You’ve done the hard work. You manufactured a quality product, found an international buyer, and successfully shipped the order. The invoice is sent, and now you wait. And wait. For 30, 60, or even 90 days, your money is tied up overseas, leaving a critical gap in your cash flow.

For small and growing export businesses, this delay isn’t just an inconvenience it can halt operations, prevent you from taking on new orders, and limit growth. This is a common struggle in international trade. You need working capital to pay suppliers, cover payroll, and reinvest in your business, but your funds are locked in accounts receivable.

What if you could get paid for your international sales almost immediately, eliminate the risk of non-payment, and focus on what you do best? That’s where export factoring comes in, providing a powerful solution for immediate cash, reduced risk, and smoother operations.

Let’s break down what export factoring really is and how it works in real business situations.

Table of Contents

What Is Export Factoring?

At its core, the export factoring meaning is simple, it is a financial arrangement where an export business sells its unpaid international invoices (accounts receivable) to a third party financial institution called a “factor.” Instead of waiting for the foreign buyer to pay, you receive an immediate cash advance from the factor.

This process is a form of international invoice financing designed specifically for global trade.

Here’s how it typically unfolds. The factor pays you a large percentage of the invoice’s value upfront, usually between 80% and 90%. Once your international customer pays the invoice in full, the factor sends you the remaining balance, minus their fees.

This transaction involves three key parties:

- The Exporter: Your business, which has sold goods or services to an international customer.

- The Importer: The foreign buyer who owes payment on the invoice.

- The Factor: The specialized finance company that buys your invoice and provides the cash advance.

Let’s look at how export factoring explained with a couple of quick examples can help an invoice factoring export business.

- Example 1: A textile exporter in India ships a $50,000 order of fabrics to a buyer in the UAE on 60-day payment terms. Instead of waiting two months, the exporter sells the invoice to a factor. The factor immediately advances them $40,000 (80% of the invoice). The factor then collects the full $50,000 from the UAE buyer and pays the remaining $10,000 to the exporter, less its service fee.

- Example 2: A spices exporter in Vietnam sends a $20,000 shipment to a supermarket chain in the UK. They use export factoring to receive an immediate $18,000 (90%) advance. This allows them to purchase more raw materials for their next order without delay.

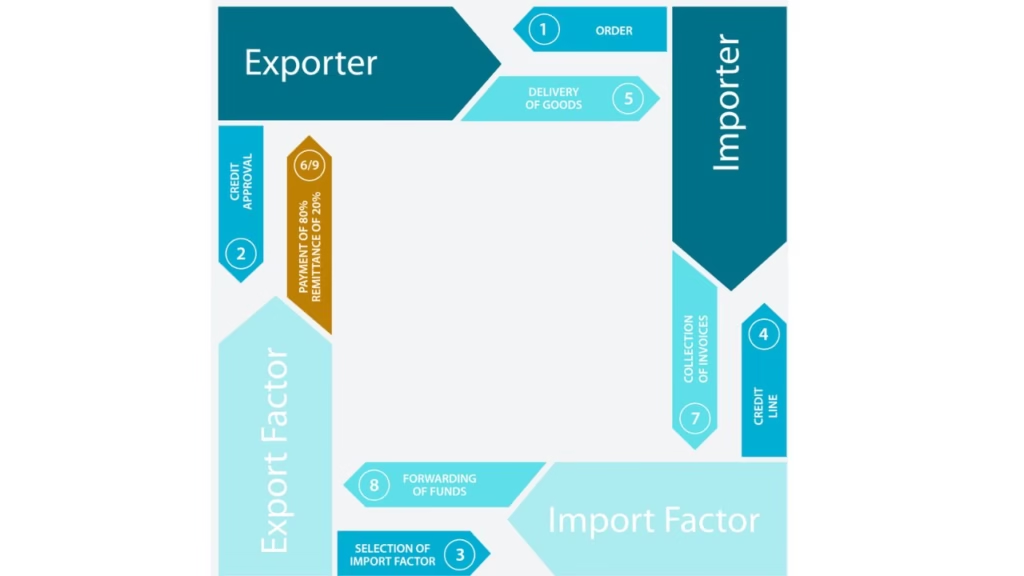

How Export Factoring Works (Step by Step Flow)

Understanding the export invoice financing process is straightforward. It’s a clean, linear flow designed to get cash into your hands quickly so you can keep your business moving forward.

Here are the typical factoring steps international trade professionals follow:

1) Ship Your Goods on Credit:

You fulfill an order for an international buyer and ship the goods. As part of your sales agreement, you offer credit terms, meaning the buyer has a set period (often 30, 60, or 90 days) to pay the invoice.

2) Raise and Submit Your Invoice:

You generate an invoice for the shipment and send a copy to both your customer and your chosen factoring partner.

3) Sell the Invoice to the Factor:

You formally sell the rights to the invoice to the factoring company. This is the core of the transaction.

4) Receive an Immediate Cash Advance:

The factor verifies the invoice and quickly advances you a significant portion of its value, typically between 80% and 90%. This cash is deposited directly into your account, often within a few days.

5) The Factor Manages Collection:

The factor takes over the responsibility of collecting the payment from your international buyer. In many cases, they work with a partner factor in the buyer’s country to manage this process seamlessly. You no longer have to chase late payments.

6) Receive the Remaining Balance:

Once the foreign buyer pays the full invoice amount to the factor, the factor releases the remaining balance (the 10-20% held in reserve) to you, minus their agreed upon fees.

This simple process has powerful real world applications.

- Use Case for a Manufacturer: A furniture manufacturer secures a large order from a US retail chain but needs capital to purchase lumber for the next production cycle. By factoring the invoice, they receive an immediate cash injection, allowing them to fund the next round of production without waiting 90 days for payment.

- Use Case for an Agricultural Exporter: An agricultural business exporting fresh produce needs to reinvest in seeds and equipment quickly to prepare for the next harvest. Export factoring provides the immediate working capital to do so, ensuring they don’t miss a critical planting window while waiting for overseas payments.

Types of Export Factoring

Not all factoring arrangements are the same. The main types of export factoring are designed to meet different business needs, primarily revolving around your urgency for cash and appetite for risk. Choosing the right one is a key decision.

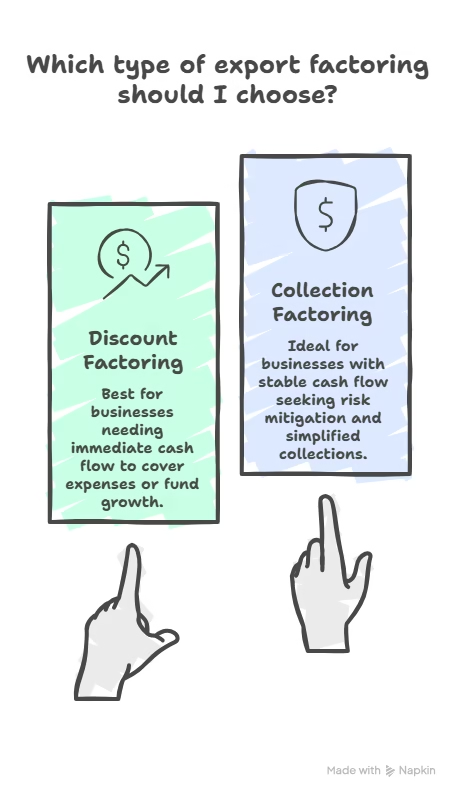

Discount Factoring

This is the most common form of factoring. With discount factoring, you receive a cash advance almost immediately after your invoice is approved by the factor. The cost is calculated based on a “discount rate” and the length of the payment term. The longer the buyer takes to pay, the higher the fee.

Best for: Businesses that need immediate working capital to cover operational expenses, fund new orders, or fuel growth.

Collection Factoring

In this arrangement, the factor still manages collections and often provides credit protection, but you don’t receive payment until the invoice’s maturity date. The primary benefit here is risk mitigation and outsourcing your collections process. The fee is typically a fixed percentage of the invoice value, usually between 1% and 4%.

Best for: Businesses with stable cash flow who are more concerned with protecting themselves against buyer default and simplifying their accounts receivable management.

Discount Factoring vs. Collection Factoring: Which Is for You?

Choosing between these factoring options for exporters comes down to a simple question What is your primary goal?

- Choose Discount Factoring if your main challenge is cash flow. You need money now to run and grow your business.

- Choose Collection Factoring if your main challenge is risk and administration. You can afford to wait for payment but want to guarantee you get paid and offload the hassle of collections.

Your decision will depend on your cash urgency and risk tolerance. Many exporters find that the immediate liquidity offered by discount factoring provides the greatest competitive advantage in the fast moving world of global trade.

Key Benefits of Export Factoring

The advantages of using export factoring extend far beyond just getting paid faster. It’s a strategic tool that offers significant competitive benefits, allowing you to operate with more confidence and flexibility in the global market. Here are the main export factoring benefits that can transform your business.

1. Immediate Cash Flow Injection

This is the most critical advantage. Instead of waiting 60 or 90 days for an international buyer to pay, you get access to the bulk of your funds within days. This ability to improve cash flow export business operations means you can pay your suppliers on time, meet payroll without stress, and cover other operating expenses without delay.

2. Significant Credit Protection

One of the biggest fears in international trade is the risk of buyer non-payment or bankruptcy. In a non-recourse factoring agreement, the factor assumes this credit risk. If your foreign customer fails to pay due to financial inability, you are protected. This helps you reduce export payment risk and expand into new markets with greater peace of mind.

3. Outsourced Collections and Accounts Receivable Management

Chasing international payments can be a time consuming and frustrating process, complicated by different time zones, languages, and business cultures. When you partner with a factor, they handle all collection activities. This frees up your team to focus on core activities like production, sales, and customer service instead of administrative follow ups.

4. No Additional Collateral Required

Unlike traditional bank loans that often require you to pledge business or personal assets as collateral, export factoring is based on the quality of your invoices. The accounts receivable themselves serve as the underlying asset. This makes it an accessible financing option for small and growing businesses that may not have significant fixed assets to offer.

5. Faster Business Growth and Scalability

With a predictable and accelerated cash flow, you can re-invest in your business much faster.

- Example for a small exporter: A growing coffee bean exporter can use the immediate funds from a factored European order to purchase a larger quantity of beans from farmers, allowing them to fulfill a new, bigger order from an American café chain without missing a beat.

- Example for a manufacturer: A parts manufacturer can confidently take on larger contracts from international automotive clients, knowing they will have the working capital to fund the extended production runs required.

Understanding the Costs of Export Factoring

To make an informed decision, it’s essential to be transparent about the costs. While the export factoring fees are typically higher than for a service like credit insurance alone, the price reflects a comprehensive package of benefits financing, risk protection, and collections services all in one.

The factoring cost international trade companies pay is not one size fits all. The final price depends on several key variables:

- Invoice Volume: Higher volumes and larger invoice values often lead to lower percentage fees.

- Payment Tenure: The longer the payment term (e.g., 90 days vs. 30 days), the higher the cost, as the factor’s capital is tied up for a longer period.

- Buyer’s Country and Creditworthiness: Risk is a major factor. Invoices for buyers in stable, low risk countries will have lower fees than those in high risk regions.

- Quality of Documentation: Clear, accurate, and complete paperwork can help streamline the process and may result in better rates.

Generally, invoice financing charges can expect to fall into a range of 1% to 4% of the invoice value for collection factoring. For discount factoring, the cost is built into the discount rate. You aren’t just paying a fee you’re investing in speed, security, and operational efficiency that can unlock new growth opportunities for your export business.

Who Should Use Export Factoring?

Export factoring isn’t a universal solution for every business, but for the right company, it can be a game changer. It is particularly effective for businesses that have strong products and international demand but lack the working capital to wait months for payment.

Ideal Candidates for Export Factoring

- Small and Medium Sized Enterprises (SMEs): These businesses often face the “liquidity trap” they have orders but not the cash to fulfill them. Factoring bridges this gap, providing the best financing for small exporters who need to compete with larger players.

- Agriculture Exporters: Fresh produce and commodities move fast, and so should the money. Agricultural businesses often need to pay farmers immediately, making the speed of factoring essential.

- Manufacturing Businesses: With high upfront costs for raw materials and labor, manufacturers need steady working capital for export business cycles. Factoring allows them to keep production lines moving without pausing for invoice payments.

- New Exporters Without Strong Credit Lines: Banks are often hesitant to lend to new exporters without years of financial history or heavy collateral. Factors look primarily at the creditworthiness of your buyers, not just your balance sheet, making this an accessible option for newer entrants.

Who Is It Not Ideal For?

- Very Low Margin Businesses: Since factoring involves a fee (typically 1-4%), businesses with extremely razor thin margins might find the cost eats too much into their profit.

- Domestic Only Sellers: As the name implies, export factoring is designed for cross border trade. Domestic factoring exists, but the risks and structures differ.

Real World Profiles

- Profile A: The New Spice Exporter

Ravi has just started exporting organic turmeric to a buyer in Germany. It’s a huge opportunity, but the buyer demands 60-day payment terms. Ravi needs cash now to pay the local farmers he sources from. By using export factoring, he gets paid 80% of the invoice value immediately upon shipment, satisfying his suppliers and securing his supply chain for the next order. - Profile B: The Garment Manufacturer

Sarah runs a boutique garment factory and just landed her first contract with a French retail chain. The order volume is double what she’s used to. She doesn’t have the credit history for a bank loan. She uses export factoring to fund the fabric purchase and labor costs, effectively using the French retailer’s strong credit rating to finance her own growth.

These examples highlight who needs export factoring most, ambitious businesses where cash flow is the only bottleneck to growth.

Export Factoring vs. Other Finance Options

Navigating the landscape of trade finance can be confusing. How does factoring stack up against traditional methods? Let’s look at a direct export finance options comparison.

| Feature | Export Factoring | Export Credit Insurance | Bank Loans | Letter of Credit (LC) |

| Primary Function | Financing + Risk Protection + Collections | Risk Protection Only | Financing Only | Payment Security |

| Speed of Cash | Immediate (24-48 hours) | None (Payout only if buyer defaults) | Slow (Weeks for approval) | Upon presentation of docs |

| Collateral Needed | The Invoice itself | None | Physical Assets / Real Estate | Cash or Credit Line |

| Buyer Credit Risk | Covered by Factor (Non-recourse) | Covered by Insurer | Borne by Exporter | Bank Guarantee |

| Cost | Higher (Service + Finance fee) | Lower (Premium only) | Interest + Fees | Moderate to High fees |

The Verdict

Export Factoring vs. Credit Insurance:

Insurance protects you if a buyer goes bankrupt, but it doesn’t give you cash today. Factoring does both.

Factoring vs. Letter of Credit:

An LC is very secure but can be expensive and administratively heavy for the buyer, sometimes discouraging sales. Factoring is invisible to the buyer (in some structures) or simply seen as a payment instruction, making it more sales friendly.

Factoring vs. Bank Loan:

Loans add debt to your balance sheet and require collateral. Factoring is an asset sale, not a loan, keeping your balance sheet cleaner.

If speed and flexibility are your priorities, export factoring is often the superior choice. It converts your sales ledger into a liquid asset, solving the cash flow puzzle that holds so many exporters back.

Risks and Limitations: What You Need to Know

While export factoring is a powerful tool for accelerating cash flow, it is not a magic wand. To make a smart business decision, you must understand the potential downsides. Being aware of the export factoring risks ensures you aren’t caught off guard and can manage your financing strategy effectively.

First, consider the cost. Factoring is a premium service that bundles financing, credit protection, and collections. Consequently, it is generally more expensive than a traditional bank line of credit. You are paying for speed and convenience, which comes at a price. If your margins are extremely thin, the factoring fees might eat too deeply into your profits.

Second, approval isn’t guaranteed. Unlike a bank loan that looks at your creditworthiness, a factor looks at your buyer’s creditworthiness. If your international customer has a poor payment history or is located in a high risk jurisdiction, the factor may refuse to buy the invoice.

Third, the process demands operational precision. One of the main disadvantages of factoring export invoices is the strict requirement for accurate documentation. If your invoices, bills of lading, and purchase orders don’t match perfectly, funding will be delayed.

Finally, unless you lock in specific hedging services, currency risks may still exist. If the invoice is in a foreign currency and exchange rates shift between the time of shipment and final settlement, your final payout could fluctuate.

Real World Scenarios to Watch For:

- The “Weak Credit” Rejection: Imagine you land a massive order from a new distributor in Brazil. You are ready to ship, but when you submit the potential invoice to your factor, they reject it. Why? Their credit check reveals the distributor is months behind on payments to other suppliers. While frustrating, this actually saves you from shipping goods to a buyer who likely wouldn’t have paid you.

- The “Paperwork” Delay: You ship a container of electronics to Germany and submit the invoice for immediate funding. However, the purchase order number on your commercial invoice has a typo and doesn’t match the customer’s PO. The factor freezes the advance until you reissue corrected documents and get the buyer to acknowledge them, delaying your cash by a week.

How to Choose the Right Export Factoring Company

Not all factors are created equal. Your choice of partner can determine whether your export business thrives or gets trapped down in hidden fees and administrative headaches. Choosing the right invoice financing provider for your export business requires a thorough review.

Here is an actionable checklist to help you identify the best export factoring companies for your specific needs:

Check the Advance Rate:

Will they advance 80%, 90%, or even 95% of the invoice value? A higher advance rate improves your immediate working capital position.

Analyze the Fee Structure:

Look beyond the headline rate. Are there application fees, origination fees, or penalties for invoices that remain unpaid past a certain date? Transparency is key.

Verify Supported Countries:

Does the factor have experience and legal reach in the specific countries where your buyers are located? If you sell to Vietnam, a factor who specializes only in European trade won’t help you.

Assess the Collection Network:

Remember, the factor will be contacting your customers to collect payment. Do they have a professional, local presence in the buyer’s country? You want a partner who maintains your customer relationships, not one who damages them with aggressive tactics.

Review Reputation and Speed:

How fast can they set up an account? How quickly do they fund after you submit an invoice? Look for reviews from other exporters in your industry.

Choosing the right partner directly impacts your margins and payment security. Don’t just pick the first option you find on Google compare your options to find a partner who understands your industry and can scale with you as you grow.

Knowing how to choose factoring company partners effectively is just as important as the financing itself.

Ready to Scale Your Export Business?

If you’re serious about scaling your export business without constant cash flow stress, export factoring can be a powerful tool when used correctly. It’s the bridge between shipping an order and having the capital to fund the next one immediately.

While the concept is simple, the execution requires the right partner. Every exporter’s needs are unique whether you need high advance rates, specific country coverage, or non-recourse protection. Don’t settle for the first option you find compare providers to ensure you get terms that protect your margins.

If you are ready to explore your options:

- Compare Top Export Factoring Providers

- Consult with an Export Finance Expert

- Get a Free Quote for Factoring Services

Conclusion

Export factoring is not just a financing mechanism it is a strategic growth tool for ambitious exporters. It removes the two biggest barriers to international trade the long wait for payment and the risk of buyer default.

By unlocking the cash tied up in your supply chain, you gain the freedom to accept larger orders, negotiate better terms with suppliers, and expand into new markets with confidence.

It helps you sell more, faster, and safer. Instead of worrying about when you’ll get paid, you can focus on what matters most delivering quality products to the world. Used right, it can turn your unpaid invoices into your biggest growth engine.

Frequently Asked Questions (FAQ)

Here are answers to some common questions exporters have about factoring.

1. Is export factoring safe for small exporters?

Yes, it is considered very safe, and in many ways, it’s safer than traditional exporting on open account terms. The primary reason is risk mitigation. With a non-recourse factoring agreement, the factor assumes the credit risk of your foreign buyer.

This means if your customer fails to pay due to insolvency, you are protected from taking a loss. This export factoring safety net is one of its biggest advantages for small businesses that cannot afford to absorb bad debt.

2. How fast do I get paid after submitting an invoice?

Speed is the core benefit of factoring. Once your account is set up and you submit a valid invoice, you can expect to receive the cash advance very quickly, often within a 24 to 48-hour window.

This fast invoice payment provides immediate access to 80-90% of your invoice’s value, transforming your accounts receivable into working capital almost instantly.

3. What happens if the buyer doesn’t pay the factor?

This depends on the type of factoring agreement you have.

Non-Recourse Factoring: If the buyer is financially unable to pay (e.g., they go bankrupt), the factor absorbs the loss. You keep the advance and are not liable for the unpaid amount. This is the most common and secure option for exporters.

Recourse Factoring: If the buyer defaults, you are responsible for buying back the invoice or repaying the advance to the factor. This option is less expensive but carries significantly more risk for you, the exporter.

4. Is export factoring better than a Letter of Credit (LC) for small shipments?

For small to medium-sized shipments, export factoring is often more flexible and cost-effective than a Letter of Credit. LCs are highly secure but can be expensive, slow, and administratively burdensome for both the exporter and the importer.

The complex paperwork can lead to discrepancies and payment delays. Factoring is a much simpler process, making it a more sales-friendly option that doesn’t bog down smaller transactions in bank fees and red tape.

5. Do I need collateral to use export factoring?

No, you do not need to pledge physical assets like real estate or equipment as collateral. In an export factoring arrangement, your unpaid invoices are the collateral. The financing is secured by the value of your accounts receivable and the creditworthiness of your international customer.

This makes factoring an accessible funding solution for asset-light businesses and growing companies without a long credit history.

About the Author

Hi, I’m SriHarsha, founder of shxhub.in.

I focus on explaining import export business topics in a practical, beginner friendly way, based on how exports actually work on the real ground especially documentation, quality control, and buyer expectations.