practical terms

- Show how FEMA actually controls your payments

- Help you avoid the exact mistakes that cause payment delays and compliance issues

Table of Contents

What Is Foreign Exchange Management Act ?

The FEMA full form is Foreign Exchange Management Act.

In plain language, FEMA is the law that controls all foreign currency transactions in India. If money is coming into or going out of India in any foreign currency, it is governed by the FEMA Act.

What this really controls:

- Imports and exports

Every payment you send or receive for international trade - Foreign payments and remittances

Freelancing income, overseas transfers, foreign service payments - Forex conversions

How USD, EUR, GBP etc. get converted into INR through banks

In banking terms, the fema meaning in banking is No foreign transaction gets processed unless it complies with FEMA rules.

Let’s break this down with real scenarios.

Example 1: Exporter receiving USD from a USA buyer

You ship goods to a buyer in the US. The buyer sends 5,000 USD. The bank does not just credit your account. It first checks your export documents under FEMA rules in India. Only after verification does the bank convert USD to INR and release the payment.

Example 2: Freelancer receiving payment through PayPal or Stripe

You design a website for a foreign client and get paid in USD. Even this payment goes through FEMA compliance checks in the background before the money reaches your Indian bank account.

That’s the real answer to what is FEMA Act in practice:

It’s the system that decides whether your foreign money gets credited smoothly or gets stuck in compliance.

FEMA Act 1999 – Background and Why It Replaced FERA

The Foreign Exchange Management Act 1999 didn’t appear randomly. It was a direct response to how outdated and restrictive the earlier system had become.

Timeline that matters:

- FERA (Foreign Exchange Regulation Act) was introduced in 1973

- India opened its economy in the early 1990s

- FEMA Act 1999 was enacted on December 29, 1999

- It came into force on June 1, 2000

It was a complete change in mindset.

Why FERA failed

FERA was built for a time when India had a foreign exchange shortage. So it treated foreign currency like something to be tightly controlled.

The problem? It was too strict for a modern economy.

- Violations were criminal offences

- You were assumed guilty unless you proved innocence

- Almost every forex transaction needed permission

Two real world problems under FERA:

- An exporter receiving delayed payment could face legal trouble even if the delay was not his fault

- Businesses needed multiple approvals for simple international transactions, slowing down trade

That approach choked growth.

Why FEMA was introduced

Foreign Exchange Management Act flipped the approach from control to management.

It was designed to:

- Support liberalization policies

- Align with WTO and global trade norms

- Make cross border business easier

Under Foreign Exchange Management Act:

- Offences became civil, not criminal

- Transactions are allowed unless specifically restricted

- The system became trade friendly

Two real world improvements after Foreign Exchange Management Act:

- Exporters can now receive payments with simpler compliance instead of criminal scrutiny

- Businesses can invest abroad or receive foreign investment under structured, clear rules

This is the main difference between FERA and FEMA.

FERA restricted. FEMA facilitates.

The answer for fera vs fema india is FEMA is built for business, FERA was built for control.

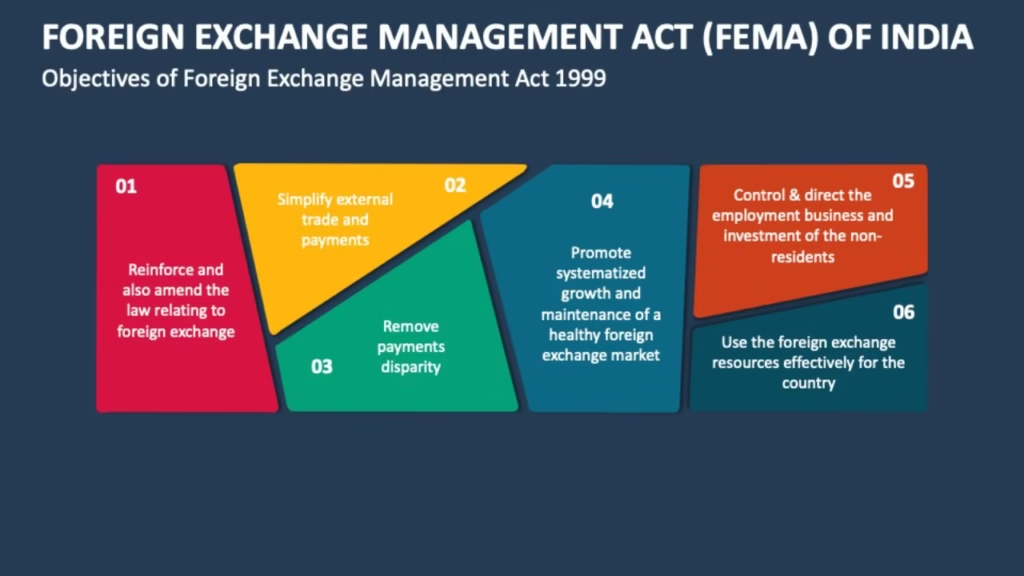

Objectives of FEMA (What the Law Is Trying to Achieve)

The objectives of Foreign Exchange Management Act are not abstract policy goals. They directly affect how money flows into your business.

Let’s break them into four clear outcomes.

1. Facilitate external trade and payments

FEMA makes sure importers and exporters can send and receive payments without unnecessary barriers.

Example:

An exporter ships goods to Europe and receives payment in EUR. Foreign Exchange Management Act ensures the bank can process that payment smoothly as long as documents are correct.

2. Promote development of the forex market

India needs a stable and active foreign exchange market. FEMA allows authorized banks and financial institutions to deal in foreign currency under RBI regulation.

Example:

Banks provide forex conversion, hedging, and forward contracts to protect exporters from currency fluctuation.

3. Regulate foreign investments

FEMA controls how foreign money enters India and how Indian money goes abroad. This includes FDI, external commercial borrowings, and overseas investments.

Example:

A foreign investor investing in an Indian startup is allowed under Foreign Exchange Management Act guidelines with defined limits and reporting requirements.

4. Ensure legal flow of foreign currency into India

The core purpose of FEMA is to make sure every foreign currency transaction is:

- genuine

- documented

- traceable

This prevents illegal activities like money laundering or fake export billing.

Example:

When RBI allows easier export payment realization timelines, it helps genuine exporters while still tracking every foreign inflow.

Put simply, the purpose of Foreign Exchange Management Act is to balance two things at once:

- make international business easy

- keep foreign exchange flows legal and transparent

That’s what fema regulations india are designed to do.

If you’re earning from outside India, investing abroad, or running an export business, these objectives are not theory. They directly control how and when your money moves.

Key Provisions of FEMA You Must Understand

Most people say they “know FEMA” but can’t explain the actual rules that control their payments. These are the core FEMA sections explained in plain terms. If you understand these, you won’t get stuck at the bank.

Section 3 :Unauthorized Forex Transactions Prohibited

This is the backbone of FEMA Section 3.

You cannot deal in foreign exchange unless:

- it is done through an authorized dealer (bank)

- and it follows RBI rules

What this really means in practice:

- You cannot accept foreign payment directly into a personal wallet without routing through the banking system

- You cannot send foreign currency to someone abroad without proper documentation

Example 1:

An exporter receives USD directly into a foreign wallet and tries to bypass the Indian banking system. This is a violation of FEMA Section 3.

Example 2:

A business sends money to a foreign supplier using unofficial channels instead of bank remittance. Also a violation.

Section 4 : Holding Foreign Assets Rules

FEMA Section 4 controls whether Indian residents can hold foreign assets. You cannot hold or own foreign currency, foreign property, or foreign securities unless permitted under Foreign Exchange Management Act or RBI guidelines.

Means:

- You can’t keep export earnings abroad indefinitely

- You can’t hold foreign accounts without permission

Example 1:

An exporter keeps his payment in a foreign account without repatriating it to India. That can trigger FEMA issues.

Example 2:

An individual invests in foreign shares without using approved routes like LRS(Liberalized Remittance Scheme). That’s also restricted.

Section 5 : Current Account Transactions Allowed

This is where FEMA becomes business friendly. Under FEMA Section 5, current account transactions are generally allowed unless specifically restricted.

These include:

- import/export payments

- travel expenses

- education fees

- remittances

Example 1:

You pay a supplier in China for raw materials. This is allowed as a current account transaction.

Example 2:

A parent sends money abroad for a child’s education. Also allowed.

Capital Account Transactions (RBI Approval Required)

This is where things get stricter.

Capital account transactions involve assets, investments, or liabilities across borders.

These require:

- RBI permission

- limits

- reporting

These include:

- foreign direct investment (FDI)

- overseas investments

- foreign loans

Example 1:

An Indian company investing in a foreign subsidiary must follow RBI guidelines.

Example 2:

Taking a loan from a foreign lender requires compliance under FEMA capital account rules.

This is the real difference in current account vs capital account FEMA:

- current = day to day payments

- capital = asset/investment related movement

Role of Authorized Dealers (Banks)

Banks are not just middlemen. They are FEMA enforcement checkpoints.

Authorized Dealers (AD banks) are responsible for:

- verifying documents

- ensuring compliance

- reporting to RBI

They decide whether your money gets released.

Example 1:

Your export payment arrives, but your shipping bill doesn’t match your invoice. The bank will hold the payment.

Example 2:

A freelancer receives a large foreign payment. The bank may ask for purpose code and documentation before credit.

If the bank is not satisfied, the money doesn’t move. Simple.

Types of Transactions Under FEMA (Very Important for Exporters)

Everything under Foreign Exchange Management Act falls into two buckets. If you don’t understand this split, you’ll keep making compliance mistakes.

Current Account Transactions

A current account transaction under FEMA is any payment related to regular business or personal expenses.

This includes:

- export and import payments

- travel expenses

- education fees

- remittances to family

These are generally allowed freely unless specifically restricted.

Example 1: Paying overseas supplier

You import raw material from Germany and send payment in EUR. This is a current account transaction.

Example 2: Receiving export payment

You export goods to the USA and receive USD in your bank account. This is also a current account transaction governed by FEMA rules for export payment.

Capital Account Transactions

A capital account transaction under FEMA changes your assets or liabilities across borders.

This includes:

- FDI (foreign direct investment)

- foreign loans

- overseas investments

These are regulated and require approvals, limits, and reporting.

Example 1: Receiving foreign investment

A US investor puts money into your Indian startup. This falls under capital account and must follow Foreign Exchange Management Act investment rules.

Example 2: Investing abroad

An Indian resident buying property or shares abroad under LRS comes under capital account.

- Current account = operational money flow

- Capital account = ownership and investment flow

If you mix these up, you create compliance problems. If you understand them, you move money smoothly and legally.

FEMA in Export Business: How It Affects Your Payments

This is the part that actually decides whether you get paid on time or not.

Forget theory. FEMA in export business is a step by step compliance pipeline that every payment must pass through.

Here’s how your export payment actually moves under FEMA export payment rules India.

Step 1: Shipment Leaves India

You ship your goods and file export documents:

- Commercial invoice

- Shipping bill

- BL or AWB

- Packing list

These documents become the proof that your foreign payment is legitimate. If your paperwork is messy here, your payment will get stuck later. No exceptions.

Step 2: Buyer Pays in Foreign Currency (FCC)

Your buyer sends money in a freely convertible currency like:

- USD

- EUR

- GBP

Under Foreign Exchange Management Act, export payments must come in foreign currency, not INR.

Step 3: Bank Checks FEMA Compliance

This is the most critical step.

Your bank (Authorized Dealer) will verify:

- invoice value vs shipping bill

- buyer details

- purpose code

- export declaration

If anything doesn’t match, the bank holds your payment. This is what Foreign Exchange Management Act compliance for exporters actually looks like in the real world.

Step 4: Currency Conversion

Once verified:

- the bank converts FCC to INR

- based on the current forex rate

- and credits your current account

Exchange rate fluctuation here directly affects how much money you receive.

Step 5: FIRC and BRC Issued

After the payment is credited:

- Bank issues FIRC (Foreign Inward Remittance Certificate)

- Later, you receive BRC (Bank Realization Certificate)

FIRC, BRC meaning in simple terms:

- FIRC = proof that foreign money entered India

- BRC = proof that export payment is realized (used for GST refunds, RoDTEP, incentives)

Without these, you cannot claim export benefits.

Examples

Example 1: USD payment from US buyer

You export garments worth $10,000 to a US buyer. The buyer sends USD to your bank. The bank verifies your export documents under FEMA, converts USD to INR, credits your account, and issues FIRC. Later you get BRC for export incentives.

Example 2: EUR payment from Germany buyer

You ship machinery parts to Germany and receive €5,000. The bank checks Foreign Exchange Management Act compliance, converts EUR to INR, credits your account, and issues compliance certificates. If your invoice and shipping bill mismatch, the payment gets held until corrected.

What this really means for you

FEMA is not paperwork. It is your cash flow control system.

If you understand it:

- you get paid faster

- you avoid delays

- you stay compliant

If you ignore it:

- your payments get stuck

- your bank keeps asking for clarification

- your working capital gets blocked

Enforcement, Penalties and Compliance

Foreign Exchange Management Act is business friendly, but don’t mistake that for “no consequences.”

Violations are civil, but penalties are still serious.

Directorate of Enforcement – Who Investigates

The Enforcement Directorate (ED) handles FEMA enforcement.

They investigate:

- illegal foreign transactions

- unreported foreign assets

- suspicious export/import payments

They have the authority to:

- issue notices

- investigate transactions

- impose penalties

This is the role of the Enforcement Directorate FEMA system.

Civil Penalties (Not Criminal Like FERA)

Under FEMA:

- violations are civil offences, not criminal

- but penalties can still be heavy

Penalty can go up to:

- 3 times the amount involved, or

- ₹2 lakh, plus

- ₹5,000 per day for continuing violations

That’s your fema violation penalty in practical terms.

Compounding of Offences

FEMA allows compounding.

That means:

- you can admit the violation

- pay the penalty

- close the case without long legal battles

This is a major difference from FERA’s criminal prosecution model.

Appeals Process

If you don’t agree with the order:

- you can appeal to Special Director (Appeals)

- then to the Appellate Tribunal

So there is a structured legal path available.

Violation Examples

Example 1: Receiving payment without proper documents

An exporter receives foreign payment but fails to submit shipping bill and invoice matching details. The bank reports it. This can lead to FEMA investigation and penalty.

Example 2: Holding foreign assets illegally

A resident keeps export earnings in a foreign account without repatriation or RBI approval. This is a direct FEMA violation and attracts penalties.

The bottom line

FEMA is flexible, but not optional.

Follow the rules:

- your payments flow smoothly

- your business stays clean

Ignore them:

- your money gets stuck

- and you risk fema penalties India that can wipe out your profit

That’s the trade off.

Difference Between FERA and FEMA (Clear Comparison)

Most beginners don’t fully grasp why FEMA is easier to work with until they see how it compares with the old system.

Here’s the clean difference between FERA and FEMA in a practical, side-by-side format.

| Aspect | FERA (Foreign Exchange Regulation Act, 1973) | FEMA (Foreign Exchange Management Act, 1999) |

| Approach | Restrictive, control-focused | Facilitating, trade-friendly |

| Nature of Offence | Criminal offence (jail possible) | Civil offence (monetary penalty) |

| Permission System | Everything prohibited unless allowed | Everything allowed unless restricted |

| Residency Definition | 6 months stay rule | 182 days stay rule (clearer and practical) |

What this really means in practice

Example 1: Export payment delay

Under FERA, a delay in receiving export payment could trigger criminal liability. Under FEMA, it’s treated as a compliance issue with a civil penalty or clarification process.

Example 2: Foreign investment into India

Under FERA, approvals were complex and restrictive. Under FEMA, FDI is structured, allowed, and regulated through clear RBI frameworks.

FERA punished. FEMA manages and enables.

If you’re running an export business today, you are operating under fema vs fera India’s modern system, which is built to support trade, not block it.

Documents Required for FEMA Compliance (Practical Section)

This is where most exporters mess up. Banks don’t release your payment just because money arrived. They release it only after verifying FEMA compliance documents.

Here are the documents for export payment India banks typically require.

1. Commercial Invoice

This is your primary sales document. It must match:

- shipment value

- buyer details

- currency used

If your invoice and shipping bill don’t match, payment gets held.

2. Shipping Bill

This is proof that goods have actually been exported.

It contains:

- export value

- product details

- destination country

Banks cross check this with your invoice.

3. Packing List

Details the physical contents of the shipment:

- quantity

- weight

- packaging details

Used for verification and customs validation.

4. Bill of Lading (BL) / Airway Bill (AWB)

This proves the shipment has been transported.

- BL for sea shipments

- AWB for air shipments

Without this, export proof is incomplete.

5. IEC (Importer Exporter Code)

Your IEC proves you are legally allowed to export from India.

No IEC = no export payment processing.

6. AD Code (Authorized Dealer Code)

Your bank’s AD code is registered with customs and links your exports to your bank account. If this is not properly registered, payments can get blocked.

7. GST Invoice

Required for:

- GST compliance

- claiming refunds

- export documentation matching

Mistake Examples

Example 1: Invoice mismatch

Your invoice says $8,000 but shipping bill shows $7,500. Bank flags it and holds your payment until corrected.

Example 2: Missing AD code

You export goods but forget to link your AD code with customs. Payment arrives but cannot be processed properly by the bank.

What this really means

These are not optional documents. They are your FEMA compliance documents for export.

If they are:

- correct → payment flows smoothly

- incorrect → payment gets stuck

- missing → payment gets rejected or delayed

Simple cause and effect.

Common Mistakes Exporters Make Under FEMA

Most export payment problems are not because of buyers. They’re because of basic FEMA compliance mistakes exporters keep repeating.

Here are the big ones that cause export payment delay India rules issues.

1. Invoice Mismatch

Your invoice must match your shipping bill and export documents exactly.

If values don’t match:

- bank flags the transaction

- payment gets held

- you get queries and delays

Example 1: Invoice value mismatch with shipping bill

Invoice shows $10,000 but shipping bill shows $9,600. The bank will not release funds until you correct and justify the difference.

2. Delayed Realization of Payment

RBI sets timelines for receiving export payments. If your payment comes late and you don’t report or extend properly, it becomes a compliance issue.

Example 2: Payment received after RBI timeline

You export goods but receive payment after the allowed realization period. If you don’t file for extension or explain the delay, it becomes a FEMA violation.

3. Wrong Currency Usage

Export payments must come in freely convertible currency.

Common mistake:

- agreeing to receive INR from a foreign buyer

- or receiving money through unofficial channels

This creates compliance problems and can even lead to penalties.

4. Missing or Incorrect Documents

Banks need full documentation to process export payments under FEMA.

If any of these are missing:

- shipping bill

- BL/AWB

- AD code

- invoice

your payment will be held.

The brutal truth

These are not “small mistakes.”

Each one directly blocks your cash flow.

If you run exports seriously, you need a document system and payment tracking system. Otherwise, you’ll keep chasing your own money.

FEMA + FCC: How Both Work Together

A lot of beginners treat FEMA and FCC as separate topics. That’s a mistake. You cannot understand export payments unless you understand FEMA and FCC together.

What is FCC in simple terms

FCC means Freely Convertible Currency.

These are currencies that can be easily exchanged globally:

- USD

- EUR

- GBP

- JPY

- AUD

- CAD

These are the currencies used in international trade.

Why FCC is mandatory for export payments

Under FEMA rules:

- export payments must come in foreign currency

- that currency must be freely convertible

This is required so:

- banks can convert the money into INR

- RBI can track foreign exchange inflow

- the transaction remains legal and verifiable

This is the core of freely convertible currency export India rules.

Why INR cannot be used

INR is not fully freely convertible globally.

So:

- foreign buyers cannot directly pay you in INR (in most cases)

- Indian banks require foreign currency inflow first

- then they convert it into INR

Trying to bypass this creates compliance issues.

How FEMA and FCC work together in real payments

Here’s the actual workflow:

- You export goods

- Buyer pays in FCC (USD/EUR etc.)

- Bank receives foreign currency

- Bank checks FEMA compliance

- Bank converts FCC into INR

- Bank credits your account and issues FIRC/BRC

That’s the system.

Real World Examples

Example 1: USD export payment

A US buyer sends $7,000. Since USD is an FCC, the bank processes it under FEMA, converts to INR, and credits your account.

Example 2: EUR export payment

A German buyer sends €4,500. The bank verifies FEMA compliance, converts EUR to INR, and releases funds after document validation.

this means

- FCC ensures smooth global payment flow

- FEMA ensures legal compliance and tracking

One handles the currency. The other handles the law. If you understand both, your export payments become predictable, compliant, and fast.

Conclusion

Let’s strip this down to reality.

FEMA is not optional.

It is the rulebook that controls every rupee of foreign money entering your business.

It directly affects:

- whether your payment gets credited

- how fast you receive it

- whether you face compliance queries

- whether you qualify for export incentives

If you treat FEMA casually, you’ll deal with:

- payment delays

- document rejections

- blocked working capital

If you understand it properly:

- your payments flow smoothly

- your bank interactions become easier

- your risk of penalties drops dramatically

This is not about memorizing law sections.

It’s about protecting your cash flow.

Learn FEMA once, avoid payment problems for years.

FAQs

Let’s answer the questions people actually search for but rarely get explained properly.

1. Is FEMA mandatory for export payments?

Yes. Completely mandatory.

Every foreign currency transaction entering or leaving India is governed by the Foreign Exchange Management Act, 1999. Banks cannot legally credit your export payment unless it complies with FEMA guidelines.

There is no workaround.

No “informal” route.

No shortcut.

If you are exporting, you are automatically under FEMA.

2. Can exporters receive payment in INR?

In most standard export transactions, no.

Export payments are expected to come in freely convertible currency like USD or EUR. The bank then converts that foreign currency into INR.

Why? Because FEMA tracks foreign exchange inflow. If payment comes directly in INR from abroad, it bypasses that tracking mechanism and creates compliance complications.

There are limited exceptions under specific RBI mechanisms, but for regular exporters, assume this rule:

Foreign buyer → pays in FCC → bank converts to INR.

3. What happens if FEMA rules are violated?

Violations are civil, not criminal like under FERA. But that doesn’t mean harmless.

Penalties can be:

Up to three times the amount involved

Or ₹2 lakh

Plus daily penalties for continuing violations

In serious cases, the Enforcement Directorate can investigate.

Two common triggers:

Export payments not realized within allowed timelines

Foreign assets held without proper approval

You won’t go to jail for minor compliance issues. But you can lose serious money in penalties.

4. What is the time limit to receive export payments?

RBI prescribes a realization period for export proceeds. Exporters are expected to receive payment within the permitted timeline from the date of shipment.

If payment is delayed:

You must seek extension through your bank

Or provide valid explanation

Ignoring delays is what turns a business issue into a compliance issue.

5. What documents are required for smooth FEMA compliance?

Banks typically require:

Commercial invoice

Shipping bill

BL/AWB

IEC

AD code details

If documents match and timelines are followed, payments are processed smoothly.

If documents mismatch, payment gets stuck. It’s that simple.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.

1 thought on “FEMA in Export Business: How the 1999 Act Controls Your Payments”